International Journal of Scientific & Engineering Research Volume 2, Issue 7, July-2011 1

ISSN 2229-5518

Indigenous resource usage in the

pharmaceuticals industry in Bangladesh: A descriptive approach to explain the industry scopes

Md. Nazmul Huda, S M Mazharul Islam, Anzir Mahmud, Md. Ariful Islam Russell

Abstract— W hether there is any framework or not, sometimes businesses grow and run into an economy. After a matured stage, the community starts developing the industry for their own good. Bangladesh has a very competitive market inside and also outside from its own pharmaceuticals industry, even where multinational organizations are facing many challenges to compete with local organizations. But in this matured stage how much indigenous technology they could reveal out from the system. Students are getting out from universities, but they’re not learning how to develop through research. They are becoming just operational workers. But through incubation and better investment, this situation can be improved. Besides this another threat is coming nearby to this industry. Patent rights valuation will make the local organizations weaker just because they are compounding the resources ignoring investments into molecule development. Several Active Pharmaceuticals Ingredients (APIs) are being produced here, but not in that large scale. To cope up with this situation government and DDA should come up some strategic plans to stand against future threats.

Index Terms— pharmaceuticals, pharmaceuticals scopes, Bangladesh, indigenous resource, pharmaceutical resources, pharmaceutical export-import, research and innovation

1 INTRODUCTION

—————————— • ——————————

ndustry can be defined as any type of Economic Activity producing goods or services. It is part of a chain – from raw materials to finished product, finished product to service

sector, and service sector to research and development.

Pharmaceutical industry can broadly be classified into two

categories. These are -a) Patent Medicines & b) Generic Medi-

cines.

Patent medicines are developed in own laboratory with high- ly sophisticated equipment & researchers with dedication, learn- ing. These products are patented for generally twenty years to enjoy the market share & also to act as a monopoly. After years

of business functions the formulation, process, medicine or tech- nology are sold in the market so that others can go into mass production with providing them adequate royalty. On the other hand Generic medicines are the products that are produced in mass scale with licensing. Several companies under different brand name market this same kind of product, where the formu- lation of this product is almost same with different commercial name. Prices of the products are under this category may vary.

————————————————

• Md. Nazmul Huda is currently working as Assistant Program Manager in Ban- gladesh Association of Software and Information Services and pursuing honors degree program in Business Administration in Khulna University, Bangladesh, Mobile-+8801714117014. E-mail: aoni_k@yahoo.com

• S M Mazharul Islam is currently pursuing honors degree program in Business Administration in Khulna University, Bangladesh, Mobile-+8801713924500. E- mail: smmzislam@gmail.com

• Anzir Mahmud is currently pursuing honors degree program in Business Admin-

istration in Khulna University, Bangladesh, Mobile-+8801715052642. E-mail:

anz_malik@yahoo.com

• Md. Ariful Islam Russell is currently working as Assistant Manager in BASIC Bank Ltd. (Khulna Branch), Bangladesh, Mobile-+8801717529503. E-mail: ari-

frussell@yahoo.com

Bangladeshi pharmaceuticals companies mainly concentrate on this category, as labor & procession cost is one of the lowest in the world. [1]

2 PHARMACEUTICALS INDUSTRY IN BANGLADESH

2.1 Development of pharmaceuticals industry in

Bangladesh

Pharmaceutical industry has grown in Bangladesh in the last two decades at a momentum rate. Its healthy growth supports development of auxiliary industries for producing glass bot- tles, plastic containers, aluminum collapsible tubes, aluminum PP caps, infusion sets, disposable syringes, and corrugated cartons. Some of these products are also being exported to oth- er countries that generally have unregulated to medium regu- lated market. Printing and packaging industries and even the ad firms consider pharmaceutical industry as their major clients and a key driving force for their growth. The sector con- sistently creates job opportunities for highly qualified as well as lower skilled people. Many established entrepreneurs of today are now thinking about establishing own pharmaceutical division the latest one is APEX pharma. Bangladeshi compa- nies are either directly or indirectly contributing largely to- wards raising the standard of healthcare services through enabling local healthcare personnel or facilities to gain access to newer products and to latest drug related information. Due to recent flashy development of this sector, Bangladesh is ex- porting medicines to global market including highly regulated European market. This sector is also providing 95% of the total medicine requirement & medical equipment of the local mar- ket. Leading Pharmaceutical Companies are expanding & en- hancing their business with new product, process, technology

IJSER © 2011 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 2, Issue 4, April-2011 2

ISSN 2229-5518

& marketing techniques with the aim to expand export market. In Bangladesh Pharmaceutical sector is one of the most devel- oped hi tech sector in this country which effectively lessening the brain drain problem that is contributing in the country's economy. After the promulgation of Drug Control Ordinance -

1982, the development of this sector was achieved. The profes- sional knowledge, dedication, government policy support, knowledge about international market, thoughts and innova- tive ideas of the pharmacists working in this sector are the key factors for these impressive developments. Recently few new industries have been established with hi tech equipments pro- ducing facilities and professionals training which will enhance the strength of this sector further.

Bangladesh, currently having more than a couple of hun- dred manufacturing facilities, dedicated pharmacists with huge Potential in pharmaceutical formulations, is going to be eco- nomically self sufficient in this sector, which will ultimately develop their technological capacity. Aiming at minimizing the import dependency on basic drugs, the country's prime con- cern is about building up of own capability in the manufactur- ing of active pharmaceutical ingredients(APIs), base materials and other allied industry inputs. Pharmaceutical sector is cap- turing near about 12% of market capitalization which is the second largest in the world & first among third world coun- tries. This position also indicates the positive sign for foreign investment in pharmaceutical sector.

The combined capacity of the industry for the pharmaceuti- cal formulation is huge and a number of companies recently have approval from UNICEF as its global as well as local sup- plier of pharmaceutical products. According to Salman F Rah- man president, Bangladesh Aushad Shilpa Samity (Bangladesh Association of Pharmaceutical Industries - BAPI), since 1972 the Association has been the only recognized association for pharmaceutical manufacturers in Bangladesh playing pivotal role in the development of pharmaceutical sector. BAPI, as the apex and premier pharmaceutical trade and promotion body of Bangladesh, has been very actively working on the industry development programs to enhance the existing capabilities and to promote the country's industrial opportunities among the developed world by attract prospective collaborators in terms of technology, product sourcing, infrastructure etc.

2.2 Localizing of the pharmaceuticals industry in

Bangladesh

Following the Drug Control Ordinance of 1982, some of the local pharmaceutical companies improved range and quality of their products considerably. The national companies account for more than 95% of the pharmaceutical business in Bangla- desh. However, among the top 20 companies of Bangladesh 2 are multinationals. Almost all the lifesaving imported products and new innovative molecules are channeled into and mar- keted in Bangladesh through these companies. Multinational and large national companies generally follow current good manufacturing practices (CGMP) including rigorous quality control of their products. The Drug Act of 1940 and its rules formed the basis of the country's drug legislation. unani, ayur- vedic, homeopathic and bio-chemic medicines were exempted from control under the legislation. The foreign companies dominated the pharmaceutical industry at that time. Even in

the allopathic market there were extemporaneous preparations dispensed from retail pharmacies. The pharmaceutical indus- try, however, like all other sectors in Bangladesh, was much neglected during Pakistan regime. Most multinational compa- nies had their production facilities in West Pakistan. With the emergence of Bangladesh in 1971, the country inherited a poor base of pharmaceutical industry. For several years after libera- tion, the government could not increase budgetary allocations for the health sector. Millions of people had little access to es- sential lifesaving medicines. With the promulgation of the Drug Control Ordinance of 1982, many medicinal products considered harmful, useless or unnecessary were removed from the market allowing availability of essential drugs to in- crease at all levels of the healthcare system. Increased competi- tion helped maintain prices of selected essential drugs at the minimum and affordable level.

In 1981, there were 166 licensed pharmaceutical manufac- turers in the country, but eight multinational companies (MNCs) which manufactured about 75% of the products domi- nated local production. There were 25 medium sized local companies, which manufactured 15% of the products, and oth- er 133 small local companies produced the remaining 10%. All these companies were mainly engaged in formulation out of imported raw materials involving an expenditure of Tk 600 million in foreign exchange. In spite of having 166 local phar- maceutical production units, the country had to spend nearly Tk 300 million on importing finished medicinal products. A positive impact of the Drug (Control) Ordinance of 1982 was that the limited available foreign currency was exclusively uti- lized for import of pharmaceutical raw materials and finished drugs, which are not produced in the country. The value of locally produced medicines rose from Tk 1.1 billion in 1981 to Tk 16.9 -13824 in 1999. At present, 95% of the total demand of medicinal products is met by local production. Local compa- nies (LCs) increased their share from 25% to 70% on total an- nual production between 1981 and 2000.

In 2000, there were 210 licensed allopathic drug- manufacturing units in the country, out of which only 173 were on active production; others were either closed down on their own or suspended by the licensing authority for drugs due to non-compliance to GMP or drug laws. They manufactured about 5,600 brands of medicines in different dosage forms. There were, however, 1,495 wholesale drug license holders and about 37,700 retail drug license holders in Bangladesh. Anti- infective is the largest therapeutic class of locally produced medicinal products, distantly followed by antacids and anti- ulcer ants.

Other significant therapeutic classes include non-steroidal anti-inflammatory drug (NSAID), vitamins, central nervous system (CNS) and respiratory products. A most remarkable progress the local industry has made in recent time is the phe- nomenal increase in the local production of basic chemicals. There are now 13 drug-manufacturing units, which also manu- facture certain basic materials. These include Paracetamols, Ampicillin Trihydrate, Amoxycillin Trihydrate, Diclofenac So- dium, Aluminum Hydroxide Dried Gel, Dextrose Monohy- drate, Hard Gelatin capsule shell, Chloroquine Phosphate, Propranolol Hydrochloride, Benzoyl Metronidazole, Sodium Stibogluconate (Stibatin) and Pyrantel Pamoate. However,

IJSER © 2011 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 2, Issue 4, April-2011 3

ISSN 2229-5518

most of these are confined to the last stage of synthesis. There are three public sector drug-manufacturing units. Two of them are the Dhaka and Bogra units of Essential Drug Company Ltd. (EDCL), which is functioning as a public limited company un- der the Ministry of Health and Family Welfare. EDCL pro- duced medicines worth Tk 964 million in 2000. There are sepa- rate vaccines and large volume IV fluids production units un- der the Institute of Public Health (IPH). The productions of both EDCL and IPH are mostly used in government hospitals and institutions. In 2000, there were 261 unani, 161 ayurvedic,

76 homeopathic and biochemic licensed manufacturing units. They produced medicines worth Tk 1.2 billion in 2000. One of the major positive impacts of Drug (Control) Ordinance is the rapid development of local manufacturing capability. Almost all types of possible dosage forms include tablets, capsules, oral and external liquids (solutions, suspensions, emulsions), ointments, creams, injections (small volume ampoules/dryfill vials/suspensions and large volume IV fluids), and aerosol inhalers are now produced in the country. In recent years, the country has achieved self-sufficiency in large volume parenter- als, some quantities of which are also exported to other coun- tries. The development of local manufacturing capability helped contain dependence on the import of pharmaceutical products (raw material and finished product) around pre-1982 level. Under the Drug (Control) Ordinance, government fixes the maximum retail prices (MRP) of 117 essential drug chemi- cal substances. Drugs other than these essential ones are priced through a system of indicative prices. This rule applies on the locally manufactured products only. For imported finished products, a fixed percentage of markup is applied on the C&F price to arrive at the MRP, regardless of whether they are with- in the list of essential 117 molecules or not. It is interesting to note that, even with withdrawal of price control from many products, prices have not shot up; healthy competition has been keeping within affordable prices.

Physical distribution of pharmaceuticals in Bangladesh has evolved in a unique way. Unlike other countries, the compa- nies themselves do Bangladesh pharmaceutical industry is more retail oriented and bulk of distribution. Pharmaceutical companies distribute their products from their own ware- houses located in different parts of the country, as no profes- sional distribution house is available. Wholesalers play a li- mited role in this regard since companies supply goods to both retailers and wholesalers. Export of pharmaceutical products is still in an infant stage, although a number of private pharma- ceutical companies have already entered the export market with their basic materials and finished products. They export their products to Vietnam, Singapore, Myanmar, Bhutan, Nep- al, Sri Lanka, Pakistan, Yemen, Oman, Thailand, and some countries of Central Asia and Africa.

The primary responsibility for drug quality control lies with the manufacturers. However, the government's drug testing laboratories (DTL) and the Directorate of Drug Administration (DDA) have the monitoring and supervising role. There are two government drug-testing laboratories. DTL at Dhaka is in the Institute of Public Health and the regional DTL at Chitta- gong is under DDA. Drug administration is responsible for registration of drugs for marketing in Bangladesh and for in- spection of premises and licensing. With its present set up and

inadequate strength, DDA often finds it difficult to carry out its very large volume of assigned work. The national drug policy and the regulatory control policies are yet to achieve best re- sults for a healthy growth of the pharmaceutical industry. Be- cause of the limited capacity of the government's drug testing laboratories, the quality of products manufactured locally can- not be uniformly ensured, sometimes this tests are done in pharmaceutical companies own testing labs(DDA) .Restrictions on patent rights discourage foreign investors to come up ac- tively in the pharmaceutical market in Bangladesh. Introduc- tion of new research molecules is difficult due to slow registra- tion process and restrictions on patent protection. Although the fixed mark-up system of pricing helped keep the prices of pharmaceutical products low, this made it difficult to cover costs of marketing and distribution. The fixed mark-up system also discourages some companies to invest for cGMP and as- surance of high quality production. Some important therapeu- tic classes of the pharmaceutical market (antacids and oral vi- tamins) are only open to the local companies even after 20 years of the drug ordinance. This policy is discriminatory and contrary to the announced investment policy of the govern- ment.

The annual per capita drug consumption & usage rate in Bangladesh is one of the lowest in the world, also in the third world countries, with high cost & poor supervision. However, the industry can be ascertained as a key contributor to the Ban- gladesh economy since 1982. With the development of health- care infrastructure, government intervention, increase of health awareness and the purchasing capacity of people, this industry is expected to grow at a higher rate in future than the present condition.. Healthy growth is likely to encourage the pharma- ceutical companies to introduce newer drugs, newer formulas, newer equipments and newer research products, while at the same time maintaining a healthy & non-monopolistic competi- tiveness in respect of the most essential drugs. In Bangladesh Pharmaceutical sector is one of the most developed hi tech sec- tor with most educated science background people, which is contributing in the country's economy. After the promulgation

& inception of Drug Control Ordinance - 1982, the develop- ment of this sector was accelerated & impressive.

Besides, out of the total domestic requirement of medicines, almost 95 per cent is met by the local manufacturing and Ban- gladesh exports formulations to 83countries around the world (EPB). The current turnover of the industry in Bangladesh is Tk. 6,000 crore. (BAPI) According to industry sources, the for- mulation industry in Bangladesh currently grows at the rate of

22 per cent. With this estimate, the expected business in year

2011 is 1, 50,000 million Tk. Today, Bangladesh is dealing with

USA, India, China, Taiwan, Hong Kong, European Union, Sin-

gapore, Malaysia, Pakistan, Sri Lanka, Thailand, Burma, Bhu-

tan, Nepal, Yemen, Mauritius, Vietnam, Kampuchea, Laos,

Mexico, Columbia, Ecuador, Russia, Uzbekistan, Tazakistan,

Kenya, Tunisia, Maldives, etc. as well as with the least devel-

oping countries where there is hardly any industry for the pro- duction of pharmaceutical formulations.

Turnover from pharmaceutical sector is encouraging & one of the highest in the world which is about 14% of total industry turnover. This position also indicates the positive sign for for- eign investment in pharmaceutical sector. To be a major global

IJSER © 2011 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 2, Issue 4, April-2011 4

ISSN 2229-5518

source of APIs and also be able to produce patent drugs is not much difficult for this country, which are still under patent protection, as the TRIPS Council meet at Doha has declared the least developed country (LDC) status to remain without patent regime till 2016, it needs active participation and contribution from local firms, governments, educational institutions as well as foreign companies to build upon the capability.

However, the trend now seems to be favorable to the coun- try as the domestic pharmaceutical industry are going for rapid expansion as well as the companies from neighboring countries like India, China and even MNCs have queued up to put in investments on this front as every stakeholder will benefit of vast potential that Bangladesh can offer. The local entrepre- neurs are capable and willing to invest and collaborate with suitable foreign partners in order to develop the existing API manufacturing facilities. Presently top pharmaceutical compa- nies in Bangladesh are also in the process of getting into bulk drug production with collaborative technology, technology transfers and joint venture basis. The large-scale players in the Bangladesh pharmaceutical industry currently include Square Pharma, Beximco, Acme, Incepta, Eskayafe, Renate, General Pharma etc. The MNCs that have a major presence in the coun- try's pharma sector are Aventis, Pfizer, Novartis and Astra Ze- neca.

3 DEVELOPMENT STATUS IN PHARMACEUTICALS INDUSTRY IN BANGLADESH

3.1 Development of National Drug Market

Drug ordinance 1982 has been successful to realize the radical objectives it proposed, by laying down the foundation for a modern pharmaceutical industry. The demographic and eco- nomic context has substantially changed over the periods in Bangladesh. If the period of 1970-2010 is considered, the popu- lation count stands at 162.2 million in 2009 from a 79 million of the 1970,though the fertility per woman has dropped down to

2.338 from 6.2 children. Over the period of time Bangladesh pharmaceutical industry has been successful in meeting the medicament demand of its huge home population. Local pro- ducers are the producers of the generic drugs in their own

brand name. There are 237-licensed drug manufacturers in Bangladesh and among them 150 are in operation, while 138 are registered member of Bangladesh association of pharma- ceuticals industries. This industry employs 65000 skilled people & 1500 unskilled people in indirect manner. Local pro- ducers supply 97% of the yearly domestic demand for the hu- man pharmaceutical drugs of the country, rest 3% imported finished drugs includes only high tech therapeutic drugs.

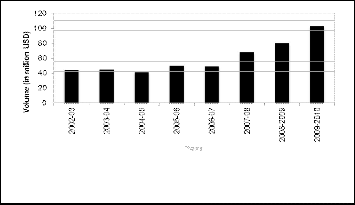

3.2 Import Scenerio

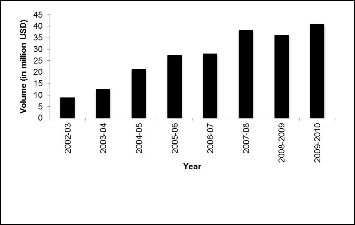

It shows that import of the finished pharmaceuticals drugs have decreased over the time, while the import of the pharma- ceutical raw materials and the packaging materials for the pharmaceutical product delivery have increased to meet the growing demand of local manufacturers.

Fig. 2. Import scenario in the Bangladeshi pharmaceutical sector

(2002-2010)

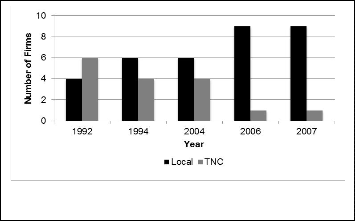

3.3 Number of firms

This chart shows that local drug manufacturers have not only increased their dominance in the market as a group, but also in individual level, they have successfully toppled the TNCs in term of their market shares in the local market.

Fig. 3. Import scenario in the Bangladeshi pharmaceutical sector

(2002-2010)

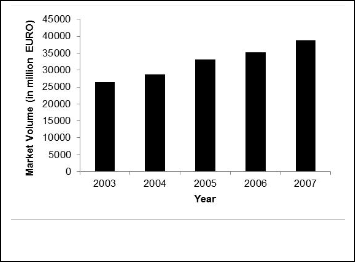

Fig. 1. Development of national drug market in Bangladesh (2003-

2007)

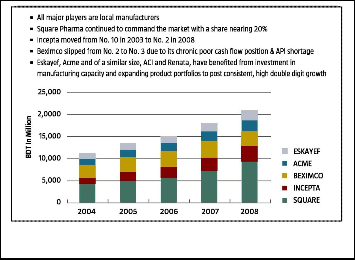

3.4 Market share composition

Bangladeshi market are keen to retain their distribution infra- structure and have the ability to offer agency services, where new entry multinationals may have no established platform. Multinationals also encounter difficulties achieving the econo- mies of scale in a field where 69% of the domestic market is made up of independent pharmacies.

IJSER © 2011 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 2, Issue 4, April-2011 5

ISSN 2229-5518

level education is very low. But there is a very significant factor that public spending ability is not that much behind its back.

TABLE 4.1

EDUCATION SCENARIO IN GENERAL BANGLADESH

Public Spending on education, total (% of government

2002 2003 2004 2005 2006 2007

16 15 15 - 14 16

Fig. 4. Market share composition in pharmaceuticals industry in Ban-

expenditure)

Public spending on

gladesh (2004-2008)

education,

total (% of

2 2 2 - 2 3

3.5 Pharmaceuticals drug export

GDP) School

enrollment,

After consolidating the positions in domestic market, leading Bangladeshi pharmaceuticals tried to explore markets outside Bangladesh. Bangladesh mainly exports generic finished for- mulations in dosage and bulk form as well as small amount API. Bangladeshi pharmaceutical products are exported to as many as 73 countries including USA, India, China, Taiwan, Hong Kong, European Union, Singapore, Malaysia, Pakistan, Sri Lanka, Thailand, Burma, Bhutan, Nepal, Yemen, Mauritius, Vietnam, Kampuchea, Laos, Mexico, Columbia, Ecuador, Rus- sia, Uzbekistan, Tazakistan, Kenya, Tunisia, Maldives, etc. as well as with the least developing countries where there is hard- ly any industry for the production of pharmaceutical formula-

primary (%net) School enrollment, secondary (%net) School enrollment, tertiary (% gross)

- - - 87 88 -

44 44 41 40 41 41

5 6 5 6 6 7

tions.

Fig. 5. Development of national drug market in Bangladesh (2003-

2007)

4 INSTITUTIONAL AND INDUSTRIAL VIEW OF BANGLADESH REGARDING DEVELOPMENT OF PHARMACEUTICALS INDUSTRY

4.1 Education and Research

Bangladesh is still pursuing to achieve the competence level in education and research works to prepare our population as a self-dependent production population.

Here in the table 1 we can see that enrollment in tertiary

World Bank Data Bank, March 2011

Since 1964, 4 public universities and 14 private universities have been settled to prepare pharmacy students and researchers. But this rate is not satisfactory to our industry. There are 18 government and 28 private medical colleges besides one medical university (including 3 dental colleges under government and 8 under private management) recognized by BMDC (Bangladesh Medical and Dental Council) where around 2500-2700 students get enrolled yearly.

But we have headache in the other side. While we have come for the true scenario, we’ve learned that to get the competitive edge our pharmaceuticals industry needs some graduates can completely sacrifice themselves into research to develop molecules. But we don’t have the capability to gain that advantage because of our public spending limitation. Neither do the private investments because of high business risk developing a molecule.

Now come back to the institutional limitations. There are two training institutes on the subject of health technology. From here technical people are getting prepared.

Global Information Technology Report (GITR) 2010 of the Global Economic Forum (GEF) has ranked the quality of the education system of Bangladesh is 108th, quality of mathematics and science education in Bangladesh is 118th, quality of management schools is 101st, and local availability of research and training is 119th of the world [2].

IJSER © 2011 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 2, Issue 4, April-2011 6

ISSN 2229-5518

We can get an explanation from the institutional actions regarding researches and education systems supporting pharmaceutical industry. From several interviews we knew that for research purpose the money is needed cannot be provided by the whole pharmaceuticals industry. This is why we are not developing researchers rather than compounding.

Basically here post graduate institutions are engaged in some small scale researches, e. g. Institute of Public Health; Bangladesh Medical Research Council; Bangladesh National Research Council; Institute of Epidemiology Disease Control and Research; International Centre for Diarrheal Disease Research, Bangladesh (iccddr,b); National Institute of Cancer Research and Hospital; National Institute of Population Research; National Institute of Preventive and Social Medicine; Rehabilitation Institute and Hospital for the Disabled; National Institute of Kidney Diseases and Urology and National Institute of Biotechnology. Beside these institutions there are some collaborative initiatives between firms and public sector institutions in R&D, teaching and delivery of health services are observed in Bangladesh [5].

TABLE 4.2

RESEARCH & INNOVATION SCENARIO IN BANGLADESH

4.2 Patent Rights and Enforcement

Bangladesh government provides patent regimes through Pa- tents and Design act 1911 (last amended in 2003) and the Patent and Design Rules of 1933. The act declares the patents to be valid for a total of 16 years (section 14), calculated from the date of application (section 7), and allows a further extension of ten years (section 15(a)(1)).

Bangladesh has been awarded a waiver period for TRIPS (Agreement on Trade Related Aspects of Intellectual Proper- ties) until 2016. By this waiver, Bangladeshi organizations can bring the formulas from outside and produce drugs through compounding process. But after 2016 when these patent rights will be declared and the waiver will be gone, the Pharmaceuti- cals industry is going to down. Because Bangladesh doesn’t have any research facilities so that the country can develop new drugs to survive in market. Whether the organizations will have to buy those formulas with a huge amount of money, or they will need to shut down. And the panic is most of the organization doesn’t have that capital infrastructure to run without that waiver.

But there is a hope that some of Bangladeshi institutions are trying to develop APIs (Active Pharmaceuticals Ingredients) and there are some excipients and paracetamols are being de-

veloped in laboratories.

Patent applications, Resisdents Patent applications, Non- residents Research & development expenditure (% of GDP) Researchers in R&D (per million people) Technicians in R&D (per million people)

2002 2003 2004 2005 2006 2007

43 58 48 50 22 29

- - - - - -

- - - - - -

- - - - - -

- - - - - -

‘National Drug Policy (NDP) 2005’ has been encouraging for production and technology transfer focused FDI and joint ven- ture in pharmaceuticals industry sector. NDP 2005 reserves the provision for the condition that the aspirant foreign firm must have at least three original drug discoveries which are regis- tered in at least two of the countries e.g. USA, UK, Switzerland, Japan, Germany, France, and Australia. It also allows the im- port of the state-of-the-art live saving drug, If those drugs are registered with similar brand name in any of the countries e.g. USA, UK, Switzerland, Japan, Germany, France, and Australia. NDP 2005 also allows contract manufacturing and toll manu- facturing for other local and foreign firms and the imports for specific high-tech drug production are being encouraged. NDP

2005 has made these foreign firms; friendly provisions mainly with the objective to facilitate technology transfer in the coun- try in faster pace and guide the industry more toward technol- ogy based competition from brand-based competition. Besides the manufacturing level surveillance on the quality and safety of the drugs, NDP 2005 puts emphasis on the post-marketing surveillance on the quality and safety of the drugs. It entrusts DDA to implement these surveillances. The local pharmaceuti-

World Bank Data Bank, March 2011

Global Information Technology Report (GITR) 2010 has ranked Bangladesh’s capacity for innovation on 123rd and availability of the latest technology on 109th place. Collaboration between industry and research institutions in the embryonic stage which GITR 2010 ranks as 125th in the world, while quality of the scientific research institutions has been ranked on 108th place in the world [2].

According to Directorate of Drug Administration (DDA) of Bangladesh there are 233 licensed pharmaceuticals institutions in the industry and in their database 10914 drugs are enlisted.

cal producers are not comfortable with the NDP 2005 provi-

sions of allowing the import of foreign drugs. NDP 2005 has

been designed for taking the local pharmaceutical industry on

the next level where attainment of the production of the API

(Active Pharmaceutical Ingredients i.e. pharmaceuticals raw

materials) and shaping up the structure of the industry for

making it suitable as reality export focused industry. Progress

of the implementation of this policy is not evident yet, as the

enforcing and monitoring institutions are far away from get-

ting them fit with it (Md. Noor Un Nabi, Utz Dornberger,

2010). Though Bangladesh Foreign Exchange Regulation (FER)

acts are quite unsupportive to international level capability building for which reason investors are discouraged to invest

IJSER © 2011 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 2, Issue 4, April-2011 7

ISSN 2229-5518

in new drugs rather than investing in invented drugs.

On the other hand there are only two testing system facili-

ties in Bangladesh operated by DDA. One is in Dhaka, and

another one is in Chittagong. Dhaka laboratory is managed by

National Institute of Health and Chittagong laboratory is un-

TABLE 4.4

RANKING OF BUSINESS CLIMATE CONDITIONS IN BANGLADESH

2002 2003 2004 2005 2006 2007

Gross

der the own hand of DDA.

The pharmaceutical sector was the second largest sector (af-

ter agriculture) in terms of national revenue. Employment in

the sector was about 75,000. The value of export for essential

drugs was US$ 3.1 million and natural ingredients US$ 48

thousand. It exported drugs to over 50 countries in the world,

but mainly to Bhutan, Singapore and Yemen. The export mar-

ket is on a rise each year. On the other hand, Bangladesh im-

ported essential drugs worth of US$ 21.6 million and natural

ingredients of US$ 19 million. Types of products imported in-

cluded 700 different types of finished products and over 742

basic raw materials. 85% of raw materials are imported from

West European countries, USA, Pakistan, Japan, Korea, Singa- pore, China and India. [7]

Here below in the table the general business climate in Ban- gladesh is now being shown-

TABLE 4.3

RESEARCH & INNOVATION SCENARIO IN BANGLADESH

2005 2006 2007 2008 2009 Overall ranking in

the world 81 88 88 107 119

Starting a new

business 63 68 68 92 98

Licencing 64 67 67 116 118

Employing Workers 75 75 75 129 124 Registration of

Property 167 167 167 171 176

Getting credit 41 48 48 48 71

savings (% of GDP) Gross fixed capital formation (% of GDP) Gross capital formation (annual % growth Domestic credit provided by banking sector (% of GDP) Domestic credit to private

sector (% of

GDP)

Financing via international capital markets (gross inflows, % of GDP)

30 30 31 31 35 36

23 23 24 25 25 24

8 8 9 11 8 8

50 50 52 55 58 58

30 30 32 34 36 37

0 0 0 0 0 1

Protecting investors 15 15 15 15 20

Paying taxes 69 72 72 81 89 Trading Across the

border 132 134 134 112 107

Enforcing contract 174 174 174 175 180

Closing business 87 93 93 102 108

World Bank Data Bank, March 2011

It can be said that there is no doubt that Bangladeshi drug companies are able to or are easily put in the position to manufacture top quality drugs. What is less clear, however, is the strategic decision to target high quality developing country export markets: since high quality comes at higher cost, and there is no significant domestic market for the most prominent donor funded drugs, those manufacturers who have a high- quality strategy rather aim for developed markets, e.g. by contract manufacturing [10]. Thus the World Bank concluded that even the larger organization can have problem with capacity planning, where the market demand is so high. Now here we can see the financing scenario in Bangladesh to understand better this situation.

World Bank Data Bank, March 2011

5 DISCUSSION

5.1 The Scene

We had a questionnaire through our interview session and within those questions everyone told that new students are efficient in just only ‘Industry & Operations’ but they are not capable of ‘Research & Development’. But there was one who talked about the private universities’ students who are not that much capable as the students do who come from public uni- versities.

There is ‘no’ in both question on research facilities availabili- ty and infrastructural support from everyone.

But the actual scene is here – 7 out of 7 organizations told that they use 100 percent of non-local equipments and machi- neries, 100 percent of local human resources. But in case of ma- terial usage, 6 out of 7 organizations found using some APIs from local producers which can be around 5% of total raw ma- terials usage of those regarding production facilities, but 1 out of 7 told that they don’t use any local material for their produc- tion purposes. This scene cause this following result into ma- terial usage-

IJSER © 2011 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 2, Issue 4, April-2011 8

ISSN 2229-5518

TABLE 5.1

FINANCING SCENARIO IN BANGLADESH

Local Materials Imported

Materials

Total Mean 4.29 95.71

Number 7 7 Standard

Deviation 1.890 1.890

Here we will discuss the other results we have got throughout the interviews.

From SK+F, they said that the new students or entrants are somehow capable for operating business functions but they have inefficiency in case of research. Another thing to mention is that pharmaceuticals industries are merely capable of producing some APIs, not really for molecular formulation. Sometimes the industry hires some experts from outside but all the operators are being recruited here.

From Cosmic, we came to know that in Bangladesh now has the only capability of producing some APIs but still DDA is not being careful of that. Market is totally captured by first and second generation companies and third generation companies even multinationals are facing problems to have a sound market entry. Government should take necessary steps regarding that.

Beacon Pharmaceuticals came up with the information that we are producing APIs, but in a very limited capacity and on the other side no equipment is served locally. To make a research on these it will need almost 25 years to make a settlement.

Ultra Pharma said about the education quality. From there we got the information that BPC (Bangladesh Pharmacists Council) has stopped licensing any pharmacist whether s/he is coming from public university or private university that doesn’t matter, students need practical experience, and without license they cannot get into industry, this is a complex situation, because private university students don’t get used to learn better and they don’t have any practical implementation in their education life. So to avoid inexperienced students, BPC is making this complexity.

ACME said about patent rights, we are losing the

opportunity. After 2016 this will make us barring to get the

formulas of drugs and we will need to buy at a very high rate.

This is going to catch our industry down, and multinationals

will have a greater opportunity. Another thing they informed

us that to develop research facilities three types of tests –

bioequivalence test, clinical test and market research, will need

a huge amount of investment and this is highly risky. This is

why still we don’t have competency to cope up with this.

SQUARE also informed us about the patent rights problem.

Another thing they told us that student can perform well but

they aren’t nurtured to make a development research.

Beximco Pharma told us about the investors, they are not

intending to invest in the high risk process to develop or

research for any newer drug. This is why some organizations

with limited scopes are producing some APIs like

paracetamols, excipients which includes antibiotics and salts.

5.2 Facts behind

Through interviews we have come to learn about these follow- ing facts –

• Within 2016 patent rights will be established, for this reason our industry is going to face a huge back log into produc- tion if there is no innovation.

• Private universities are not maintaining required facilities to train and prepare students; this is why BAPI is now stop- ping licensing pharmacists without experiences records. This is also affecting public university students.

• Pharmaceuticals industries in Bangladesh are merely capa- ble of producing some API, but they are not capable to in- vest into research and development to develop new mole- cules of their own to compete. This is why 2016 is coming with a bigger threat to this industry.

• Directorate of Drug Administration of Bangladesh is con- servative and outdated. It needs both infrastructural and cultural development to cope up with newer business and production challenges.

• Market is totally captured with first and second generation pharmaceuticals organization, third generation organiza- tions are not getting shield to enter into market to compete without a huge investment. Even multinationals are not get- ting that competitive advantage.

5 CONCLUSION

At the end of the day, pharmaceuticals industry in Bangladesh is very emerging and promising sector, but nobody knows what will come after 2016 through the local firms. Now multinationals are facing challenges from local organizations into market, but after losing advantages, local organization may fall down in competition. But still investors are not looking for newer molecule development through research for high risk. Without this investment our educational institutions are not gaining capabilities to provide the best trainings could be, though students are passing out there enough skilled to operate but not to research and develop new technologies. There is no usage of our local invented technology in the pharmaceuticals sector in Bangladesh.

ACKNOWLEDGMENT

First of all, our thankfulness to our Almighty. Our greatfulness is to Mr. Noor Un Nabi currently working as research associate in University of Leipzig for giving such an opportunity to run this research, and our classmates of 17th batch of BBA Program in Khulna University, Bangladesh to help and encourage us to make this research most successful. Besides these we are also very thankful to those associates of pharmaceuticals industry in Bangladesh who helped us a lot by giving us so valuable information and spent time for us. And at last thanks to our family members for great support.

IJSER © 2011 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 2, Issue 4, April-2011 9

ISSN 2229-5518

REFERENCES

[1] Directorate of Drug Administration, Bangladesh (http://www.ddabd.org/)

[2] Nabi, Md. Noor Un and Dornberger, Utz, “Emergence of Industry and Insufficient Institutions – Development of the Generic Pharma- ceuticals Industry in Bangladesh”, 2010

[3] Bobhate, Shailendra, “Open for Trade – Bangladesh offers fertile ground for Zuellig Pharma’s distribution ambition in South Asia”, The Market Partner (Zuellig Pharma Asia Pacific), pp.14-17, Issue 48 | April

2010

[4] World Bank Data Bank (http://databank.worldnank.org/)

[5] Gehl Sampath, P., “Innovation and Competitive Capacity in Bangla- desh’s Pharmaceuticals Sector”, UNU-MERIT Working Paper No. 2007-

031, United Nations University (UNU) – Maastricht Economic and Social Research and training center on Innovation and Technology (MERIT), The Netherlands, 2007

[6] Azad, Abul K., “Bangladesh Pharmaceutical Sector: Present and Po-

tential”, BAPA Journal, July 2006

[7] Bangladesh Bank Export-Import Data (http://www.bangladesh- bank.org/)

[8] Foreign Trade Statistics of Bangladesh Reports, Bangladesh Bureau of

Statistics (http://www.bbs.gov.bd/)

[9] Human Development Unit, South Asia Region, The World Bank, “Public and Private Sector Approaches to Improving Pharmaceuticals Quality in Bangladesh”, Bangladesh Development Series (Paper No. 23), March 2008

[10] Trade Programme, Division Economic Development and Employment,

Division Agriculture, Fisheries and Food, GTZ, Study on the Viability of

High Quality Drug Manufacturing in Bangladesh, 2007

IJSER © 2011 http://www.ijser.org