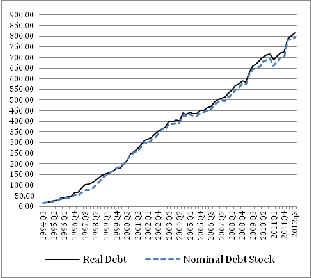

Figure 1: Real and nominal quarterly debt stock 1992-

2012 (in mio USD)

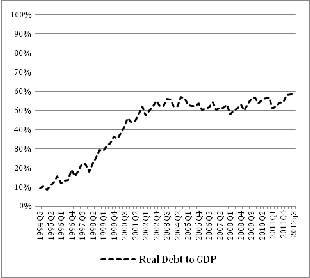

Figure 2: Real Debt to GDP ratio 1992-2012 (in %)

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 1979

ISSN 2229-5518

Areta Dymleku (Allamani)

Abstract-- Albania economy has undergone differenet turbulances from the time it introduced market economy and entered transition. Debt sustainability and financial performance of governments are debated and overlooked indicators today, given the fact that unsustainable public debt drove many economies into recession or buncraptcy.At the verge of financial crisies that emerged in 2008, Albanian economy was experiencing a fats growth (growth rate of around 9%) and faced no difficulties in ensuring a sustainable debt to GDP ratio. This study aims to examine the sensitivity of fiscal polic y to public debt dynamics by estimating the fiscal reaction function. The long and short term reaction of government budget balance (fiscal policy) to public indebtness is examined through a VEC model, given that primary balance and public debt are co-integrated time series of the same order. The analyses are based on the quarterly time series (1995-2012) of budget balance, debt to GDP ration, inflation and dummy variables to track the political events influence on the fiscal policies.

Index Terms: Public debt, debt sustainability, fiscal reaction function, primary balance

—————————— ——————————

Debt sustainability and financial performance of governments are debated and overlooked indicators today, given the fact that unsustainable public debt drove many economies into recession or buncraptcy. Bohn (1995) in his seminal paper argued that public debt series turn sustainable over time, as long as primary balance (primary surplus) reacts to the debt dynamics. He argued that the relation between dynamics of the public debt and fiscal policy is very important for understanding debt sustainability.

Since Albania was introduced to free market and entered transition, its economy faced continues fluctuations through those years. At the verge of financial crisies that emerged in 2008, Albanian economy was experiencing a fats growth (growth rate of around 9%) and faced no difficulties in ensuring a sustainable debt to GDP ratio. The downturn of economic situation in Greece, Italy and overall EU block affected the Albanian economy. The fiscal policy designed in 2008, was mainly expansiory and was aiming to maintain the growth pace, but is also caused a high level of public debt.

Albanian government in 2013 approved an extension of the

public debt to GDP ratio from 60 to 63%, the growth rate has declined to a modest level of around 2.2%, and the economy is still dry of liquidity.

This paper objective is to examine the sensitivity of fiscal policy to public debt dynamics by estimating the fiscal reaction function. The long and short term reaction of government budget balance (fiscal policy) to public indebtness is examined through a VEC model, given that

primary balance and public debt are cointegrated time series of the same order. The analyses are based on the quarterly time series (1995-2012) of budget balance, debt to GDP ration, inflation and dummy variables to track the political events influence on the fiscal policies. The analyses does not cover a long time span, due to data limitations. It, however, covers a time of interesting decisions regarding fiscal policy in a country of weak macro stability, under structural trasnition, with volatile and unstable growth. Evidence on sustainability of public debt checked through the time series properties of real debt to GDP, were weak and inconclusive. Debt and primary balance were co- integrated series of the same order and a Vector Error Correction model

was run. The fiscal reaction function was estimated OLS,

GMM and VAR method. The results were used to run the

Bohn test of debt sutainability.

The public debt in nominal terms in Albania was barely visible in early 90s and its ratio to GDP was at a modest rate of xx%, when the centralized economy broke and the open market economy was installed in the country. The main factors keeping the public debt at such low level were related to the low pace of development of the economy, the public sector shrinkage, foreign aid capital flows as well as lack of financial instituional and weak regulatory

framework for supporting public sector financing through

different financing instruments.

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 1980

ISSN 2229-5518

Figure 1: Real and nominal quarterly debt stock 1992- 2012 (in mio USD) | Figure 2: Real Debt to GDP ratio 1992-2012 (in %) |

|

|

Source: Ministry of Finance Public Finance (Public Debt Managment data) and author’s calculation

In 1995, after Albania went through the fist stage of shock therapy, the main structural reforms and the economy started to revive public debt entered into a positive

growing path with cycles of debt stock change closely related to political and economic situation.The political turbulences in 1997 and the economic caos caused by the crash of the pyramid schemes mark the first abnormal

variation in the quterly public debt, with declining debt level and debt to GDP ration. The after 1997 debt level has increased continously, debt to GDP ratio has also increased

noticable after 1998, until 2005 when the debt to GDP ratio was approaching the threshold of 60% and caution has been shown in fiscal policy design to keep the debt stock change at moderate level and ensure stability.

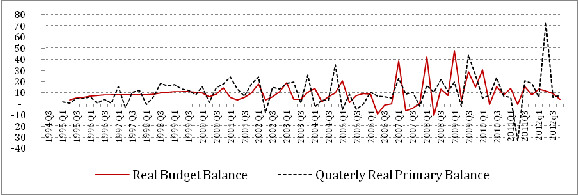

Figure 3: Quarterly real budget balance and primary balance (in Ml USD)

Source: Ministry of Finance Public Finance (Public Debt Managment data) and author’s calculation

However caution the fiscal policy was designed, the debt to

GDP value is now quite sensitive, small changes in debt level do cause debt to GDP ratio a high upward move because of the low growth rate of the economy and the edgy situation public debt has reached. The question of

what cycle of dynamics has the public debt entered, and

how responsive the government is to debt dynamics to ensure debt sustainability is quite crutial for the macrostability of the country. Comparing debt stockchange and budget balance indicates comovement of

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 1981

ISSN 2229-5518

both variables and signs of a responsive fiscal policy to debt dynamics. The paper aims to further explore the

sustainability of public debt and the responsiveness of the fiscal policy through more rigorous techniques.

Intertemporal budget constaint of the government is used to derive the link between debt and fiscal policy and then identify theoretical conditions that ensure debt sustainable path. Government budget constraint at time t, states the simple fact that debt stock at time time is equal to previous debt, debt serving costs and the budget deficit/surplus (equation 1).

![]() (1)

(1)

Using equation 1 to derive present value of future debt by forward substituting and expectation operations and imposing the transversality condition an equilibrium state where debt stock equals to the sum of discounted future primary deficit/surpluses is reached. Expressing this condition in GDP terms, one arrives at a relational expression between primary budget balance and public indebtness (equation 2) where bt is the public budget balance ratio to GDP at time t, rt , gt are the real interest rate, real growth dt is debt stock to GDP at t-1.

![]() (2)

(2)

This equation can be interpreted as a fiscal rule, defining

the primary budget balance to GDP that ensures debt sustainability. (Burger et al, 2011) A fiscal reaction function can therefore be estimated using primary public deficit and public debt.

![]() (3)

(3)

![]()

with being an approximate for the term ![]() .

.

The empirical work will consist on estimating a fiscal

reaction function as in equation 3, augmented with other controll variables to account for other economic or political factors determine the fiscal policy. Output gap and public expenditure outlays are included in the model as control variables, they cover the dependance between fiscal stance and business cycles. (Bohn 2007; De Mello 2005). Because variables in nominal terms might lead to inconclusive results due to the trend component (or non-stationarity) in the analyses we have used real data (denomanated by the price index).![]()

(4)

We expect primary budget balance(expenditures-income) to react to public indebtness. The absolute value of the coefficient ![]() and

and ![]() are important indicator on the sustainability of public debt. Corrective actions of fiscal authorities can be found by examine these coefficients. A positive response shows that the government is taking actions to reduce public spendings or raise revenues to counteract the dynamics of public debt.

are important indicator on the sustainability of public debt. Corrective actions of fiscal authorities can be found by examine these coefficients. A positive response shows that the government is taking actions to reduce public spendings or raise revenues to counteract the dynamics of public debt.

If the change in government budget balance in response to indebtness is lcloser to the value of the

term , it mean that government is trying to adjust

its primary balance to ensure debt converges to its previous period level and ensure a stationary debt to GDP.

Quarterly data on public consolidated budget, including income, expenditure and primary balance as well as quarterly debt data are made available from the Ministry of Finance. Public expenditures include debt service as well as expenditures done at local government level. Data on gross domestic product and inflation are provided by the National Statistical Office (see appendix 1 for descriptive statistics).

The debt sustainability and time series properties of the data will be treated carefuly in the analyses. The fiscal reaction function will be estimated through three different methods OLS, GMM and VAR. Time series properties of primary budget balance and debt to GDP will be examined through unit root tests, and short run vs long run relations between debt and primary budget balance would be estimated through a VEC model.

This part of the emprirical analyses focuses on time series

properties (on their stationarity) of real public debt, real

expenditure, real income and real primary balance. Unit

root tests and cointegration analyses were performed and the results are used to derive insights on sustainability of public debt. The tests were run on real variables, GDP ratios. The results on stationari property of the GDP ratios are summarised and discuseed. Three tests were used to asses the unit root properties of the data, augmented- Dickey-Fuller test with intercept and a 4-lag structure, the Philip-Perron (PP) test with an intercept and a 3 lag structure and the KPPS test.

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 1982

ISSN 2229-5518

Table 1: Unit Root test

significant cointegration relation between budget balance and public debt (expressed as ratios to GDP, see table 2 for test result). Trace and max-eigenvalue statistics indicate one cointegration equation at 0.05% level of significance.

Table 2: Cointegration Test

Number of Cointegra tion Equation | Eigenvalu e | Trace Statistic | Critical Value | P- Value |

None* | 0.3764 | 37.481 | 25.871 | 0.001 2 |

At most 1 | 0.083 | 5.836 | 12.517 | 0.481 |

Eigen value | Max-Eigen Statistic | Critical Value | P- value | |

None* | 0.376 | 31.645 | 19.387 | 0.005 |

At most 1 | 0.083 | 5.8356 | 12.517 | 0.481 |

*rejection of hypothesis at 5% level fo significance

UR- Unit Root/NUR – No Unit Root, S/NS – stationary/non stationary

Inconclusive results, as ofenly faced in the literature are found after running unit root tests. The real debt to GDP series appear to be a non-stationary one, but given the short time span covered by the analyses, the frequency of economic fluctuations and the strong positive trend of the public debt during 2004-2009 supported by the fast growing economy do influence the results. The stationary ptoperties of other variables does conflict with the non- stationarity of the public debt, non-stationarity of public expenditure and revenues can be confidently proved by the unit root. Expenditure and income are non-stationary only based on the ADF test, PP test and KPSS tests do give conflicting signals concerning stationary/non-stationanry. In search of evidence for Trehan and Walsh (1988) condition, which states that if real revenues, real spending, and real debt have unit roots, a stationary deficit is sufficient for a sustainable debt, the conflicting results do not help. Real budget balance to GDP appears stationary only under PP test, ADF and KPPS reject the hypotheses of a stationary budget balance.

Real debt to GDP and real budget balance are integrated of

the same order (I(1)), and contegration test shows there is a

Trehan and Walsh (1988), in their paper support the hypothesis of contegrated debt and primary public balance and if fiscal policy is responsive to debt dynamics, than an

error correction term would be found in the data, so a VEC

model will be estimated to identify error correction term.

The fiscal reaction function estimation in various methods are run to confim outcome of the results. The model explains modestly the variation of the primary budget balance, but the influence of debt into fiscal policy is robust. The debt to GDP ratio (coefficient a2) is in all set ups of the model and method of estimations significantly related to primary budget balance, confirming the fact that fiscal policy decisions have taken into account indebtness level. The primary budget balance lagged coefficient shows a high flexibility of government in adjusting its budget, and in fact the budget reviews for the last three years have been almost of a quaterly frequency to adjust to the spendings and revenue cycle as well as to accomodate the increased debt.

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 1983

ISSN 2229-5518

Variables | Baseline (OLS) | Model 1 (OLS) | Model 2 OLS | Model 2 VAR | Model 2 GMM |

Constant | -0.037 (-7.582) | -0.037 (-7.59) | -0.038 (-7.417) | -0.038 | -0.039 (-15.859) |

Real Primary Budget Balance (Lag,1) | -0.2 (-1.76) | -0.214 (-1.853) | -0.21 (-1.77) | -0.21 (-1.807) | -0.28 (-3.882) |

Real Debt to GDP (Lag, 1) | 0.044 (5.053) | 0.036 (2.789) | 0.039 (2.602) | 0.039 (2.589) | 0.0405 (3.947) |

Output Gap1 (Lag,1) | 0.0000003 (0.817) | 0.0000004 (0.704) | 0.0000004 (0.702) | 0.0000004 (0.89) | |

Outlays Gap (Lag,1) | -.0000008 (-0.38) | -.0000009 (-0.382) | -.00000077 (-0.392) | ||

Election Dummy | -0.000037 (-0.011) | 0.0004 (0.124) | -0.0004 (-0.285) | ||

R-Square | 0.27 | 0.28 | 0.29 | 0.28 | 0.28 |

Adjusted R-Square | 0.25 | 0.25 | 0.23 | 0.23 | 0.23 |

F-Statistic | 12.8 | 8.716 | 5.114 | 5.118 | |

Durbin-Watson | 2.1 | 2.1 | 2.11 | 1.99 | |

Number of Observation | 70 | 70 | 70 | 70 | 70 |

![]()

1 HP generated output gap and expenditure gap

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 1984

ISSN 2229-5518

Output gap, as measures of the economic cycles are not playing a significant role on government decision on its decision on budget, mostly because the time span we looking at has been characterized by high growth rates, moreover the high degree of informality and low rate of tax collection keep public revenues not very dependant on business cycles. The informal economic activity is being narrowed and economic situation of persistant low growth rate will influence the influence of economic cycles on fiscal planning (revenues and expenditures). Political cycles are as well not a significant influence on primary budget balance, stable revenues have supported political cycles of increased public expenditures.

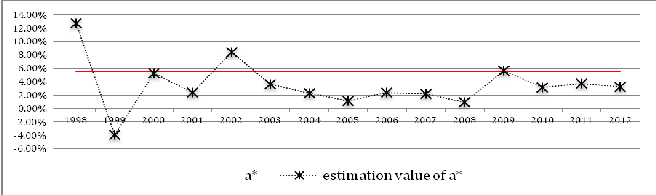

Using the baseline estimates of α1 and α2 coefficients, we have calculated the α* coefficient and compared it with the historical value of the primary-debt theoretical coeffient of dependency ![]() . 12-month treasury bill interest rate at each

. 12-month treasury bill interest rate at each

year and real annual growth rate of GDP were used as approximation for the interest rate and growth factor of the debt-primary balance coefficient of relation. The results show that Albanian government has run under stable path of debt dynamics most of the time, supported by strong growth, however there has been cases when the decision fiscal policy have risked the sustainability of public debt (in

1998, in 2004 and 2009). This have actually been elections years with high public spendings and debt. In 2009, the high growth of the economy was significantly slowed down due to the world economic downturn, and this was an aditional factor along side political elections that drove the level of indebtness to the verge of unstable dynamics. The government has intervene after 2009 with strong fiscal measures to keep expenditures under strick control, keep the debt to GDP ratio under the threshold of 60% (see figure 4)

Figure 4: Bohn test on sustainability of public debt

Source: Author calculations

Table 4: VEC Results

Cointegrating Equation | |

Real Primary budget Balance (Lag,1) | 1 |

Real Debt to GDP (Lagged,1) | -0.028*** (-4.728) |

Constant | 0.0276 |

Error Correction Equation | D(Real Primary budget Balance) |

Co-integrating Equation | -1.92*** (-8.028) |

D(Real Primary budget Balance (Lag,1)) | 0.47*** (2.519) |

D(Real Primary budget Balance (Lag,2)) | 0.34*** (2.86) |

D(Real Debt to GDP (Lagged,1)) | -0.14*** (-2.49) |

D(Real Debt to GDP (Lagged,2)) | -0.029 (-0.506) |

Constant | -0.004 |

IJSER © 2013 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 4, Issue 12, December-2013 1985

ISSN 2229-5518

(-1.25) Output Gap(-1) 0.0000003*

(1.96)

Election Dummy -0.0006 (-0.2)

![]()

R-Square 0.71

Adjusted R-Square 0.68

The Vector Error Correction estimation do confirm the

influence of debt dynamics on budget balance (fiscal policy, mainly expenditure level and deficit). The long run relation between debt and primary budget balance at the contegration part of the estimations shows that an increase of debt to GDP ratio by 1% will increase the budget balance (deficit) by 0.028 percent.

The error correction term of the primary balance is

significant and indicates a responsive fiscal policy to

deviation of from the long run budget balance. The primary budget balance is influenced by the debt to GDP ration in short run, significatly, but at “one time scenario”. If debt increases the reaction in short run is an immediate measure to stabilize. Political cycles are not identified as a factor of influence in short run, while business cycles (or economic activity quaterly fluctuation, measured by HP filter on quaterly GDP) do influence primary balance, mainly through the quaterly public revenue level, which influences the decision on spendings and the budget balance.

6. CONCLUSION

The dynamics of the public debt in Albania during the

economic transition and the years of fast economic growth

(1993-2012) do not put at risk the sustainability of debt and the macroeconomic stability, in general. However there is evidence that at time interval the debt was driven at the edge of unstable dynamics. These shocks to the public debt were not persistent and corrective actions from the fiscal authorities have turned the debt into stable path.

The time series properties of the debt to GDP ration were

inconclusive on the sustainability of the public debt, mainly

reflecting the influence of high fluctuations of debt in 1997,

2004 and 2009.

The increasing public debt that Albania has experienced after 1998 was able to remain into a stable path (not exploding, no unit root and sustainable) mainly due to two main factors – strong growth rates of private economic activity and strict control over public expenditures, mainly over public investments. The fiscal reaction function estimated showed clear evidence of the fiscal policy reaction to dynamics of indebtness. Bohn test confirms that policy intervention combined with economic growth have been able to eliminate exploding public debt dynamics and return debt to GDP into stable dynamics

[1] BOHN, H. 2007. Are stationary and co integration restrictions really necessary for the inter-temporal budget constraint? Journal of Monetary Economics, 54, pp. 1837-47

[2] BOHN, H. 1998, “The behavior of US public debt and deficits”. The

Quarterly Journal of Economics, 113 (3), pp. 949-63. [3] Bank of Albania “Annual report” 1993

[4] Bank of Albania “Annual report” 1994 [5] Bank of Albania “Annual report” 1995 [6] Bank of Albania “Annual report” 1996 [7] Bank of Albania “Annual report” 1997

[8] Bank of Albania “Annual report” 1998 [9] Bank of Albania “Annual report” 1999

[10] Bank of Albania “Annual report” 2000-2012

[11] DE MELLO, L. 2005. Estimating a fiscal reaction function: The case of debt sustainability in

[12] Brazil. OECD Economics Department Working Paper No. 423. OECD, Paris.

[13] Ministry of Finance – Fiscal Indicators Report, 1999-2012 [14]“Sustainability of Public Debt” CES info Seminar Series, The MIT Press, 2008

IJSER © 2013 http://www.ijser.org