International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 232

ISSN 2229-5518

Abstract

Sustainability analysis of public

debt in Albania

D itj o na KU LE P hD st ude nt , Prof. Assoc. Dr. Doriana MATRAKU (Dervishi) 1,

One of the most delicate and the most debated argument recently in Albania is public debt which has reached its maximum level in this moment. The aim problem is the current debt crisis that the Euro zone countries are experiencing. The importance of debt is great not only because it supports economic growth, but it creates vulnerabilities could lead to the destruction of public finance balances. The objective of debt sustainability analysis is to evaluat e the ability of a country to finance its political agenda and to serve subsequent debt without major adjustments, which may affect macroeconomic stability. The purpose of this an alysis is to highlight whether the high level of debt is serving to boost economic growth or has already become a burden on the economy.

In the first section of this paper will initially present theoretical aspects of debt related to its role in economic development and sustainability. The first contributions in the sustainability of fiscal policy analysis are classic authors like Hume, Smith and Ricardo, who analyzed public debt in terms of overall effects on the economy. The analysis is focused on the comparison of taxes and public spending deficit financing, which are considered as an exogenous variable. Tot al debt sustainability will be analyzed further by comparing other developing countries as well as seeing the performance indicators. Finally, it will focus on the effects of debt on economic development by comparing two indicators: the cost of debt with the level of investment and the real effects of the crisis in finance.

An important question in fiscal policy is: can high levels of debt reduce the growth? Without debt countries are poor and stay like that. Borrowing allows individuals to facilitate their consumption in terms of variable income, allows firms to facilitate investment and production in variable sales conditions and allows the government to ease the tax burden for individuals in terms of variable costs. So borrowing improves the allocation of capital in the economy. Public debt provides liquidity, which contribute to the easing of credit conditions for firms and consumers, resulting in increased private investment.

Index terms public debt, sustainability, analyses, indicators of debt

1.1 Debt role in econIomic JdevelopmeSnt ER

—————————— ——————————

1 Theoretical Background

Early contributions of sustainability of fiscal policy analysis are related to classic authors as Hume, Smith and Ricardo, who analyzed public debt in terms of overall effects on the economy. The initial analysis was focused on the comparison of taxes and public spending deficit financing, which the latter considered as an exogenous variable. According to the traditional view, the budget deficit increases aggregate demand and stimulates the growth of production in the short term, but reduces capital and reduces long-term economic growth rates. While Ricardo view was called “Ricardian equivalence” the budget deficit has none of these effects because consumers realize that this deficit means a tax burden in the future. There are three reasons why the budget deficit or surplus is the inevitable result of fiscal policy:

1) Stabilization-a deficit or surplus can help stabilize the economy. When the economy is in recession, taxes automatically fall and transfers automatically rise. Despite these automatic stabilizers helps the economy they bring a budget deficit. A balanced budget will require raising taxes and reducing deepening transfers,

and this will create more economic decline.

2) The fiscal burden - a budget deficit or surplus can be used to reduce the distortion of incentives caused by the tax system. Fiscal burden is a cost to society, which discourages economic activity. To minimize this cost kept stable tax rate. Therefore, a budget deficit is needed to ease the fiscal burden in terms of a recession.

3) Redistribution between generations - a budget deficit can be used for shifting the tax burden from the current generation to the next one [1]. Mankiw N.G (2001)

An important question about fiscal policy is: did the high levels of debt reduce growth? [2]. Without debt countries are poor and stay like that. Borrowing allows individuals to facilitate their consumption in terms of variable income, allows firms to facilitate investment and production in variable sales conditions and allows the government to ease the tax burden for individuals in terms of variable costs. So borrowing improves the allocation of capital in the economy. Public debt provides liquidity, which contribute to the easing of

1 Lecturer of Economics, Economics D epartment, Fa culty of Economy, Tirana University.

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 233

ISSN 2229-5518

credit conditions for firms and consumers, resulting in

increased private investment [3].

History teaches us that borrowing can create vulnerabilities. When the ratio of debt / GDP grows beyond a certain level, financial crises are more likely to occur. Debt accumulation involves a certain risk. As the level of debt increases, the ability of borrowers to pay becomes more sensitive to declining revenues, the decline in sales, increase of interest rate. High levels of nominal debt mean volatility, financial fragility and drop of growth rates. Public sector capacity to borrow is not unlimited. In the case of a crisis, the government's ability to intervene depends on the amount of debt that it has accumulated already, so its fiscal capacity-the ability to increase revenues from taxes, to serve and pay off debt [4].

This means that high levels of debt limit government functions. There is a certain level at which the debt becomes excessive. This level of government debt is accounted about 85% of GDP. We can say that low levels of debt are a source of economic growth and

stability. High levels increase volatility and reduce

requires the provision of interest rates for domestic

debt and exchange rate for external debt. In the case of absence as refinancing, this does not mean that the debt is unsustainable, but is simply a liquidity issue. Lack of liquidity could lead to insolvency, although the debt may be established according to the above definitions. When increasing interest rates exceed the rate of economic growth, the process of debt accumulation is unsustainable. So there are two difficulties: firstly, small changes in interest and GDP can turn debt from stable to unstable and secondly, when these rates are close to each other, economic shock can have powerful effects on the performance of debt [5].

There is not a theory about debt sustainability, and therefore should be considered a wide range of factors such as: the history of debt payments, the nature of government and institutions, the level of GDP, exports, changes in interest rates, exchange rates, income tax etc.

2. Analysis on public debt sustainability

economic growth.

There is not a definition about the optimal level of debt. The level of debt that must be considered

1.2 Sustainability of public debt

Sustainability of public debt is a matter of debate. Its importance is great, but there is no clear definition or a precise measurement, as in the case of inflation or other macroeconomic indicators. For this reason, debt sustainability is an imprecise indicator to serve as a tool for the design of fiscal policy.

Sustainability as an IMF definition is: "The debt is sustainable when it meets the conditions of payment with a great accuracy .... based data costs." Debt solvency is achieved when future surpluses would be sufficient to pay off debt, principal and interest. What is important is the level of future balances because it may happen that higher debts are settled and small to be unstable. For example, Britain's debt in 2004 has reached 270%, but was stable in terms of solvency. Therefore, the concept of sustainability should be seen in a broader perspective, based on long term periods and event that has not yet occurred.

Another aspect that should be taken into account in the theoretical treatment of stability is related to the fact that the debt should be measured in accordance with the size of the country. For this reason we measure the ratio of debt with GDP. The source of income for its finance is directly related to the ability of government to collect taxes. Sustainability relates to change in the case of debt refinancing costs. This

sustainable change significantly in all countries. Debt level primarily depends on the level of debt stock an d the potential rate of growth. Secondly, countries differ in their ability to generate trade and budget surpluses needed to fund the debt [6 ].

2.1 The level of debt in comparison to developing countries

To determine a sustainable level of debt can rely two treatments: first, we compare the level of debt in Albania with other emerging countries countries, and second, we examine the empirical literature on debt sustainability. We have examined data on public debt as a percentage of GDP for eight emerging countries as average level (Bosnia & Herzegovina, Bulgaria, Croatia, Hungary, Macedonia, Romania, Serbia and Turkey) and Albania.

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 234

ISSN 2229-5518

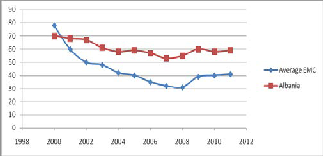

Figure 1. Public debt for EMC and Albania (as % of GDP)

Source: IMF (2012)

The average debt ratio for developing countries has declined most during this period than that of Albania, deepening even more the gap. Given the low level of income and vulnerability to economic shocks, the debt ratio should not be higher than the average of developing countries, which in 2011 means no more than 41% of GDP. Given this standard conclude that its reduction is needed.

In 2003, the IMF undertook a detailed study on the

government expenditure and 5% of GDP. In this case

the country has a better indicator, interest costs are less than 3% of GDP and 10% of total expenditure. This is due to borrowing on concessionary terms, but with increased borrowing at market rates, these indicators will deteriorate.

4) the sensitivity of the debt ratio to changes in the exchange rate. With a large debt issued in foreign currency in developing countries, occur immediately and significantly depending on external factors. This part of the debt issued in foreign currency in Albania to total public debt is lower than the average of developing countries [7].

2.2 Performance of the debt indicators

Public debt may be issued within the country and held by residents (internal debt) or by non-residents (foreign debt). The chart below presents the development of the structure of the debt stock. As can be seen the level of debt stock to GDP during this period remained at high levels, over 50% of GDP. In 2000, despite the fact that

IJSER

sustainability of public debt in developing countries,

noting to what debt developing countries could not

afford to pay and how fiscal policy was responding to different levels of debt. The results showed that while the level of public debt in insolvency period differed significantly. In 55% of countries with insolvency, debt level was below the limit of 60% of the Maastricht criteria and in 35% of cases was less than 40% of GDP. Almost half of insolvency cases occurred in countries with a lower debt ratio or as Albania. Again this conclusion, it is a signal to reduce the level of debt. When using the results of debt sustainability in developing countries should be taken into account several factors:

1) relatively low income in relation to GDP in developing countries, which makes it more difficult to service public debt. IMF in 2003 estimated an average rate of 27% of the revenue to GDP for these countries, a level similar to that in Bangladesh.

2) high volatility in revenue collection, reflects and macroeconomic volatility in these countries. For the period 1996-2008 the index of revenue was 6.7%, ranking Albania in a middle position compared with the other countries of the region. In recent years this index has decreased, reflecting the greater macroeconomic stability.

3) interest costs in developing countries are high and show a high level of risk and economic volatility refle cting market conditions in these countries. The IMF estimated that the average interest costs were 17% of

revenues from privatization were high (privatization of

the National Commercial Bank), budget revenues were

lower than costs and hence costs and investments were financed not only by privatization, but of debt. In 2001, privatization was increased by 43% and financed 30% of the deficit that year, reducing the borrowing for this year.

Other two years were characterized by lower income from privatizations and an increase in the l evel of debt. In 2004, it was privatized former Savings Bank, which enabled the management of deficit and debt reduction. In 2005 -2006 the privatization process was stopped.

However, in 2007 there was a reduction in the debt stock as a result of the reduction of domestic borrowing needs due to privatization receipts (privatization of state-owned company "Albtelecom") and nominal GDP growth [8].

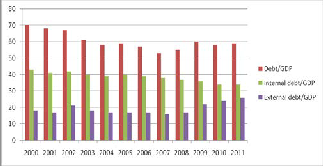

At the end of 2007 there is a tendency to increase the debt stock. Based on Figure 2, it turns out that has changed the structure of the debt stock. The share of domestic versus foreign debt since the end of 2007, reflecting the strategy of the state to provide capital in foreign markets. New loans to finance projects dealt with commercial interests given that Albania is considered a middle-income country.

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 235

ISSN 2229-5518

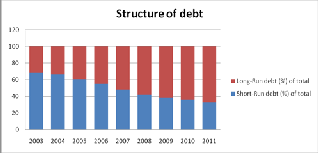

According to the study conducted by Open Data Albania on debt maturity structure, it is shown that during the period 2003-2011 has changed the share of short-term versus long-term debt. This report relates to the strategy followed by the Ministry of Finance on the issuance of long-term debt instruments.

Figure 2. The tendency of the debt in % of GDP

Source: MF (2011) [9].

The public debt stock has increased in recent years as a result of the economic crisis. Income gathered did not meet the government's request for money, which was

forced to borrow to cover investment costs. During the

2007-2008 costs increased significantly as a result of

the construction of the Durres-Kukes road and other investments in 2009 as the election period. Increased in public spending was made with the intention of depreciation of the crisis. Increased in debt stock also

came as a result of increased wages and interest

Figure 3. The structure of the debt.

Source: ODA (2011)

Domestic debt is mainly composed of treasury bills, while the long-term by 2 and 5-year bonds. In 2007 was issued for the first time 7-year bond. Domestic debt

is almost all short and its average maturity is 0.8 years,

IJSER

expense, in terms of a lower growth rate. In 2010, for

the first time were included in the stock of public debt

obligation s of local governments, which are estimated

to be 0.01% of GDP. Also in 2010 took place the first Albanian Eurobond issuance in order to reduce the cost of public debt. Its issuance were used to repay the loan association in 2009 and to finance public investment. This led the debt portfolio diversification. Debt stock rises, so high levels of it have put in danger the stability in the conditions of the euro zone crisis [10]. According to two debt rating agencies, Albanian debt is presented with B + by Standard & Poor's and B1 by Moody's, which are indicators of high risk for investors. These indicators have a significant impact on the high rates of interest on loans and treasury bills issued to finance state debt [ 11 ].

Under these conditions, when interest expenses occupy an important part in the budget, what is expected is the increase in the ratio of debt stock as government borrows to pay interest. Deficit expansion will bring an increase in public debt to other years if not offset by a positive effect between economic growth and the interest rate on the debt. Only with a growth rate of over 5% of GDP can ensure debt sustainability and not to enter into a so-called debt crisis. Looking at the performance of this indicator in recent years and in terms of an economic crisis that has already begun to touch our country, the achievement of this goal seems difficult.

it means that he should refinance within a year.

External debt is long term, given that until 2005 were taken with long-term soft loans for investment projects maturity and has a maturity of 11 years. Eurobond issued in 2010 has a maturity of 5 years. Orientation towards long-term instrument borrowing has reduced the need for refinancing favoring debt repayment profile, but has increased its costs (lower liquidity means higher interest payments) [12].

By issuing currency, 59% of the stock is ALL and 41% in foreign currency. The ratio of debt service to income tax shows the government's ability to pay debt service with internal resources. The minimum level of this ratio for developing countries suggested by the IMF hovers at 25% -35% [13].

In Albania about 18% of revenue collected from taxes go to interest payments. Although the share of income used to cover the interest for the period 2000-2011 is below the limit set by the IMF, it is consistent with the size of the economy and our country's modest ability to repay debt payments.

2.3 Analysis of external debt

To assess the sustainability of public debt is important to analyze the sustainability of external debt. He is regarded as an important element of macroeconomic management, which can bring positive effects on economic growth, but can also lead to financial crisis. External debt allows a higher spending level that

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 236

ISSN 2229-5518

which can be met only by internal resources.

-External debt indicators

Principal holders of foreign debt of our country are the World Bank with about 800 million euros, which are used for infrastructure projects, private creditors

721mln euro Eurobond buyers with about 300ml euro. About 25% of the total public debt is external debt. Structure of external debt based currency issuance for 2011 is 69.8% in EUR and 19.6% in USD. About 2/3 of the external debt consists of debt in Euro. Increasing the ratio euro against other currencies brings increased risk of exchange rate and rising cost of debt if the Euro strengthened

External commercial borrowing has contributed to the growth of the share of external debt with variable interest, with only 75.6% of the stock of external debt with fixed interest. On the other hand is reduced and external debt maturity to 6.8 years, compared with the average maturity of 11.4 years [14].

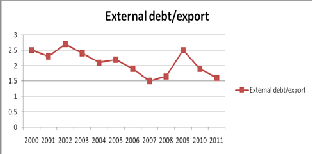

Index of the ratio of external debt to exports is an important indicator of economic capacity to repay

foreign debt payments. Based on the classification of

the IMF regarding the sustainability of external debt as a percentage of exports, which in Albania is 200%, we can say that must be followed strong macroeconomic policies [16].

Conclusion

From this analysis of public debt sustainability concluded that:

1 - Albania debt level for the period 2000-2011 is higher than the average for developing countries

2 - The need to improve the level of these indicators: interest expense, fiscal deficit and the rate of economic growth, in order not to be affected poor balances that held debt sustainability and not to enter into what is called debt crisis.

3 - Borrowing orientation towards long-term instrument has reduced the need for refinancing favoring debt repayment profile, but has increased its costs.

4 - About 2/3 of the external debt is issued in the euro

IJSER

external debt payments provided currency income

from exports. A ratio less than 1 suggests that the debt can be settled quickly, ideally in less than a year. The higher this ratio, the less it is able to repay external debt country export revenues [15].

We can conclude that our country has a foreign debt almost double compared to exports. So, we must ensure once again double the amount of exports to repay foreign debt. This report for the period 2000-

2011 ranges from 1.5-2.6. So, we need a period of several years to repay foreign debt. It is even more difficult in terms of a deep trade deficit as a result of the lack of domestic production, but also the reduction of foreign trade in terms of the economic crisis in the eurozone.

Figure 4. External debt indicators

Source: MF (2011)

In this situation it is important to stimulate the most representative sectors of the economy, to increase the amount of exports and the country's capacity to repay

which leads to increased exchange rate risk.

5 - The ratio of external debt to exports is high, indicating low capacity of the economy to repay foreign debt. In this situation it is important to stimulate the most representative sectors of the economy, to increase the amount of exports and the country's ability to repay foreign debt payments.

6 - The cost of debt is comparable to the level of investment in the economy. Public debt is within the limits of his return to a burden on the economy. Should pursue a stronger macroeconomic management, to stimulate economy.

REFERENCES

[1]. Mankiw N.G (2001), "U.S. Monetary Policy During the

1990s," NBER Working Papers 8471, National Bureau of Economic

Research, Inc.

[2]. Panizza U., Presbitero F A. (2012), Public Debt and Economic

Growth: Is there a causal effect?, MoFiR Working Paper, No. 65

[3]. Barro, Robert J., 1979. "On the Determination of the Public Debt," Scholarly Articles 3451400, Harvard University Department of Economics.

[4]. “The real effect s of debt”, Stephen G Cecchetti, M S Mohanty and Fabrizio Zampolli, September 2011.

[5]. Wyplosz Ch.(2007), Debt Sustainability Assessment: The FMN Approach and Alternatives, HEI Working mic growth and increase debt solvency.paper No.03, Graduate Institute of International Studies

[6 ]. Akyuz Y. (2007), Debt Sustainability in Emerging Markets: A

critical Appraisal, DESA Working paper No.

[7]. FMN (2010), Jonas J., Fiscal Objectives in the Post IMF Program

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 237

ISSN 2229-5518

World: The Case of Albania

[8]. ODA(2012), Privatizimet në Shqipëri 1993-2010 nëpërmjet shifrave [9]. Ministry of Finance (2011), Strategjia e Borxhit Publik 2011-201, [10]. Ministry of Finance (2012), Statement of the Ministry of Finance

on the occasion of the first Eurobond issuance in the country

[ 11 ] www.moodys.com, www.standardandpoors.com

[12] ODA, (2012), Eurobondi i parë i Shqipërisë dhe Performanca e tij që nga emetimi, http://www. open.data.al/,

ODA (2012), Borxhi Publik I Shqipërisë sipas Afatit të Maturimit, http://www. open.data.al/,

ODA (2012), Cost of debt compared to some fiscal indicators

ODA (2012), Costs, revenues and the state budget deficit

[13] INTOSAI (2010), Debt indicators, http://www.intosai.org/

[14] MF (2011) Ministry of Finance (2011), Fiscal table 2000-2011,

Ministry of Finance (2011), The indicators of debt 2011

[15]World Bank, (2006), Restructuring Public Expenditure to Sustain

Growth, Volumi 1, Raport Nr.36453

[16] IMF (2012), The Joint World Bank–IMF Debt Sustainability Framework for Low-Income Countries, http://www.imf.org/external/np/exr/facts/jdsf.htm

IJSER

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013

ISSN 2229-5518

238

IJSER <S> 2013

http/lwww f!ser org