International Journal of Scientific & Engineering Research, Volume 4, Issue 8, August 2013 894

ISSN 2229-5518

Feasibility Study of Available Georesources at

Kanaighat Thana in Sylhet District, Bangladesh

Isteyak Ahmad & Mohammad Shahedul Hossain

Abstract— This paper reports feasibility study of available georesources at Kanaighat thana in Sylhet district. In Kanaighat, rocks are found as available georesource. The source of these rocks is near Meghalaya of India. Luba River is the main rock quarry in Kanaighat Thana. Every day approximately 400,000 cubic feet of rocks have been extracting commercially from this quarry. People normally use manual hand tools during rock extraction. There are 7 crusher mills established whose main task is to give these rocks various sizes and shapes. A Technical & Economic analysis has been applied over this project area, to make this project more informative and worthwhile. Although there are some technical shortcomings in extraction area and its surroundings, but after economic analysis it can be said that Rock extraction project in Luba quarry is economically feasible.

Index Terms— feasibility study, georesources, Economical analysis, Technical analysis, Kanaighat Thana, Quarry, Crusher mill

1 INTRODUCTION

—————————— ——————————

easibility study means a study designed to determine the practicability of a system or a plan [1].

Technical or technological feasibility study is carried out to determine whether the company has the capability, in terms of software, hardware, personnel & expertise, to handle the completion of the project [2].

Economic feasibility study is the most frequently used

method for evaluating the effectiveness of a new system.

More commonly known as cost/benefit analysis, the

procedure is to determine the benefits & savings that are expected from a candidate system & compare them with costs [2].

Although Kanaighat thana of Sylhet district are not so renowned for georesources like some other Thanas of

sylhet division, which are enriched with natural gas, oil etc. but a massive rock quarry are found at Luba river in Kanaighat called Lubachhara or Luba quarry. These rocks are mainly used in constructional purposes. In Kanaighat Thana Luba River is the only quarry from which rocks can be produced commercially. The sources of Kanaighat rock is the nearby Meghalaya of India. This part of India is relatively in higher ground level than Bangladesh. That’s why the rock comes down by gravity especially in the rainy season. The water is the main transportation media which brings these rocks. Yet there is no gas and oil field found in kanaighat. Though sand are also being found here but being insignificant in both quality & quantity, are not produced commercially from this area. Based on Luba River which is usually known as Luba rock quarry people get involve in rock business. In average approximately

400,000 cubic feet of rock [according to questionnaire survey] can be extracted in everyday. Some crusher mills are also established in kanaighat based on rock business. Here in kanaighat the main problem is rock transportation from quarry to different places in Kanaghat & outside. Because in the dry season Luba River got dry and there is no road way from quarry to different places. That’s why boat and small ship carry these rocks and transport it only

in the rainy season from quarry to different places in Sylhet Division & outside. In the dry season people make some temporary economy floating bridge as path way over the canals with personal efforts to keep their business continuous. The given information at below has been applied for feasibility analysis.

Some factors of Technical Feasibility

Is the project possible with current technology?

What technical risk is there?

Availability of the technology :

o Is it available locally?

o Can it be obtained?

o Will it be compatible with other systems? Those factors are obtained from Whitten, Bentley & Dittman [3], and Satzinger, Jackson & Burd [4]

Some factors Economic Feasibility

o Is the project possible, given resource constraints?

o What are the benefits?

o Both tangible and intangible

o Quantify them

o What are the development and operational costs?

o Are the benefits worth the costs? Those factors are

obtained from Whitten, Bentley & Dittman [3], and

Satzinger, Jackson & Burd [4]

From these studies it can be possible to find out such necessary data & information which reveals the feasibility of available georesources in this area, its importance, applications and economic value as well. Here only Technical and Economic feasibility study is being analyzed. In the analysis section all the data are secondary, which is collected from local people of Kanaighat Thana conducting by a questionnaire survey.

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 8, August 2013 895

ISSN 2229-5518

2 GENERAL FEATURE & SCHEMATIC LOCATION OF

KANAIGHAT THANA –

Sylhet district was established on 3 January 1782, and until

1878 it was part of Bengal province. In that year, Sylhet was

included in the newly created Assam province, and it

remained as part of Assam up to 1947 (except during the

brief break-up of Bengal province in 1905–11). In 1947,

Sylhet became a part of East Pakistan as a result of a

referendum (except the sub-division of Karimganj). Sylhet subsequently became a sub-division of Sylhet Division and was converted into a district in 1983–84. Sylhet District is divided into twelve sub-districts or Upazilas/Thanas. The Kanaighat Thana is one of them. [5]

Kanaighat (Town) consists of 5 mouzas. It has an area of

3.36 sq km; population 4590; male 53.7%, female 46.3%;

density of population is 1366 per sq km. Literacy rate among the town people 31.5%. The town has one dakbungalow. Administration Kanaighat thana was established in 1932 and was turned into an upazila in 1980. The upazila consists of 9 union parishads, 252 mouzas and

288 villages. [6]

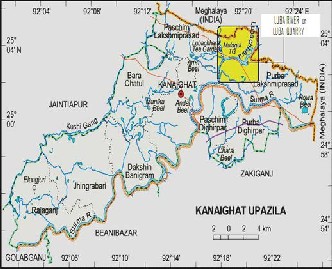

Fig. 1: Location of geo resource on Kanaighat Map [2]

On this map it has seen that a river named Luba which is connected with the river Surma & the source of Luba River is from Meghalaya. Actually the Afa & Barchara canal (locally called) are comming out from Meghalaya & by mixing with each other, they get entered into Bangladesh as a river named Luba. Between those two canal Afa & Barchara , Barchara canal brings maximum amount of these rocks to the junction of Afa, barchara & Luba.

The river Luba used to be a main depositional area of rock in Kanaighat Thana. Here these Rocks are deposited all over the river Luba. Here the area under river is approximately 5340 acres or 2162 hectare [9]. But according

to questionnaire survey the depositional area of Luba quarry is approximately 140 hectares.

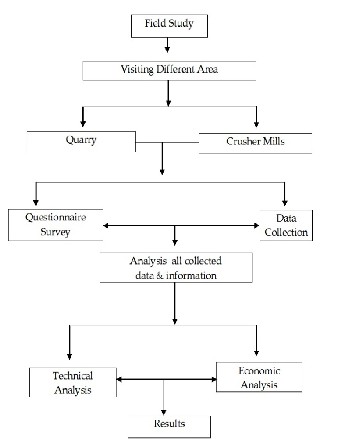

3 OBJECTIVES & METHODOLOGY

The comprehensiveness of the study is to evaluate which geo-resources amongst the available all geo-resources in Kanaighat Thana will be feasible for commercial production. Study of feasibility of prevailing resources in the area of interest begins with—

identifying the geo-resources

locating the geo-resources

performing qualitative study on the identified

resources

introducing different possible methods of extraction

calculating & performing a qualitative study of the

economical value of the studied geo-resources

finally assessing the feasibility of the prevailing resources

3.1 Methodology flowchart

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 8, August 2013 896

ISSN 2229-5518

4 ANALYSIS

4.1 Technical feasibility Analysis

In the Luba rock quarry there are very simple method have been using to extract rock. Laborers are mainly using various hand tools for this purpose. So this extraction method of rock from quarry is manual. When water level of Luba quarry would raise then a special type of pump are being used here which can drag sand with water and uncover the surface of rock deposits. But use of this type of machine is very limited. Laborers are mainly using manual hand tools such as – Spade, Pick-axe, Gauge, Shovel etc are available here for extraction purposes. Small and big engine boats are used here for transportation of extracted rocks.

At kanaighat sadar crusher mills are also available and it is seven kilometers away from Luba quarry. Here all crushers are small in size. In total 7 crushers are available in kanaighat sadar.

According to questionnaire survey some scenarios of small crushers are —

The engine of these crushers can be run by diesel.

In crusher various types of metal bits are used here during crushing rocks.

All parts of these machines are not locally available.

There are 35—40 laborers are required to maintain each

crusher production.

These small crushers cause severe dust pollution &

small noise pollution also.

The production of these small size crushers is 2000—

2500 cuft/day (here, cuft = cubic feet). The total small

size crushers are 7, so according to this the total

production by small size crusher is (2250 × 7) = 15750

cuft/day.

So, the annual production is (15750 × 365) = 5748750

cuft.

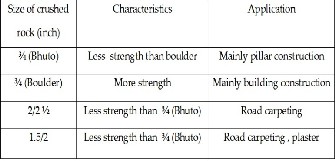

There are 4 different types of crushing rocks can be

found in small size crusher. These crushed rocks sizes

are considered as inches ( ″ )

1) ¾ ″ (Bhuto)

2) ¾ ″ (Boulder)

3) 2/2 ½ ″

4) 1.5/2 ″

Generally the required sizes are ¾″ (Bhuto) and ¾″ (Boulder). Local people call it by sthese names. There are also two sizes 2/2 ½″ and 1.5/2″, people call it with its numeric caption. Just Bhuto and Boulder shaped rock could be sized from raw materials approximately 1000 cuft/day.

Difference between ¾″ (Bhuto) and ¾″ (Boulder): The crushed rock ¾″ (Bhuto) and ¾″ (Boulder) are same in size but their shape are different. ¾″ (Bhuto) are more angular than ¾″ (Boulder). The roundness is greater in ¾″ (Boulder) than ¾″ (Bhuto). The ¾″ (Boulder) is much stronger than any other sized & shaped rock. The prize of ¾″ (Boulder) is also high. According to consumer demands the owner of crusher supply to them desired shape of rock. The operator of crusher must have to be skilled. Because millions of productions are being continuously operated by them.

Table (1) Application and Characteristics of different size

crushed rock

However it has known that weathering is the mechanism by which rocks are broken up and supplied to the agents that transport the fragments to their new depositional sites. The mechanism of broke down is accomplished by mechanical or physical and chemical means, which often work together and are called mechanical and chemical weathering; this is obtained from Peter K. Link [11]

But in the Luba quarry, here the sizes & shapes of all rocks is the ultimate result of mechanical and chemical weathering.

Yet there are no updated methods being used here, that’s why their production rate from quarry is a bit slow. So by applying more updated methods such as bringing pump, automatic machine can make their project of extracting rocks more worthwhile and fast.

During extraction of rock there have been no risk spotted. But in rainy season when water level rise it may be counted as a bit adverse condition with respect to workers, who extract rocks from quarry. Till now this extraction project is running under hackneyed process & there would not possess any necessary update technology to make this extraction of rock more fluent.

The rock extraction from quarry has been maintaining by local people. Although this is a simple quarry mining but it would be better to possess some expertise to maintain the overall activity.

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 8, August 2013 897

ISSN 2229-5518

Operating cost of crusher

4.2.1 Cost—Benefit scenario at the Luba quarry:

4.2 Economic feasibility Analysis

The main theme of Economic Feasibility analysis is Cost– Benefit analysis. So here the cost — benefit term is analyzed based on capital investment. Here the Cost – Benefit term is analyzed with respect to quarry and rock crushers of this area. In this section all the data are secondary which has been found by conducting questionnaire survey. In all of these calculations, Dollar ($) & Cent (¢) has been used instead of BDT (Taka) with respect to latest currency rate. So here –

1 Dollar/100 Cent = 78 BDT

Benefits are normally two types - these factors are obtained from Whitten, Bentley & Dittman [3], and Satzinger, Jackson & Burd [4]

• Tangible & Intangible

Tangible benefits are being readily quantified $ value, for example:

increased sales of rock

cost/error reductions

increased throughput/efficiency

increased margin on sales

more effective use of staff time

Intangible benefits are difficult to quantify & often it can use to be a catalyst to enhance Tangible benefits imperceptibly. For example -

increased flexibility of running method of extraction

higher quality products/services

better customer relations

improved staff morale

Cost can be divided into two terms – these factors are obtained from Whitten, Bentley & Dittman [3], and Satzinger, Jackson & Burd [4]

• Development cost & Operational cost

Development & Operational cost includes—

Project development cost

Hand tools purchasing cost

Laborer cost

Transportation cost

Fuel cost (for crusher)

All businessmen who engaged with rock business in kanaighat purchase rock from quarry as per cubic feet measurement.

There are mainly two size of rock can be found in quarry, its Local name is —

1) Single (comparatively small in size)

2) Boulder (comparatively large)

The price of Single & Boulder varies on rainy season and Dry season. Businessmen have to their give Royalty & Union-Tax as per cubic feet term. They give the payment of rock to Local workers who can extract rock. Local Union Tax collectors And Royalty collectors are used to collect their taxes from businessmen as per cubic feet term in Kanaighat Luba quarry. So rock businessmen give their taxes according to extraction of rock per cubic feet basis. In the economic analysis section these taxes are included, so here all economic analysis and calculations are considered after giving taxes.

• Royalty : 2.24 cent/cuft = 0.022 Dollar/cuft

• Union tax : 0.32 cent/cuft = 0.003 Dollar/cuft

In the dry season, Businessmen purchase rock from quarry

Single : 0.23$ per cuft [including , Royalty + Union Tax]

Boulder: 0.28$ per cuft [including ,Royalty +Union Tax]

If they sale this rock without crushing, then businessmen can make profit only 0.04/= Dollar per cuft. So the selling price of Single and Double would be—

Single : 0.23 + 0.04 = 0.27 $ per cuft

Boulder : 0.28 + 0.04 = 0.32 $ per cuft

In the rainy season, Businessmen purchase rock from quarry

Single : 0.38 $ per cuft [including, Royalty + Union Tax]

Boulder: 0.51 $ per cuft [including, Royalty+Union Tax]

They usually make only 0.04/= Dollar per cubic feet without crushing rocks, so their selling price would be

Single : 0.38 + 0.04 = 0.42 $ per cuft

Boulder : 0.51 + 0.04 = 0.55 $ per cuft

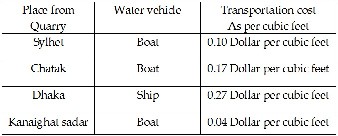

From quarry to different place the transportation media is only river, that’s why different size of boats and ships are also available here for rock transportation purposes. Here transportation cost depends on place to place. The owner of these boats and ships takes payment as per cubic feet term.

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 8, August 2013 898

ISSN 2229-5518

Rocks of Luba quarry has been transporting to three different places – Sylhet, Chatak & Dhaka. Now let see the Transportation cost scenario.

Table (2) Transportation cost scenario

Usually here preliminary the transportation cost is being paid by businessman to boat owners. So to neutralize these transportation costs they include these costs into their selling prices which are being imperceptibly paid by customers. For example - during rainy season, from quarry to Sylhet selling price of—

Single : 0.42 + 0.10 = 0.52 $ per cubic feet

Boulder : 0.55 + 0.10 = 0.65 $ per cubic feet

Here in above 0.10$ included as transportation cost which is imperceptibly paid by customer. That‘s why the profit rate 0.04$ per cubic feet remain constant.

In Rainy season total production from quarry is 200000 cuft/day and in the dry or stock season the total production from quarry is 600000 cuft/day. So the mean production is

400000 cuft/day, when rainy & dry seasons are not taken into consideration. Here the profit by selling rock per cubic feet remain constant at 0.04 $ from quarry. If purchase price of rock in rainy season is Single = 0.38 Dollar/cuft, Boulder

= 0.51 Dollar/cuft, for Simplification purposes we can consider the average price of single and boulder together for further calculations. So the price would be 0.45

Dollar/cuft [including, Royalty + Union Tax]. The

calculation procedure is same for the dry season in quarry,

so here for simplification purposes the cash flow has been applied only for rainy season at the quarry.

Before executing a cash flow analysis for rock business in quarry, compared to the results obtained by Peters, Klaus & Timmerhaus [7], some secondary data need to be fixed to make these calculations easier. These are—

Total production = Total sale = 400000 cuft/day

Taxes (Royalty + Union taxes) = 0.022 + 0.003 =

0.03 $ /cuft

Average purchase price of rock = 0.42+0.03= 0.45

$/cuft [including , Royalty + Union Tax]

Transportation from quarry to Sylhet = 0.10 $/cuft

Profit per cubic feet = 0.04 $/cuft

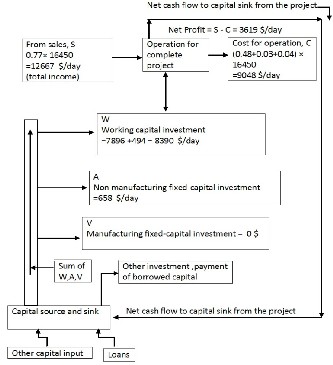

Cash flow for quarry: This is very important to know some specific information for cash flow analysis and these are given below—

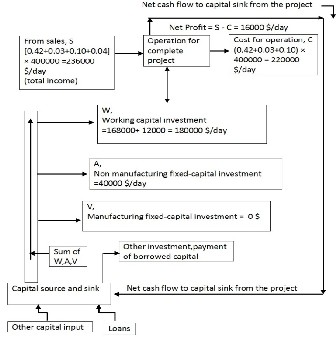

• Manufacturing fixed-capital investment, V = 0 $ (Here Manufacturing fixed-capital investment, V=0 $, in regard of this all capital investments belongs to non manufacturing & working type)

• Non manufacturing fixed –capital investment , A:

Transportation = 400000 × 0.10 = 40000 $/day

• Working capital investment ,W:

Raw material =400000 × 0.42 = 168000 $/day

Taxes (Union Tax Royalty)=400000 × 0.03 = 12000

$/day

Fig. 2: Tree diagram showing cash flow for rock quarry [7]

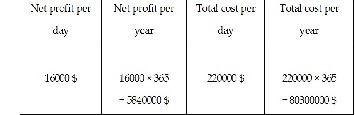

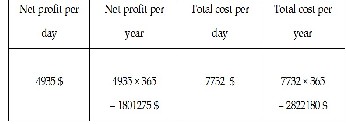

Table (3) Cost – benefit scenario at the quarry

• Return on investment (%) = (Gain from investment—

cost of investment) / cost of investment [8]

= Total profit / Total cost

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 8, August 2013 899

ISSN 2229-5518

Breakeven point

= (5840000/80300000) × 100

= 7.27 %

without crushing. There only boulder size rocks get crush into various shapes and sizes which are encountered in (table 4). Now analyze the cost— benefit scenario with respect to crusher. For the simplification of this analysis it would be better to consider the average production rate of

Per day production = 400000 cuft

Selling price =0.59 $/cuft

Per day production cost = 220000 $

To we keep rock business at no profit-no loss condition, then the amounts of rocks, businessmen have to

Sale = (220000/0.59) cuft/day = 372881 cuft/day [10]

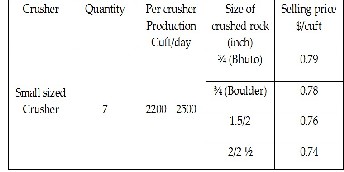

4.2.2 Cost–Benefit scenario at the Crusher Mills: Here in Kanaighat sadar all crushers are small sized .The production of a small size crusher is 2000 – 2500 cuft/day. The total numbers of small size crushers are 7, if we take the mean production as 2350 cuft /day, so according to this the total production by small size crusher is –

• Total production = (2350 × 7) cuft /day = 16450 cuft/day

• And the annual production is = 16450 × 365 = 6004250 cuft/year

Production rates of different Sized crushed rocks: There are 4 different types of crushed rocks are being produced by small sized crusher. ¾″ (Bhuto) and ¾″ (Boulder) are produced 1000 cuft/day and 2/2 ½″ and 1.5/2″ are produced 1200—1500 cuft/day.

Selling price of crushed rock: Rocks are crushed into different required sizes. Their prices are also varying with their sizes. Their required size is ¾″. The size ¾″ (Boulder) is most costly than others. The price of ¾″ (Boulder) is 0.79

$/cuft and the price of ¾″ (Bhuto) is 0.78 $ /cuft. The price

of 1.5/2″ is 0.76 $ /cuft and the price of 2/2 ½″ is 0.74

$/cuft.

Table (4) quantity, production & selling price scenario of crusher Mills

It has known that, Single & Boulder size rocks are generally provide from quarry as raw materials. Here single size rock is very small in size that’s why it is not crushed into various shapes and sizes. People can sale it with its original shape

crusher & average selling price.

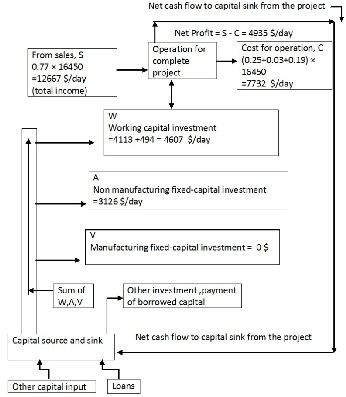

In the dry season: Before executing a cash flow for rock business in the crusher mills, compared to the results obtained by Peters, Klaus & Timmerhaus [7], and some secondary data need to be fixed to make this calculation easier. These are—

Total production=Total sale = 16450 cuft/day

Taxes (Royalty + Union taxes) = 0.022 + 0.003 = 0.03

$/cuft

Purchase price of Boulder = 0.25+0.03= 0.28 $/cuft

[including , Royalty + Union Tax]

Mean selling prize of various crushed rock is =

(0.74+0.76+0.78+0.79) /4 $/cuft = 0.77 $/cuft

Transportation from quarry to Kanaighat sadar = 0.19

$/cuft (via Truck/Lorry )

Cash flow for crusher in the dry season:

This is very important to know some specific information for cash flow analysis and these are given below—

• Manufacturing fixed-capital investment, V = 0 $

Here Manufacturing fixed-capital investment, V=0 $, in regard of this all capital investment are belongs to non manufacturing & working type.

• Non manufacturing fixed–capital investment , A:

Transportation = 16450 × 0.19 = 3126 $/day

• Working capital investment ,W :

Raw material =16450 × 0.25 = 4113 $/day

Taxes (Union Tax+ Royalty)=16450 × 0.03 = 494 $/day

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 8, August 2013 900

ISSN 2229-5518

Before executing a cash flow for rock business in the crusher mills, compared to the results obtained by Peters, Klaus & Timmerhaus [7], and some secondary data need to be fixed to make this calculation easier. These are—

Total production=Total sale = 16450 cuft/day

Taxes (Royalty + Union taxes) = 0.022 + 0.003 = 0.03

$/cuft

Purchase price of Boulder = 0.48+0.03= 0.51 $/cuft

[including , Royalty + Union Tax]

Mean selling price of various crushed rock is =

(0.74+0.76+0.78+0.79) /4 $/cuft = 0.77 $/cuft

Transportation from quarry to Kanaighat sadar = 0.04

$/cuft

Cash flow for crusher in the rainy season:

It is very important to know some specific information for cash flow analysis and these are given below—

Fig. 3: Tree diagram showing cash flow for crusher mills in the dry season [7]

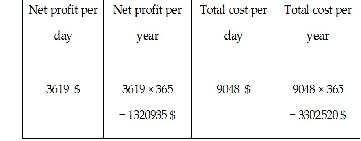

Table (5) Cost – benefit scenario from the crusher mills in the dry season

• Return on investment (%) = (Gain from investment —

cost of investment) / cost of investment [8]

= Total profit / Total cost

= (1801275 / 2822180) × 100

= 63.83 %

Breakeven point

Per day production = 16450 cuft

Mean selling price =0.77 $/cuft

Per day production cost = 7732 $

To we keep rock business at no profit-no loss condition, then the amounts of rocks, businessmen have to sale = (7732/0.77) cuft/day = 10042 cuft/day [10]

In the rainy season:

• Manufacturing fixed-capital investment, V = 0 $ [Here

V=0 $, so all capital investment are belongs to A &W]

• Non manufacturing fixed –capital investment , A:

Transportation = 16450 × 0.04 = 658 $/day

• Working capital investment ,W :

Raw material =16450 × 0.48 = 7896 $/day

Taxes (Union Tax+ Royalty) = 16450 × 0.03 = 494

$/day

Fig. 4: Tree diagram showing cash flow for crusher in the rainy season [7]

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 8, August 2013 901

ISSN 2229-5518

Table (6) Cost – benefit scenario from the crushers in the rainy season

• Return on investment (%) = (Gain from investment —

cost of investment) / cost of investment [8]

= Total profit / Total cost

= (1320935/3302520) × 100

= 40 %

Breakeven point

Per day production = 16450 cuft

Mean selling price = 0.77 $/cuft

Per day production cost = 9048 $

To we keep rock business at no profit-no loss conditions, then the amounts of rocks, businessmen have to sale= (9048/0.77) cuft/day = 11751 cuft/day [10]

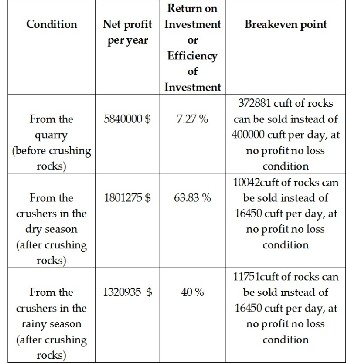

5 RESULTS SUMMARY & INTERPRETATION

In the quarry,

Rock remain as stock = [(400000-372881) ×100]/400000

= 6.78 %

So, (100 - 6.78) % = 93.22 % of extracted rock has to be

sold to keep no profit no loss condition.

In the crusher at dry season,

Rock remain as stock = [(16450-10042) ×100]/16450

= 38.95%

So, (100 – 38.95) % = 61.05 % of extracted rock has to be

sold to keep no profit no loss condition.

In the crusher at rainy season,

Rock remain as stock = [(16450-11751) ×100]/16450

= 28.57%

So, (100 – 28.57) % = 71.43 % of extracted rock has to be sold to keep no profit no loss condition.

From above results it can be said that rock extraction from quarry in Kanaghat Thana is economically feasible & profitable. It is noticeable that selling of rocks after crushing is more profitable, and in regard of this the Efficiency of Investment is higher as well. By selling relatively small amount of crushed rocks, it is possible to gain breakeven point or “no profit no loss” condition. For example in the crusher at dry season, to achieve capital investment or total cost without profit 61.67% of extracted rock has to be sold, in this condition rocks remain as stock about 38.33% for further selling. So it is clear that their benefits worth the costs.

6 RECOMMENDATIONS

1. By developing road transportation facilities people can decrease rock transportation cost.

2. There are 35—40 laborers are required to maintain each crusher production, so authority of crusher mills can attach automatic conveyer belt system to the output of every crusher to carry these crushed rocks, & consequently which could decrease the number of laborers at every crusher mills.

3. Some sort of automatic machines are also able to

decrease investment cost of this project and can make rock extraction more worthwhile, cheap and fast.

4. Government should take necessary steps to improve this commercial site, because Kanaighat rock quarry is a great source of georesource and it can able to play a

great role in constructional purposes according to our national demands.

7 DISCUSSION & CONCLUSION

Luba Rock is known as a building material which can be usually used in construction all over the country. Luba rock quarry in Kanaighat is a massive depositional area of rocks

& it is approximately 140 hectares. Meghalaya of India is

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 8, August 2013 902

ISSN 2229-5518

relatively in higher ground level than Bangladesh, for this | 22. | How much is the selling price of these rocks? |

reason rocks come into the Kanaighat Luba quarry | 23. | How much is the transportation cost? |

especially in the rainy season via high speedy stream. But | 24. | What types of taxes are included here & its amount? |

till now as usual technology have been using here to extract | 25. | Is there any crushing mill? |

these rocks. Local people are extracting these constructional | 26. | How much rocks can be crushed per day? |

rocks by using manual hand tools. However to achieve the | 27. | What type of crushed rock can be found there? |

goal of this project work some questionnaire survey has | 28. | How is the selling price of these crushed rocks? |

been made and some technical & economic analysis has | 29. | What is the amount of rock depositional area? |

been made here as well. In the economic feasibility analysis | 30. | Does the Luba River directly come from Meghalaya? |

section— Cash Flow analysis, Return on investment

analysis & breakeven point analysis are noteworthy.

From those above feasibility study on the prevailing georesources in Kanaighat Thana shows that existing available resource is economically feasible and able to go for the commercial production.

APPENDIX

Questionnaire Survey

To collect necessary data and information there are some questionnaire survey has been made to pep up this project work. All the information is collected from local people & rock businessmen. These are given below—

1. In which regions can we find georesources?

2. What types of georesources have been usually found?

3. What are the sources of these resources?

4. What type of extracting methods are the workers

using?

5. Does it (method) have any environmental impact?

6. What are the applications of these available

georesources?

7. How is their (rocks) economic viability?

8. How is the necessity of this georesources respect to our country?

9. Is it being exported in foreign countries?

10. Does it have any contribution for the prosperity of this village & for local people?

11. In which peobable regions can we get any types of georesources?

12. Is there any oil & gas reservoir which has been technically proved by any oil-gas exploration company?

13. How is the depositional rate of available georesources from their sources?

14. In which season can we get the maximum production of available georesources?

15. How is the reserve of available georesources?

16. Are there any survey records for any kind of resources by any exploration company?

17. What is the main problem in rock quarry?

18. How much rock can be extracted per day from this quarry?

19. What type of measurement based on which

businessmen can purchase rocks from quarry?

20. What type of rock can be found in this quarry?

21. How much is the purchase price of these rocks?

ACKNOWLEDGEMENT

Authors are thankful to the Local people, Local Rock businessmen of kanaighat Thana & Petroleum and mining Engineering Department of Shahjalal University of Science

& Technology, Sylhet, Bangladesh.

REFERENCES:

[1] Collins English Dictionary website, “definition of feasibility study” [online]. http://www. collinsdictionary. com. 2013.

[2] wikipedia, “Feasibility Study“,http://en.m.wikipedia. org/

wiki/Feasibility study. 2013.

[3] J. L. Whitten, L. D. Bentley and K. Dittman, “Systems Analysis and Design Methods,“ McGraw-Hill: Boston, MA, 2004.

[4] J.W. Satzinger, R. B. Jackson, and S. D. Burd, “Object-Oriented

Analysis and Design with the Unified Process.“ Thomson: Boston, MA, 2005.

[5] wikipedia website [online]. http://en.wikipedia.org/ wiki/ Sylhet_District.2013.

[6] Banglapedia, “Kanaighatthana”, http://www. banglapedia.org/

httpdocs/HT/K_0069.HTM. 2006.

[7] Max S. Peters, Klaus D. Timmerhaus “Plant Design & economics

for chemical engineers“, 4th ed, p. 151, New York: Mc Graw-Hill

Inc press, 1991.

[8] Investopedia, “Return on Investment– ROI”. http://www. investopedia.com/terms/r/returnoninvestment.asp. 2013.

[9] The Bangladesh bureau of Statistics website [online],

http://www.bbs.gov.bd. 2010.

[10] wikipedia website [online]. https://en.wikipedia.org/ wiki/

Break-even. 2013.

[11] Peter K. Link, “Basic Petroleum Geology, “ 2nd ed, p. 77, Tulsa:

Oil & Gas consultants International, Inc. 1987.

————————————————

• Isteyak Ahmad- B.Sc Engineer, Petroleum & Mining Engineering

Department, Shahjalal University of Science & Technology, Sylhet-

3114, Bangladesh,

PH: +8801832889511,

Email: isteyakrahi@gmail.com

• Mohammad Shahedul Hossain- Assistant Professor, Petroleum & Mining Engineering Department, Shahjalal University of Science & Technology, Sylhet- 3114, Bangladesh,

PH: +8801712537886, Email:shahedulhossain@gmail.com

IJSER © 2013 http://www.ijser.org