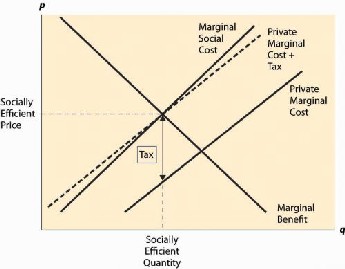

Fig- Pigovian Tax

Pigovian tax is the difference between marginal social cost and the marginal private cost, which equals to the marginal

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 1294

ISSN 2229-5518

Pigovian Tax

And Rethinking the Role of State

Ruchira Boss, Dikshita Baid

Abstract- A Pigovian tax is a tax applied to a m arket ac tivity that gen erates neg ative externalities . T he tax is intended to c orrect the market outc om e. In the pres enc e of neg ative externalities, the s ocial c ost of a market ac tivity is not c overed by the private c ost of the activity. In such a c as e, the market outc om e is not effic ient and may lead to over-c onsumption of the produc t. A Pigovian tax equal to the negative externality is thought to c orrect the mark et outc ome bac k to eff icienc y. Mos t of the critic is m of the Pigovi an tax relat e to the determination of the tax and the implem entation. There are various f ac tors that c an c omplic ate the implementation of Pigovian Tax s uc h as s ocial c os t c annot be measured, the tax am ount should be fixed or politic al f ac tors etc.

Key words- Pigovian Tax, ext ernalities, c oas e theorem, s oc ial cost, private c os t, ec on omic c os t, welf are ec on omics , en vironmental ec onomics, government.

—————————— ——————————

Tax a government can artificially create a cost for such activity - ideally a cost equal to what the price would be

had a market for such activity existed. In a country like

Can imposing Pigovian Tax prove to be beneficial?

According to the Neo-classicals, to correct market failure,

Canada with socialized medicine, the cigarette tax acts as a Pigovian tax - it (more than) raises the revenue necessary to offset the expense to the health care system generated by

IJSER

the first best solution is Perfect competition. But it is an

impossible situation for every economy. Therefore, government interference is the second best solution. Pigovian Tax imposed by the government corrects market failure. It helps to curb negative externalities (e.g. pollution) and eliminate the burden of the society caused by the externalities. Moreover it reduces over-consumption. The paper examines the effects of a Pigovian tax and analyses its degree of effectiveness in an economy.

Before understanding the ingrained mechanism of Pigovian tax, it is necessary to get acquainted with its meaning, nature and significance. Pigovian tax is a kind of tax, which is levied to correct a negative cost that is directly created by the actions of any business firm, but that is not considered in firm’s costs or profits. Also known as ‘sin tax’, it is a tax placed on a negative externality to correct market failure. (1) In the presence of negative externalities, the social cost of a market activity is not covered by the private cost of the activity. In such a case, the market outcome is not efficient and may lead to over-consumption of the product. A Pigovian tax equal to the negative externality is thought to correct the market outcome back to efficiency.

For example, a factory does not take financially take into account the damage their emissions cause to the air, since there is no market for air pollution. By imposing a Pigovian

————————————————

• Ruchira Boss is currently pursuing bachelors degree program in economics in St. Xavier’s College, Jaipur, India E-mail: boss_ruchira@yahoo.in

smoking.

The idea was first put forward by Arthur Cecil Pigou in the year 1912. In his book, The Economics of Welfare, he argued that industrialists seek their own marginal private interest.

Fig- Pigovian Tax

Pigovian tax is the difference between marginal social cost and the marginal private cost, which equals to the marginal

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 1295

ISSN 2229-5518

external cost. The tax level need not equal the marginal external cost at other quantities. The above figure reflects a marginal external cost that is growing as the quantity grows. Nevertheless, the new supply curve created by the addition of the tax intersects demand (the marginal benefit) at the socially efficient quantity. As a result, the new competition equilibrium, taking account of the tax, is efficient. (2) Although this tax works perfect in theory, the practical implementation is very difficult due to a lack of complete information on damage levels (MC).

When Arthur Pigou first came up with the concept, he laid down some set of assumptions, one of which is a perfectly competitive market. Although, in a real market scenario, perfect competition suits the best, but it is completely an unrealistic situation. Monopoly, monopsony and oligopoly are widely seen and recognized. According to Keynesian economics, government intervention is necessary for a stable economy. To internalize the external cost, government needs to intervene and impose taxes. It’s a key measure by which the government maintains stability and equity in the market rather than simply buying and selling of goods and services.

Pigovian tax can be applied to all spheres of production, be

it production of a good (automobile) or service

b) Overhead: Pigovian Tax Anatomy- i. Unregulated result (Q, P)

ii. Socially efficient level of production = Q’

iii. Efficient Pigovian tax = P’-P’’

iv. Tax payment to government (shared by consumer and

producers = P’ACP”

v. Gross benefit from decrease in externality = ADBC

vi. Foregone consumption benefits – i.e., the social cost of

abatement = ABC

vii. Net benefit to society = ADB

Pigovian tax is a part of welfare economics i.e. for the welfare of the society, therein controlling over-consumption and a source of revenue as well as environmental economics i.e. controlling and covering the external cost. Just like every concept can be argued, similarly Pigovian tax was and is one such concept to be argued upon. Roland Coase (1960) propounded that if markets may not secure the optimal amount of externality they “can be very gently

‘nudged’ in that direction without the necessity for full- scale regulatory activity”. (20) Yet again, the Coase theorem faced criticisms too since property rights are not as strictly defined as required by the Coase theorem. Coarse argued that the social harm gets even worse if only the

offender pays for the social harm. It is difficult to calculate

IJSER

(transportation, banking etc). There are some conflicting

views that have been expressed concerning the efficiency of

resource allocation under a Pigovian Tax to control

pollution, when account is taken of the long-run entry of

firms to, and exit of firms from, a competitive polluting

industry. Baumol and Oates (1975, chaps. 4 and 12) argue

that if a Pigovian tax is set equal to the level of marginal

damage (external cost) at the Pareto-optimal level of

pollution the industry will move towards its optimal

pollution level. (15)

a) Applied to the production of a good that has an externality.

the right tax in a world of imperfect Coasian bargains.

Though the concept of imposing tax to correct market failure because of negative externalities was first developed by Arthur Pigou, it was twisted and turned in many ways to see what is best for the economy. Many such concepts were developed such as the Coase theorem, emission trading i.e. cap and trade (Europe), Environmental Protection agencies (U.S.) was formed with the idea of command and control, carbon tax, tradable permits etc. It’s still a topic under debate.

Governments have the option of protecting the environment by means of a ‘direct regulatory’ approach or a more ‘economic’ or market-oriented approach. While the Coase theorem suggests that the market can potentially solve externalities if property rights are clearly assigned and negotiation is feasible, in some cases this is clearly infeasible. E.g. airlines cannot realistically negotiate with individual homeowners for over flight rights to their houses, even though these over flights do create externalities. And it is the state who takes a decision on property rights. Coase theorem states that if the property rights are fully assigned, then the regulatory body should not, in theory, have to be involved. Instead, parties will negotiate among themselves to find the lowest cost solution to correcting the externality.

Since, not always will be parties come to negotiation, and

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 1296

ISSN 2229-5518

hence there is a traditional way to limiting externalities i.e.

‘command and control. This approach sets numerical

quantity limits on activities that have external effects. It is

cumbersome to implement and to get right. Sometimes it is

not feasible or legal to regulate firm’s behaviour at the plant

level, which therefore leads to inefficiencies. While this

method has been undertaken by the US government, the

economies of Europe consider cap and trade as a better

solution. It causes the least polluting firms to do the

majority of the production since its social cost of production

is the lowest.

“There is some debate about whether to quantify externalities if the methods are imperfect. The usual response is that as long as we are honest about the flaws in the numbers, it is better to have some numbers than none” - (Carl V. Phillips, 1999).

Rajeev K. Goel and Edward W. T. Hsieh laid down a two- period model in their research (Durable Emissions and Optimal Pigovian Taxes) where a social planner minimizes social damage by setting the per-unit Pigovian tax on a polluting monopolist. Results show that for a given level of production, the durability of emissions and the socially optimal Pigovian tax are negatively related. This meant

public policy to be implemented by the government to

due to insuperable cognitive limits. Pigou and Friedrich Hayek point out that the assumption that the government can determine the marginal social cost of a negative externality and convert that amount into a monetary value is a weakness of the Pigovian tax.

Therefore, the key difficulty with this tax is calculating what level of applied tax would counterbalance the negative externalities. For example, if gas taxes should be raised purely to offset the social costs of gas use, how high are those social costs be?

Also, even if Pigovian tax is measured properly is not a completely reliable guide to the correct level of the Pigovian tax because, in a world with regulations and efficient transfers, the observed amount of the externality (e.g., pollution) is unlikely to be zero since we will still observe some externalities. Any tax calculation that is determined using the size of the measured externality but that does not consider all regulations and transfers affecting equilibrium will not tell us what the optimal tax should be. The cost should be empirically measured and not just identified and the rate of tax should be best set equal to the per-unit external cost that “spills over” into the society. A tax imposed without such calculations may well be inefficient and redundant.

There is political influence too on the levied tax, in such a

IJSER

achieve socially optimum level of output. (18)

The former guide of About.com, Mike Moffatt, in his article named ‘Pigovian Taxes - Joining the Pigou Club; Promoting Economic Growth and Reducing Externalities’, wrote in favor of Pigovian Tax. He states, ‘One of the uses of taxes is to discourage activity that has negative externalities, or we believe is otherwise economically/socially harmful.’ These taxes also raise revenue for the state. In 2004-2005, the Canadian government collected $16.7 billion in "other" taxes, which were largely Pigovian taxes such as energy taxes and excise taxes on cigarettes and alcohol. (11)

In theory, using Pigovian taxes to correct for what economists call “market failures” is simple. But in practice, it’s not so. The important problem often ignored by advocates of Pigovian taxes is what might be called the “measurement problem” or the “Knowledge problem”. It is recognized as the biggest flaw. Arthur Pigou himself accepted that measurement of Pigovian tax was a flaw. He said "It must be confessed, however, that we seldom know enough to decide in what fields and to what extent the State, on account of [the gaps between private and public costs] could interfere with individual choice." (16) In other words, the economist's blackboard "model" assumes knowledge we don't possess — it's a model with assumed "givens" which are in fact not given to anyone. Friedrich Hayek would argue that this is knowledge which could not be provided as a "given" by any "method" yet discovered,

way that lobbying of government by the polluters may tend

to reduce the level of the tax levied and which would

ultimately reduce the mitigating effect of tax and lead to

increase in production. Instead of accomplishing the goal of

the tax imposed, the burden shifts to the society. Thomas A.

Barthold (1994) argued that in the US in the year 1994 the

actual policy decisions often come from budget

requirements, not concern for the environment. (17) The

taxes do not always parallel raw economic theory because

social benefits and costs are hard to measure. He uses the

1989 Montreal Protocol as an example. President George H. W. Bush signed this protocol that allowed either a permit auction or a tax on ozone-depleting chemicals. Barthold attributes the decision to implement the tax to the pressure

on the Ways and Means committee to come up with more consistent revenue.

“By definition a Pigovian tax hits a concentrated interest to the benefit of society: hardly a way to win political support.” (10)

Alike the other taxes imposed by the government, Pigovian tax gives air to malpractices like black marketing, smuggling and child labour especially if they create large differences in the price of products which are more popular in the neighboring jurisdiction and if the demand for the product increases inspite of the increase in production. A more recent 2002 report by International Labour Organization claims that child labour is significant in Tamil Nadu's fireworks, matches or incense sticks industries. This is because the formal economy and corporate establishments have not expanded to meet the demand, rather home-based production operations have

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 1297

ISSN 2229-5518

mushroomed. This has increased the potential of child labour.

Pigovian Tax imposed by the government is a complex mechanism. It has its societal merits and elementary de- merits. While it covers the cost of negative externalities and eliminates the burden of society, on the same page it may also hamper the growth of industries leading to inefficiency of small industries. Comparing the merits and de-merits on one-to-one count will be illogical and misleading. Therefore, government should be decisive in choosing whether Pigovian tax should be imposed or not, keeping in mind the economic situations, development of the country, environment conditions and other important aspects prevalent in the country.

An example of this kind of tax in action would be the special excise taxes that many states impose upon tobacco products, where the excess social costs might be the increased spending for health care to deal with smoking- related ailments. In Hawai, the government has been greatly increasing their taxes on tobacco products over the last several years. Here, the typical excise tax imposed by the upon a pack of cigarettes has increased from $1.00 in

2000 to $3.20 per pack in 2011, with 60% of that increase having taken place since 2008. During that same time, the

federal excise tax on tobacco has increased from $0.34 per

and cigarette industries whose demand is inelastic in all seasons. But if low income individuals tend to spend a greater proportion of their income on the product with external social cost, such as cigarettes or electricity, then the corresponding Pigovian tax will prove to be regressive.

Any industry possessing any kind of external cost has to pay the tax. Pigovian tax leads to reduction in competitiveness and increase in Welfare. In terms of allocative efficiency, the pollution tax improves the use of resources in the economy.

The point that should be borne in mind is that the key issue is to consider social welfare; competitiveness is, in this context, a minor issue, even an irrelevance. Therefore imposing of Pigovian tax plays an important role and is a key policy of the government. More than market failure, market prices can be distorted by government policies. Possible distortions include: subsidies or tax incentives; direct price controls; foreign exchange controls; and international trade restrictions. Thus, before internalizing environmental externalities, we should investigate whether there is a policy failure affecting the environment. If there

is, then the first step of internalisation should be the

IJSER

pack to $1.01 per pack, and the typical retail price of a pack

of cigarettes in Hawaii has risen from $4.05 in 2000 to $9.27

in 2011.

France is in the process of introducing soda tax on sugary

drinks for 2012 with the aim of discouraging unhealthy

diets and offset the economic costs of obesity. To counter

the problem of children’s easy access to soft drinks, in 2005

the American Beverage Association (the largest US trade

organization for soft drink bottlers) began working to

remove soft drink machines from primary schools, and to

replace soft drinks with healthier beverages such as orange juice or milk.

Though in a monopsony market, where there is only one buyer i.e. there is only one source of demand, it is difficult to impose Pigovian tax since the burden of the tax will be borne by one. Also, taxing consumer products would mean hampering the living standards of the consumers which would therein result in low velocity of the money cycle. While it can be said, that imposing Pigovian tax would lead to reduction in the level of quantity produced of a commodity by an industry. To increase production within the tax constraints, the industries will look upon to new advancements in technologies. This will open doors to research in this field. Also, this shift in technology by commodity producers will cause the externality to be automatically internalised. This approach of internalisation is rather different to that usually suggested, which raises the market price of commodities, the `full-cost pricing of commodities' approach. While big firms may face losses because of decrease in demand and may lead to shut down of small industries, an exception here will be the tobacco

removal of this failure. Though, Pigovian taxes are close to

impossible to implement effectively as the efficient level of

taxation is dependent on estimated damage costs.

Whatever benefits Pigovian taxes might be able to provide,

it will give diminishing returns. Past a certain point, the

government might fail to achieve their objectives of

meaningfully reducing the excess social costs for the ails

they are meant to fix. Instead, these kinds of taxes would appear to simply become a vehicle by which politicians may raise tax revenue by imposing a discriminatory tax policy aimed at an "undesirable" minority.

1. Greg Mankiw, May 3rd, 2010, Pigovian Taxes save lives. http://gregmankiw.blogspot.in/2012/01/pigovian-taxes- save-lives.html (3/11/2012)

2. www. web-books.com/eLibrary/NC/B0/B59/038MB59.html-

3. R.A., Apr 25th 2011, Jim Manzi makes the case for higher petrol taxes (The Economist, WASHINGTON)

4. Apr 1st 2009, 17:42 , Nicotine tax: still a good idea, (The Economist | WASHINGTON), http://www.economist.com/blogs/freeexchange/2009/04/nicot ine_tax_still_a_good_idea

5. Nov 9th 2006, Pigou or NoPigou? An old debate gets a makeover in cyberspace (from the print edition | Finance and economics). http://www.economist.com/node/8150198

6. Sep 18th 2007, 18:05, Not quite Pigou, by The Economist | WASHINGTON, http://www.economist.com/blogs/freeexchange/2007/09/not_ quite_pigou

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 1298

ISSN 2229-5518

7. Aug 7th 2008, 15:31, For the stimulus before he was against it, by The Economist | WASHINGTON

8. M.S. , Feb 24th 2011, The irony of the tragedy of the commons, the Economist (Environmental Regulation)

9. Robert S. main, Butler University, 2010, Simple Pigovian Taxes vs. Emission Fees to Control Negative Externalities: A Pedagogical Note

10. Luigi Zingales, Jun 7th 2010, It's not about revenues

11. Mike Moffatt (former About.com Guide), Pigovian Taxes - Joining the Pigou Club, Promoting Economic Growth and Reducing Externalities.

12. Pigovian taxes, Agnar Sandmo, From The New Palgrave Dictionary of Economics, Second Edition, 2008, Edited by Steven N. Durlauf and Lawrence E. Blume

13. http://www.dictionaryofeconomics.com/article?id=p de2008_P000351> doi:10.1057/9780230226203.1289

14. Wisegeek

15. http://www.jstor.org/discover/10.2307/134738?uid=37

38256&uid=4575783497&uid=2&uid=3&uid=4575783

487&uid=60&sid=21101411252067

16. Pigou, A.C., (1954) Some Aspects of the Welfare

State. Diogenes 7 (6).

17. Barthold, Thomas A. (1994). “Issues in the Design of Environmental Excise Taxes,” The Journal of Economic Perspectives, 8(1): 133-151.

18. Public Finance Preview, July 2004 volume 32

![]()

19. http://www.economist.com/economics/by-invitation/guest- contributions/its_not_about_revenues

20. Sebastian Storfner, 2004, CAN MARKET FORCES SOLVE ENVIRONMENTAL PROBLEMS? NEOCLASSICAL VS. AUSTRIAN ANALYTICS, 5/11/2012

21. 2006, Lecture 7 2006.pdf

22. Political Calculations, march 22,

http://politicalcalculations.blogspot.in/2012/03/failure- of-pigous-taxes.html

23. State of Hawaii. Department of the Attorney General. Report on the Tobacco Enforcement Special Fund. Fiscal Year 2010-

2011. [PDF document ]. 9 January 2012.

IJSER © 2013 http://www.ijser.org