International Journal of Scientific & Engineering Research, Volume 6, Issue 2, February-2015 97

ISSN 2229-5518

Mobile Internet Subscription Trends in

Kenya up to 2014

Omae M. Oteri, Ndungu E. N and Kibet P. L.

Abstract-Mobile phone communication is a sector that has been credited for playing a very vital role in the economy of most countries in the world. It has helped poor people in the rural areas to be able to communicate far within a very short time with minimal costs as opposed to earlier communication methods. The telecommunications market in Kenya was liberalized in 1999 with the licensing of two mobile operators at that time Safaricom Ltd and Celtel Kenya currently Airtel Networks Kenya Ltd while mobile internet communication was introduced in 2008. Since then its subscription has been growing steadily helping the Government to generate more revenues and create job opportunities. The current mobile operators in Kenya are given as Safaricom Ltd, Airtel Networks Kenya Ltd, Essar Telecom Kenya Ltd and Telkom Kenya Ltd (Orange) through which the mobile internet service is provided.

This paper discusses the present market condition of mobile internet in Kenya and the trends in subscription since 2008 when the mobile operators started providing the service. The paper also tries to find out what is likely to happen in a few years to come and provide a set of recommendations based on the analysis. The study was based on extensive literature review and secondary data sources mainly from CAK. The data obtained was analyzed using Matlab and Microsoft excel to obtain the relevant graphical representations as given in results and discussions.

Keywords: Communication, Telecommunication, Mobile phone, Internet, Subscription, Trends.

—————————— ——————————

I. INTRODUCTION

The local sector regulator CAK, as well as a number of

independent research organizations, has studied how Kenyans use their phones. These studies are not conclusive in themselves but give a general insight into the use of mobile phones. According to the latest statistics from CAK, 99% of internet access is from a mobile device (phone, modem, tablets etc). This represents about 19 million internet users in Kenya. Further CAK carried out a National ICT survey in

2011 and the findings report is summarized in the Table 1.

Close to three out of five users used internet for communication while one out of five users engaged in research activities. The data suggests that Kenyans are yet to take full advantage of transacting business on the internet; for example only 2.1 per cent of the users reported having engaged in internet banking. In addition, only 4.4 per cent of users engaged in purchasing or ordering goods and services

Omae M. O, Ndungu E. N, Kibet P. L.School of Electrical, Electronic and Information Engineering, Department of Telecommunication & Information Engineering, JKUAT (phone: +2540722805012;+2540721366349,

+2540724833749 fax: +2546752711; e-mail: m_oteri@yahoo.com,ndunguen@yahoo.com, kibetlp@yahoo.com).

(E-commerce) though 12.1 per cent looked for information about goods and services from the internet.

TABLE I: INTERNET ACCESS FROM A MOBILE DEVICE

IJSER © 2015 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 6, Issue 2, February-2015 98

ISSN 2229-5518

Also InMobi, a mobile advertising agency, in a recent report found out that 25% of people using mobile media engage themselves in social media sites such as Facebook and twitter. Other media usage was classified as follows: 19% general entertainment; 17% General information and search;

13% Games; 12% E-mail; 8% local searches; and 7% shopping [1]. ICT has got a big boost by mobile phone technology growth more so in the mobile application software development section. These rapid changes have been made possible with the mobile technology growth. From the information found in the yearly reports from CAK reveals that mobile phone subscription in Kenya reached the 32.8 million subscriptions by September 2014 [3]. Because of this growth it is naturally expected that the mobile internet also grows where by this period it was recorded as 14.8 million subscriptions.

A. Statement of the problem

ICT is an important sector in any country where it plays a very

important role in a nation’s economy. Researchers have not looked into the study of the trends of mobile internet subscription over the period from 2008 to 2014 when mobile phone operators started providing this service. This research is intended to have a detailed study on the trends of this industry in Kenya. This can help the telecommunication industry understand the trends and what is likely to happen in the near future so that they can give it a strategic response.

The Communications Commission of Kenya has in the past 15 years licensed four mobile operators (Safaricom, Airtel and Essar (Yu); all of which are global operators) and several internet service providers like Wananchi and Jamii Telkom. Clearly, competition in this sector has greatly intensified.

B. Research objectives

The broad objective of the paper is to make an extensive study on the trends experienced in the mobile internet in Kenya. The specific objectives are:

• Determine and analyze the mobile internet subscriptions trend in Kenya.

• To find out the determinants that affects the expansion

(growth) of this sector.

C. Importance of the study

The study would be valuable to several stakeholders for the following reasons:

1. Enable the telecommunication companies to know the trends in mobile internet subscription in Kenya.

2. Help companies to make informed future plans on mobile internet.

3. Telecommunication companies can use the findings to develop appropriate policies and strategic responses to the challenges as result of the rate of mobile internet subscription.

4. Enable CAK to give proper guidance to the mobile phone

operators in relation to data transfer.

5. The study would also provide a source of inspiration to a researcher for self-professional development and enrichment.

II. LITERATURE REVIEW

A. Telecommunication sector in Kenya.

To date there are four mobile operators in our country namely Safaricom Ltd, Airtel Networks Kenya Ltd, Essar Telecom Kenya Ltd and Telkom Kenya Ltd (Orange) even though Essar Telecom Kenya Ltd is expected to exit the market any time soon. According to the mobile subscription and profitability Safaricom Ltd is in the top position among the four operators [2]. The other companies have lower market shares as shown in the study but their main companies are the world’s famous and big organizations like Airtel has very high subscription in most Asian countries including India (highest with 192.22 million subscribers as of August 2013) [3].

According to CAK statistics, by the end of the first quarter of the 2014/15 financial year (Sep. 14), there were a total of

32.8 million subscriptions in the mobile telephony market segment up from 32.2 million posted in the previous quarter. This represents an increase of 1.6 percent during the period. Mobile penetration however increased by 1.3 percentage points to 80.5 per cent from 79.2 per cent during the previous quarter. The number of SMS grew by 1.2 per cent to stand at

6.9 billion up from 6.8 billion recorded during the previous quarter. Each subscriber sent an average of 71 SMS per month. Mobile money transfer service continued to record growth due to its popularity and convenience in usage. During the quarter under review, the number of subscriptions rose marginally by 1.4 per cent to 26.9 million up from 26.6 million subscriptions recorded during the previous period. The fixed line market continued to record a downward trend to post 192,778 lines down from 201,233 recorded during the previous period, representing a 4.2 per cent decline. Fixed terrestrial lines declined after recording 50,018 lines from

52,053 during the previous quarter. Fixed wireless recorded a

decline of 4.3 per cent during the period to register 142,760 subscriptions from 149,180 posted during the previous quarter.

Data/Internet subscriptions maintained an upward trend during the quarter, mainly boosted by the mobile data/internet subscriptions. During the quarter under review, there were

14.8 million data/internet subscriptions up from 14.0 million subscriptions in the last quarter, representing 5.8 per cent increase. Mobile data/internet subscriptions rose by a similar margin of 5.9 percent to reach 14.7 million up from 13.9 million recorded the previous quarter. Consequently, the number of estimated internet users stood at 23.2 million up from 22.3 million users in the last quarter, representing a 4.1 percent increase during the period.

The International Internet Bandwidth Available (Equipped/Lit) in the country increased marginally during the quarter to reach 847,516 Mbps up from 847,464 Mbps recorded in the previous quarter. The International Internet Bandwidth Used stood at 478,074 Mbps representing 56.4 per cent of the total available capacity.

IJSER © 2015 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 6, Issue 2, February-2015 99

ISSN 2229-5518

The postal and courier sub-sector showed improvement during the quarter. The number of letters sent locally stood at 13.9 million up from 11.8 million letters sent during the last quarter, representing growth of 17.9 percent. Courier items sent locally too registered a 0.5 percent marginal increase to stand at 942,147 items up from 937,619 items during the last quarter. On the international traffic, incoming letters grew by

0.6 percent to record 24.7 million letters while international outgoing letters recorded substantial growth of 69.3 percent to reach 1.2 million up from 761,315 letters sent [2].

B. Mobile internet subscription

Mobile internet subscriptions are subscriptions to a public mobile telephone service using cellular technology, which provide access to the public switched telephone network [4]. The number of mobile internet subscribers usually gives an indication of how vibrant the internet telecommunication sector of a country is. It also shows the rate of growth of the sector. It can help many companies determine their stage of growth and respond strategically to the different challenges that come with each stage. The market share for each player in this field can also be determined using this very important indicator.

III. RESEARCH METHODOLOGY

A. Research design and data collection

This study basically covers a period of 5 years starting from June 2008 to June 2014. An attempt has also been made to include the latest information whenever available.

Much of the information for this research was obtained from secondary source i.e. websites. This was done by collecting data from the reports of the Communications Commission of Kenya (CAK), via the internet.

Annual reports of different telecom companies, articles published in newspapers, conference papers and seminars proceedings were also carefully studied to procure the needed information. The report only presents simple frequency and quantitative tables. Various statistical tools and techniques have been applied for the analysis and interpretation of data.

B. Data analysis

For this study, the content analysis technique was employed to analyze the data. Matlab and Microsoft Excel Spread Sheet, with the associated trend analysis and graphical representation techniques were used to analyze quantitative data. The full report on the key findings of this study by the researcher are presented in section below.

B. Market share analysis of telecom sector in Kenya:

Mobile subscription by September 2014.

By September 2014 the total number of mobile subscriptions was recorded as 14.8 million up from 14 million posted in the previous quarter (June the same year). This represents an increase of 5.8 percent during the period. The continued growth in mobile subscriptions indicates that there is still opportunity for growth in the mobile telephony services. However, the rate of growth in the subscriber base is flattening as the sector progressively tends towards maturity. The growth of mobile subscriptions is shown in Table 1.

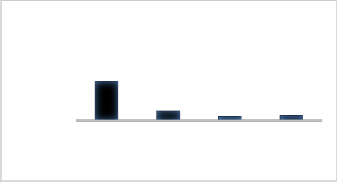

As of September 2014 the level of market shares measured by subscription is given in Table 1. Safaricom Ltd by mobile subscriptions has the highest market share as of this time of the year i.e. 21,849,831 translating to 66.7%. This is followed by Airtel Networks Kenya Limited at 5,402,415 equivalent to

16.5% then Telkom (Orange) with 3,022,889 same as 9.2% and finally Essar Telecom with the lowest at 2,493,693 translating to 7.6%. The market share by subscription by operator is shown in Figure 1.

TABLE II: MOBILE SUBSCRIPTIONS

Source: CAK

P ER C EN TA N G E S U B S C R I P T I O N M A R K ET S H A R E P ER O P ER AT O R

IV. FINDINGS AND DISCUSSIONS A. Introduction

This section deals with analysis and discussion of the research findings. Data was collected from the CAK website

30,000,000

20,000,000

10,000,000

0

21,849,831

5,402,415 2,493,693 3,022,889

in which case the mobile internet subscriptions are analyzed. Following is a report on the key findings of this study by the researcher.

Source CAK

Safaricom

Ltd

Airtel

Networks

Kenya Ltd

Essar

Telecom

Kenya Ltd

Telkom

Kenya Ltd

(Orange)

IJSER © 2015 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 6, Issue 2, February-2015 100

ISSN 2229-5518

Figure 1: Percentage market share per operator as of

September 2014

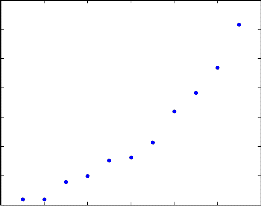

Mobile internet subscription from 2008 to 2014

Table 3 below summarizes the key findings on the mobile internet subscription from the year 2008 to 2014. The data provided is on half yearly basis taking subscription as of June and December each year except for 2014 where the subscription is as of June.

Probably due to aggressive rollout of mobile data services by mobile operators led to the astronomical growth of subscriptions between December 2008 and June 2009 as can be noted from the table. Besides the above subsequent growth was attributed by the provision of data services through GPRS/EDGE and 3G networks by mobile operators and innovative offerings such as connectivity to social networking sites through the mobile phones, a service that has gained popularity among young people in the country. Mobile service contributed 99 per cent of the total internet subscriptions during this period according to CAK data.

For instance one operator offered reduced prices for handsets that have the capability to access 3G services as well as GPRS/EDGE.

TABLE III: MOBILE INTERNET SUBSCRIPTIONS

period, one of the operators offered 10 per cent free airtime upon purchase or renewal of certain bundles while another offered certain categories of free minutes to customers for audio conferencing for bundle usage of Kshs100 weekly or Kshs400 monthly. Also one of the operators offered inactive internet subscribers with data enabled phones free 40MB data valid for 30 days while another offered its customers double bonus for purchase of the daily data bundles. In addition, another operator offered 500MB per month for four months for a minimum top up of Kshs 200.

x 10 Mobile internet Subscription.

14

12

10

8

6

4

2

0

2008 2009 2010 2011 2012 2013 2014

Year

Figure 2: Mobile internet subscription from June 2008 to June

2014

From the graph it can be noted that at the initial stages the growth was not as high as the later stages. Between 2008 and

2009 the growth rate was very high. This is the same case as for from 2011 onwards. This clearly shows that the mobile internet market is still at its early stages of growth. It will take some time before it reaches market maturity. Because of this mobile operators should look for means to tap into this market. We can conclude that the graphical changes seem to follow a natural trend of exponential growth. This is because at the initial stages there is a slow growth i.e. from 2008 to

2011, the middle is characterized by high growth with steep gradient i.e. 2011 to 2014 and later the growth is expected to start flattening which has not happened yet.

TABLE IV: MOBILE INTERNET SUBSCRIPTIONS YEARLY GROWTH RATE

From June 2012 to June 2014 mobile internet subscription came close to double attributed by the fact that data service promotions and special offers by mobile operators during the period confirmed their keenness to continue growing their market shares and consequently contributing to the increase in mobile data/internet subscriptions. For instance, during the

IJSER © 2015 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 6, Issue 2, February-2015 101

ISSN 2229-5518

Source: Research findings

3000

2500

2000

1500

1000

500

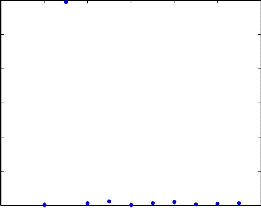

Mobile internet subscription growth rate in Kenya.

0

2008 2009 2010 2011 2012 2013 2014

Year

Figure 3: Mobile internet Subscriptions yearly growth rate

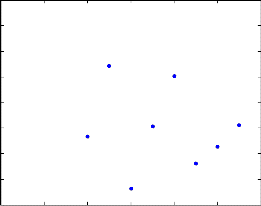

Figure 3 and 4 show graphical representations of the subscription growth rate against the years. The graphs show that the period between December 2008 and June 2009 had a very high growth rate and from June 2009 to December 2009 the growth rate decreased drastically. This could be attributed by the fact that during this period business was at its initial stages of growth and was based on small numbers. There were slight increments between June 2010 and December 2010 as well as 2011 to 2012 and June 2012 and June 2014 probably due to the large number base which is in the million range. Figure 4 gives a representation between 2010 and 2014 to increase clarity since the variations are small.

Mobile internet subscription growth rate in Kenya.

80

70

60

50

40

30

20

10

0

2008 2009 2010 2011 2012 2013 2014

Year

Figure 4: Mobile internet Subscriptions yearly growth rate from 2010 to 2014

V. SUMMARY, CONCLUSIONS AND RECOMMENDATIONS

A. Summary

The objectives of this study were to analyze the mobile internet subscription trends in the telecommunication industry in Kenya. The researcher found out that subscription rate has been growing since the mobile operators started offering internet through their networks. By June 2014 the total number of mobile internet subscriptions was recorded as 14.0 million up from 388 thousand posted in 2008. This shows that mobile internet subscription has been steadily growing and is expected to continue growing given that there is a huge untapped market.

B. Conclusion

According to the population census 2009, the age bracket of

15-64 years represent 53.6 per cent of the population, an indication that there is still a huge market potential that is yet to be covered and opportunities for provision to this service are yet to be fully exploited.

We can conclude that the graphical changes seem to follow a natural trend of exponential growth. This is because at the initial stages there is a slow growth i.e. from 2008 to 2011, the middle is characterized by high growth with steep gradient i.e.

2011 to 2014 and later the growth is expected to start flattening which has not happened yet.

There has been significant growth in telecommunication sector particularly in the use of mobile internet. Competition among the operators, unification of the licenses and the application of new technologies in mobile market segment has witnessed diversification of services by the operators, reduced rates and increased affordability of communication services by a large population. This is further seen as a movement towards closing the digital divide. Currently the number of smart phones has grown where most people can afford them. The introduction of 3G networks in Kenya has also helped a lot in

shaping the internet market. Currently plans are under way to

introduce 4G which is highly IP based and therefore tailored well to handle data.

IJSER © 2015 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 6, Issue 2, February-2015 102

ISSN 2229-5518

This growth is expected to increase as more and more people especially the youth continue to join the social networks like face book, twitters and blogs.

Considering this trend, the coming periods are likely to continue recording growth as operators devise innovative products and services expected to entice subscribers and thus propel this sector even further. Besides the data market is expected to have new entrants soon like Equity bank which has already been given a license. The influential factors in the evolution of Mobile Services are but not limited to the following; rapid growth in the internet, increasingly data- hungry applications, and data overtakes voice traffic, users want mobility and huge potential for mobile Internet. The ease of subscription coupled by the ease of accessing the service through the mobile phone has enhanced growth in this market segment. Moreover, there is still unexploited capacity and potential in this market segment. Consideration for projects geared towards optimal utilization of this capacity could be valuable as this will ultimately stimulate further growth in this market segment. Therefore research needs to be undertaken to increase the quality of service (QoS) to the mobile internet users who seem to be growing day and night.

C. Recommendations

In light of the foregoing findings by the researcher, Telecommunication companies should keenly implement the following:

• Look for ways of improving mobile internet subscriptions while balancing on their returns.

• Research on the different ways of increasing quality of service (QoS) to significantly new competitive levels.

• Look for ways of reducing the cost of mobile internet which

is still high.

D. Limitations of the study

The major limitation of the study is lack of information on monthly basis and previous workings on the topic. There are not enough supportive articles to make an extensive literature review since this is a new field.

E. Areas of further study

Future research should include forecasting the future of internet subscriptions in Kenya using different methods. Another area of study would be to look at the impact fixed networks on the competitiveness of Kenyan telecommunications companies. One can also research on comparing mobile internet and fixed internet as well as QoS improvement strategies.

F. Future outlook

The future outlook of mobile internet is very positive as the market still looks young and the introduction of 4G will make it even better where it is expected to have more and more IP based services for instance mobile IP and IPTV besides the predicted use of mobile internet for Geo-tracking (location based search), Mobile Video and Mobile Advertising. Telecommunication infrastructure will have a major boost

with the completion of the Optic Fibre Backbone Infrastructure which is being currently being laid in most urban centres. This is expected to increase bandwidth capacity, in most parts of the country which should have a positive impact on internet diffusion in rural and remote areas. With the recent focus on local content by data service providers and introduction of new data service providers like Equity, internet usage in the country is expected to rise.

REFERENCES:

[1] http://www.CAK.go.ke/resc/statcs.html

[2] http://www.CAK.go.ke/resc/research.html

[3] http://telecomtalk.info/aircel-adds-highest-number-of- gsm-subscribers-in-august-followed-by-airtel-vodafone- loses-coai/108943/

[4] http://data.worldbank.org/indicator/IT.CEL.SETS.P2

IJSER © 2015 http://www.ijser.org