International Journal of Scientific & Engineering Research, Volume 5, Issue 2, February-2014 742

ISSN 2229-5518

Comparative Analysis of Proposed ANN Model of Hybrid Network with Existing Models

1. R.Rajalakshmi, 2. Dr.S.Thirunirai Senthil, MCA,M.Phil., Ph.D.,

Abstract — Prediction of stock market returns is an important issue in finance. Artificial neural networks have been used in stock market for prediction during the last decade. Studies were performed for the prediction of stock index values and daily direction of change in the index. This work compares three different ANN models and makes these models to train with the past historical data of 10 years stock price datasets of HCL and the prediction of future stock price of HCL has been found. The Root Mean Square error (RMSE) and Mean Absolute Performance (MAPE) of two metrics are used to calculate the error rate value of each model. Multilayer perceptron (MLP) with Back propagation and Flexible Neural Tree (FNT) has higher error rate than the proposed Hybrid Network model (Functional Link Fuzzy Logic Neural Model). Implementation of Fuzzy Logic in Functional Link Artificial Neural Network Model (FLANN) reduces the convergence problem and fuzzy values gives higher accuracy in the output layer. As from the comparative study of three models result states that the Hybrid Network Model (FLFLN) is the optimal model which has lesser error rate than the existing models.

Keywords — Multiperceptron, Fuzzy Logic, Neural network, stock market

1 INTRODUCTION

Prior to 1974, there had been many attempts to model

A neural network is an interconnected group of nodes, akin to the vast network of neurons in the human brain. An Artificial Neural Network is a mathematical model or computational model based on biological neural networks. Detecting trends and patterns in financial data is of great interest to the business world to support the decision-making process. So far, the primary means of detecting trends and patterns has involved statistical methods such as statistical clustering and regression analysis. The mathematical models associated with these methods for economical forecasting, however, are linear and may fail to forecast the turning points in economic cycles because in many cases the data they model may be highly nonlinear. A new generation of methodologies, including neural networks, knowledge-based systems and genetic algorithms, has attracted attention for analysis of trends and patterns. In particular, neural networks are being used extensively for financial forecasting with stock markets, foreign exchange trading, commodity future trading and bond yields. The recent resurgence of interest in the field of NNs has been inspired by new developments in NN learning algorithms, analog VLSI circuits and parallel processing techniques. One main possibility for the use of artificial neural system is to simulate physical systems that are best expressed by massively parallel networks.

• R. Rajalakshmi is currently pursuing M.Tech (Information

Technology) in PRIST UNIVERSITY, Puducherry. E-mail: rajee.apr20@gmail.com

• Dr.S.Thirunirai Senthil, MCA, P.Phil, Ph.D., is currently working as Professor in PRIST UNIVERSITY, Computer Science Department, Puducherry

events and phenomena via network based techniques.

Probably the most well known of these modeling

methodologies was introduced by the Reverend Thomas

Bayes as early as 1763. Within these models as shown in

Figure 1.1, simple probability or rule-based calculations were

carried out within so-called ‘nodes’ and the results transmitted to other such nodes to create compound models. Vintage network models consist of intelligent nodes communicating through dumb connections. Modern day neural networks consist of dumb nodes or switches that effectively grow connections that embody intelligence. According to the DARPA Neural Network Study “a neural network is a system composed of many simple processing elements operating in parallel whose function is determined by network structure, connection strengths, and the processing performed at computing elements or nodes”.

Figure 1.1: Network vs. Neural Network Models

2 OBJECTIVE OF THE PAPER

IJSER © 2014 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 5, Issue 2, February-2014 743

ISSN 2229-5518

To develop a different ANN models and compare those models with their performance. To implement ANN models on Stock Market exchange for prediction and obtain the optimal model by calculating and comparing the error rate percentage. An easy way to comply with the conference paper formatting requirements is to use this document as a template and simply type your text into it.

3 MOTIVATION

There are several motivations for trying to predict stock market prices. The most basic of these is financial gain. Any system that can consistently pick winners and losers in the dynamic marketplace would make the owner of the system very wealthy. Thus, many individuals including researchers, investment professionals, and average investors are continually looking for this superior system which will yield them high returns.

There is a second motivation in the research and financial communities. It has been proposed in the Efficient Market Hypothesis (EMH) that markets are efficient in that opportunities for profit are discovered so quickly that they cease to be opportunities. The EMH effectively states that no system can continually beat the market because if this system becomes public, everyone will use it, thus negating its potential gain. There has been an ongoing debate about the validity of the EMH, and some researchers attempted to use neural networks to validate their claims. There has been no consensus on the EMH’s validity, but many market observers tend to believe in its weaker forms, and thus are often unwilling to share proprietary investment systems.

Neural networks are used to predict stock market prices because they are able to learn nonlinear mappings between inputs and outputs. Contrary to the EMH, several researchers claim the stock market and other complex systems exhibit chaos. Chaos is a nonlinear deterministic process which only appears random because it cannot be easily expressed. With the neural networks’ ability to learn nonlinear, chaotic systems, it may be possible to outperform traditional analysis and other computer-based methods.

4 MULTI LAYER PERCEPTRON

To be able to solve nonlinearly separable problems, a number of neurons are connected in layers to build a multilayer perceptron. Each of the perceptrons is used to identify small linearly separable sections of the inputs. Outputs of the perceptrons are combined into another perceptron to produce the final output. The hard-limiting (step) function used for producing the output prevents information on the real inputs flowing on to inner neurons. To solve this problem, the step function is replaced with a continuous function- usually the sigmoid function.

5 FUNCTIONAL LINK ARTIFICIAL NEURAL NETWORK

The Functional Link or FLANN architecture based model to predict the movements of prices in the stock indices. It has been shown that this network may be conveniently used for functional approximation and pattern classification with faster convergence rate and lesser computational load than a Multi-Layer Perceptron (MLP) structure. The structure of the FLANN is fairly simple. It is a flat net without any need for a hidden layer. Therefore, the computation as well as learning algorithm used in this network is simple. The functional expansion of the input to the network effectively increases the dimensionality of the input vector and hence the hyper-planes generated by the FLANN provide greater discrimination capability in the input pattern space.

Nowadays vast amounts of capital are traded through the Stock Markets all around the world. National economies are strongly linked and heavily influenced of the performance of their Stock Markets. Moreover, recently the Markets have become a more accessible investment tool, not only for strategic investors but for common people as well. Consequently they are not only related to macroeconomic parameters, but they influence everyday life in a more direct way. Therefore they constitute a mechanism which has important and direct social impacts. The characteristic that all Stock Markets have in common is the uncertainty, which is related with their short and long-term future state. This feature is undesirable for the investor but it is also unavoidable whenever the Stock Market is selected as the investment tool. The best that one can do is to try to reduce this uncertainty. Stock Market Prediction (or Forecasting) is one of the instruments in this process. The financial market is a complex, evolutionary, and non-linear dynamical system. The field of financial forecasting is characterized by data intensity, noise, non-stationary, unstructured nature, high degree of uncertainty, and hidden relationships. Many factors interact in finance fluctuation based on political events, general economic conditions, and traders’ expectations. Therefore, predicting finance market price movements is quite difficult. Increasingly, according to academic investigations, movements in market prices are not random. Rather, they behave in a highly non-linear, dynamic manner.

IJSER © 2014 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 5, Issue 2, February-2014 744

ISSN 2229-5518

In literature a number of different methods have been applied in order to predict Stock Market returns. These methods can be grouped in four major categories:

i) Technical Analysis Methods,

ii) Fundamental Analysis Methods,

iii) Traditional Time Series

Forecasting and Machine

Learning Methods.

Technical analysts, known as chartists, attempt to predict the market by tracing patterns that come from the study of charts which describe historic data of the market. Fundamental analysts study the intrinsic value of a stock and they invest on it if they estimate that its current value is lower that it’s intrinsic value. In Traditional Time Series forecasting an attempt to create linear prediction models to trace patterns in historic data takes place. These linear models are divided in two categories: the univariate and the multivariate regression models, depending on whether they use one of more variables to approximate the Stock Market time series. There are a number of methods that have been developed under the common label Machine Learning and these methods use a set of samples and try to trace patterns in it (linear or non-linear) in order to approximate the underlying function that generated the data. Finally, artificial Neural Network has taken a great prominent role in forecasting the share market and a number of researches haven done in this area.

6 ANALYSIS OF DATASETS AND INPUT SELECTION

The historical data is obtained from the National Stock Exchange. The whole data set covers a total of 1,200 pairs of data for about eight years from January 2000 to December 2007. The totals of 676 pairs of datasets are taken for observations. The data set is divided into two parts. The first part consists 640 pairs of observations are used to determine the specifications of the models and parameters. The second part contains 36 pairs of observations which are reserved for evaluation and comparison of performances among forecasting models. It is often a difficult task to select important variables for a forecasting or classification problem, especially when the feature space is large.

The input selection is done initially with the input variables are selected to formulate the model with same probabilities, the variable which have more contribution to the objective function will be enhanced and have high opportunity to survive in the next generation and evolutionary operators provide a input selection method by which the FNT models select appropriate variable automatically. The table lists out the variables and the description for those variables.

Input Variables

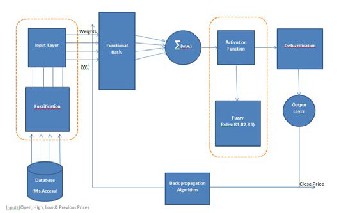

FUNCTIONAL LINK FUZZY LOGIC NEURAL NETWORK

Figure 6.1: Fuzzy Logic implementation in FLANN Model

Various system identifications, control of nonlinear systems, noise cancellation and image classification systems have been reported in recent times. These experiments have proven the ability of FLANN to give out satisfactory results to problems with highly non-linear and dynamic data. Further the ability of the FLANN architecture based model to predict stock index movements, both for short term (next day) and medium term (one month and two months) prediction using statistical parameters consisting of well-known technical indicators based on historical index data is shown and analyzed. The Proposed Hybrid Functional Link Fuzzy Logic Neural model (FLFNM) uses the nonlinear combination of input variables. The proposed hybrid model architecture is explained below:

IJSER © 2014 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 5, Issue 2, February-2014 745

ISSN 2229-5518

1.The raw datasets are stored in database (.mdb); the

fuzzification process gets started with the raw datasets. This 18 process involves, crisp value conversion that helps to train the 16 neural network with greater accuracy. 14

2.After the fuzzification process, the converted crisp 12

input values are moved to neural network input layer. 10

3.The input layer has nodes that collects the inputs from 8

fuzzification block and pass the inputs to neuron. 6

4.The functional expansion block (neuron- FLANN 4

model) collects the inputs and multiplied with weights 2

ERROR RATE FOR H

assigned between input layer and functional expansion block.

5.The multiplied inputs are summed collectively and forwarded to activation function.

6.The activation function used in this neuron is (tanh

function), this function gets the summed inputs and coverts it to 0 to 1 range using tanh mathematical function.

7.After range conversion over, the value is passed to

fuzzy sets to check which operation will perform.

8.The fuzzy sets has three relations

a.If (Value<0) then tomorrow close price value is less than today’s price (loss).

b.If (Value<=0.5 && Value>=0) then tomorrow close price value remains same as today’s price (no loss).

c.If (Value>0.5) then tomorrow close price value is

greater than today’s price (profit).

9.Finally the satisfied condition throws the output to the neural network output layer.

10.In training phase, the error will be back propagated

using back propagation algorithm.

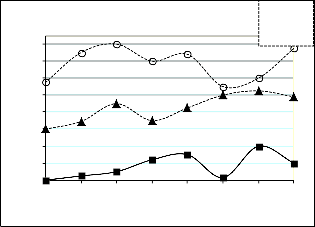

COMPARISON OF THREE MODELS

2000 2001 2002 2003 2004 2005 2006 2007

YEAR

Fi g 6: Comparative Error Rate for Three Models

7 CONCLUSION

The proposed ANN model of FLFLN and existing ANN Model of MLP & FNT has been studied and implemented the case study of stock market exchange. The result of proposed model of FLFLN model compare with existing model of MLP & FNT and conclude that Proposed Hybrid FLFLN ANN model is more accuracy than MLP & FNT.

8 FUTURE ENHANCEMENT

Present work can be extended to predict trends of several stock indices across the globe. For accurate prediction influencing factors from both technical and fundamental analysis should be taken as it would deal with market details as well as the company’s details which would inturn make better predictions. Our project is an attempt to work on the efficiency of three ANN models in predicting stock prices in the Indian context and with respect to interpolation and can be further extended for extrapolation. The results suggest that the efficiency of proposed hybrid model (FLFLN) is more than MLP & FNT for tomorrow’s trend today accurately.

9 REFERENCES

[1] Pratap kishore padhiary, Ambika prasad mishra,

”Development of improved artificial neural network model for stock market prediction”, International journal of engineering science and technology (ijest), ISSN : 0975-5462 vol. 3 no. 2, pp. 458- 465, feb 2011.

[2] Chakravarty, S. Dash, P.K., “Forecasting stock market indices using hybrid network “, in the proceeding of the IEEE Transactions of Neural Network, pp. 1225 –

1230, Dec. 2009.

IJSER © 2014 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 5, Issue 2, February-2014 746

ISSN 2229-5518

[3] J. Kumaran @ Kumar and Poonguzhali,” Artificial Neural Network Technique for Forecasting: Neural Tree and Necessary Number of Hidden Units”, International Journal of Recent Trends in Engineering, Vol. 1, No. 2, pp. 625-632, May 2009.

[4] Vahid Aeinfar,Hoorieh Mazdarani,Fatemeh Deregeh, Mohsen Hayati, Mehrdad Payandelr, “Multilayer Perceptron Neural Network with Supervised Training Method for Diagnosis and Predicting Blood Disorder and Cancer”, IEEE International Symposium on Industrial Electronics (ISlE 2009), pp. 115-122, July 5-

8, 2009.

[5] Mini Qi and G. Peter Zhang “Trend Time-Series Modeling and Forecasting With Neural Networks” in the proceeding of the IEEE Transaction on Neural Networks, Vol.19. No.5, pp. 725-732, MAY 2008.

[6] Ramnik Arora, “Artificial Neural Networks for Forecasting Stock Price”, Computers and Operations Research, pp. 35-42, 2008.

[7] Stephan Trenn “Multilayer Perceptrons: Approximation Order and Necessary Number of Hidden Units” in the proceeding of the IEEE Transaction on Neural Networks, Vol.19. No.5, pp.

311-319, MAY 2008.

[8] Manna Majumder and MD Anwar Hussian, “Forecasting Of Indian Stock Market Index Using Artificial Neural Network”, Information Science, pp. 98- 105, 2007.

[9] Yuehui Chen, Bo Yang and Ajith Abraham, “Flexible neural trees ensemble for stock index modeling”, in the proceeding of the Neurocomputing conference, pp. 145-152, October 2006.

[10] Yuehui Chen, Bo Yang, Jiwen Dong and Ajith Abraham “Time-series forecasting using flexible neural tree model” Information Science, Elsevier, pp.

411-419, Nov 2004.

[11] Birgul Egeli, Meltem Ozturan and Bertan Badur, “Stock Market Prediction Using Artificial Neural Networks”, in the proceeding of IEEE Transaction of Neural Networks, pp. 254-263, Jan 2000.

[12] Drossu, R., and Obradovic, Z., “Rapid Design of Neural Networks for Time Series Prediction”, in the proceeding of the IEEE Computational Science & Engineering, pp. 116-122, Mar 1996.

[13] K. Hornik, M. Stinchcombe, and H. White, “Multilayer feed forward networks are universal approximators,” in the proceeding of the IEEE

Transaction on Neural Networks, vol. 2, no. 5, pp.

359–366, Oct 1995.

[14] Clarence N.W. Tan and Gerhard E. Wittig, “A Study of the Parameters of a Back propagation Stock Price Prediction Model”, in the Proceedings of the First International Two-Stream Conference on Artificial Neural Networks and Expert Systems, pp. 288-

291,1993.

[15] M. Leshno, V. Y. Lin, A. Pinkus, and S. Schocken, “Multilayer feed forward networks with a no polynomial activation function can approximate any function,” in the proceeding of the IEEE Transaction on Neural Networks, vol. 6, no. 6, pp. 861–867, Aug

1993.

[16] Schumann and M, Lohrbach, T, “Comparing artificial neural networks with statistical methods within the field of stock market prediction”, in the proceeding of the International Conference on System Sciences, Volume IV, pp. 597 – 606, Jan. 1993.

[17] K. Hornik, “Approximation capabilities of multilayer feed forward networks,” in the proceeding of the IEEE Transaction on Neural Networks, vol. 4, no. 2, pp. 251–257, Jul 1991.

IJSER © 2014 http://www.ijser.org