International Journal of Scientific & Engineering Research Volume 3, Issue 4, April-2012 1

ISSN 2229-5518

Enabling Poor People to Overcome Poverty and Innovative Access to Finance for Small and Medium Enterprises in the United Republic of Tanzania by Rotating Savings and Credit Association Method.

A. Ranjith, R.Thandaiah Prabu, P. Albert Shelton

Abstract— The United Republic of Tanzania is an emerging economy with high growth potential. W ith per capita gross domestic product (GDP) of US$500, the economy has shown strong and consistent growth in the last two decades the Tanzanian economy went through a period of successful transition in which economic liberalization and institutional reform led to a recovery of GDP growth to more than 7% per year since 2000. However, during the same period, the country has been unable to achieve significant reductions in poverty. Approximately 90 per cent of the United Republic of Tanzania’s poor people lives in rural areas. The incidence of poverty varies greatly across the country but is highest among rural families living in arid and semi-arid regions. The main aim of this paper is to enabling poor rural people to overcome poverty and increase their savings by introducing The Rotating Savings and Credit Association (Rosca) method. It plays an important role as a financial intermediary in many parts of developing countries. It flourishes in both urban and rural settings, especially where formal financial institutions seem to fail to meet the needs of a large fraction of the population.

Keywords— Roscas, upatu, bid, poverty, loan, MDG and household

—————————— —————————

1 INTRODUCTION

N Tanzania, this in 1999 ranked 156 out of 174 countries in the Human Development Index (HDI),

53% of the population is below the age of 18. It is estimated that Tanzania’s economy must grow by 7% per annum. 51% of the population lives on less than $1 a day. About half or 42% of these live in absolute poverty on less than $0.75 cents a day [12].A popular and useful definition of a poor person is someone who doesn't have much money. Among academics, and in the aid industry, this definition has gone out of fashion. Poor people can save and want to save, and when they do not save it is because of lack of opportunity rather than lack of capacity. During their lives there are many occasions when they need sums of cash greater than they have to hand, and the only reliable way of getting hold of such sums is by finding some way to build them from their savings. They need these lump sums to meet lifecycle needs, to cope with emergencies, and to grasp opportunities to acquire assets or develop businesses.

————————————————

A. Ranjith & R. Thandaiah Prabu are currently working as a lecturer in school of electronics and telecommunication engineering in St.Joseph College of Engineering and Technology, Tanzania.

Mobile: +255 714949729, +255 656023085.

E-mail: aranjithece@ gmail.com, thandaiah@gmail.com.

P. Albert Shelton is currently working as a lecturer in Mechanical

engineering in St.Joseph College of Engineering and Technology, Tanzania. Mobile +255 652325117, E-mail: albertshelton85@gmail.com

The job of financial services for the poor, then, is to provide them with mechanisms to turn savings into lump sums for a wide variety of uses (and not just to run microenterprises). Good financial services for the poor are those that do this job in the safest, most convenient, most flexible and most affordable way. The poor seek to turn their savings into lump sums by finding reliable deposit takers, by seeking advances against future savings (loans), or by setting up devices like savings clubs and ROSCAs [4].

ROSCAs are a means to ‘save and borrow’ simultaneously. Rotating Savings and Credit Associations can be found all over the world and go by different names in different regions and countries. In broad terms, a ROSCA can be defined as ‘a voluntary grouping of individuals who agree to contribute financially at each of a set of uniformly-spaced dates towards the creation of a fund, which will then be allotted in accordance with some prearranged principle to each member of the group in turn’ [2]. It is considered one of the best instruments to cater to the needs of the poor.

Upatu are the Tanzania equivalent of the Rotating Savings and Credit Associations (ROSCA). It enables poor people to convert their small savings into lump sums. The concept of upatu originated more than 1000 years ago. Initially it was in the form of an informal association of traders and households within communities, wherein the member contributed some money in return for an accumulated sum at the end of the tenure.

IJSER © 2012 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 3, Issue 4, April-2012 2

ISSN 2229-5518

Participation in Upatu was mainly for the purpose of purchasing some property or, in other words, for consumption purposes [3].

ROSCAs are found worldwide (like Asia, Latin America, and the Caribbean Africa) in countries with vastly different levels of economic development [6]. ROSCA participation is high in Africa [5]. These estimated that, in Central African countries, about 20% of household savings are accumulated in informal ROSCAs [15]. A sample of 115 households in central Kenya showed that

45% were participating in a ROSCA [7]. In a sample in urban Zimbabwe 76% of urban market traders participate in a ROSCA; even though 77% of these traders have a banking account [8]. Taiwan with relatively well functioning credit markets as many as 80% of adults is estimated to belong to ROSCA [9]. ROSCA can provide a commitment mechanism that ties participants hands and commits them to saving patterns and sometimes to spending patterns as well [5]. Several commitment devices that villagers in East Africa use to stick to saving plans, including buying a lock box and throwing away the key [1]. ROSCA is one of the vital methods in various countries to reduce poverty and increase saving potential. The main objective of this paper is to reduce the poverty percentage in Tanzania and increase the participant’s percentage in ROSCA like the above mentioned countries.

2 PRELIMINARIES

In this section, w e first state the number of people in poverty, population and housing census of Tanzania, changes in the poverty head count in selected countries.

Overall, in the 16 year period between 1991 and 2007, poverty fell by about 5%. From the table1 There are more poor people today than in 2001 While the percent of people living in poverty (i.e. on less than Tsh.500/- per person per day) went down slightly since 2000/1, because the population has increased, the total number of people living below the poverty line increased by 1.3 million in the same period. Tanzania has signed up to the Millennium Development Goals (MDGs). The First MDG commits Tanzania to reduce poverty between 1990 and

2015 by 50%. In 1991/92 poverty was 38% in Tanzania, so the objective is to reduce poverty to 19% by 2015 [10].

TABLE I

NATIONAL BUREAU OF STATISTICS 2001 & 2007

In Tanzania, the latest population and housing census that covered all regions was carried out in 2002. The 2002 census was preceded by three other post- independence population censuses which were conducted in 1967, 1978 and 1988[11].The above table shows that United Republic of Tanzania, 2002 Population and Housing Census. From Table II Mwenza, Dar es Salaam and Mbeya region has the highest population when compared with other region [11].

TABLE II

UNITED REPUBLIC OF TANZANIA,

2002 POPULATION AND HOUSING CENSUS

Year | Population (Tanzania main land) | Poverty rate (%) | Number of people in poverty |

2001 | 32.4 | 35.6 | 11.5 |

2007 | 38.3 | 33.4 | 12.8 |

IJSER © 2012 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 3, Issue 4, April-2012 3

ISSN 2229-5518

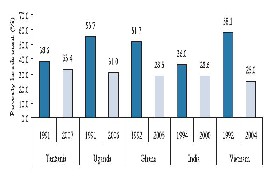

From the figure1Tanzania’s performance in poverty reduction compares poorly relative to comparator countries which like Tanzania were relatively stable and who underwent macro-economic reform in the region (Ghana, Uganda) and in Asia (Vietnam and India). Whereas in Tanzania headcount poverty declined by 2.4% between 1991 and 2007, it dropped in Uganda, Ghana and Vietnam by 10 times as much: approximately 23 to 24%. India too achieved a much higher reduction in poverty (by 7%) over a much shorter period [10].

FIGURE1: CHANGES IN POVERTY HEADCOUNT IN SELECTED COUNTRIES.

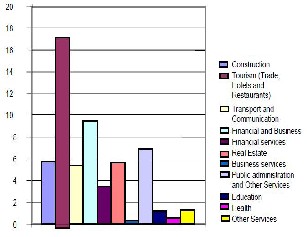

FIGURE2 :PERCENTAGE OF CONTRIBUTION OF SERVICES SECTOR TO

GDP IN 2006.

The above figure2 shows Percentage of contribution of services sector to GDP in 2006. The highest contribution service from Tourism(Trade, Hotels and restarunt). In case of financial and business approx 5-6%. Financial service approximately 3-4%. In this paper we focus on providing funds to the low income households and reduce their poverty and increase their saving potential by Rotating Savings and Credit Association method. By introducing this method percentage of contribution of financial service sector to GDP will increase. This method will be useful to achieve the target of the MKUKUTA (reduce poverty between 1990 and 2015 by 50 %.).

It is difficult to predict a random ROSCA as a series of loans and debt repayments [3]. The bidding allotment mechanism allows member to obtain a upatu when an unexpected opportunity or emergency arise, albeit at the cost of a discount [14]. Thus, in a certain world, a random Rosca is preferred by identical individuals desiring to overcome indivisibilities in consumption, while a bidding Rosca is superior in responding to heterogeneity among its members [13]. In contrast, the bidding ROSCA illustrated in Table3 suggest that bidding ROSCA elements of lending and borrowing. There are 12 people who come together and form a group. Each one will contribute Tsh.10000/- per month and this will continue for next 12 months (equal to number of people in the group). In this group there will be one organizer, who will take the pain of fixing the meetings, collecting money from each other and then doing other procedures. To generate the pot of Tsh. 120000/- for example the organizer would gather six other participants and require that each (plus himself/ herself) contribute Tsh.10000/- monthly. So each month all these 12 people will meet on a particular day and deposit Tsh.1,0000/- each. That will make a total of Tsh.120,000/- every month. At the end of the first rotation of contribution by seven participants, the organizer receives the Tsh.120000/- pot (including Tsh.10000/- of his own funds). In the second rotation naturally there will be few people who are in need of big amount because of some reason like some big expenses, liquidity crunch, business problem etc. Out of all the people who are in need of money, someone will bid the amount, depending on how desperate he/she is for this money. The person who submits the highest bid for the rotation receives the pot. Suppose out of total 6 people who bid for Tsh.500/-, Tsh.750/- and Tsh.1,000/-, the one who bids the highest will win. In this case it’s the person (P2) who has bid Tsh.1,000/-. The high bid amount Tsh.1000/- will be deducted for the rest of the person (P3 to P12) so each person (P3 to P12) will contribute Tsh.9000/- for the second rotation. Hence participant P2 receives the total contribution for the second rotation Tsh.110000/-. So here you can see that the main winner took a big loss because of his desperate need of getting the money and others benefitted by it. So each person actually paid just Tsh.9000/-, not Tsh.10000/- in this case (they got Tsh.1000/- back). Note that when a person takes the money after bidding, he/she can’t bid from next time, only rest of the people will be eligible for bidding. Now next month the same thing happens and suppose the best bid was Tsh.1500/- , then winner will get Tsh.106500/- this is illustrated in table3 and the Tsh.1500/- will be reduced to people (P4 to P12). So each person (P4 to P12) is paying effectively Tsh.8500/-. This way each month all the people contribute the money, someone takes the money by bidding highest and the rest money is deducted back to members.

IJSER © 2012 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 3, Issue 4, April-2012 4

ISSN 2229-5518

TABLE III

ROSCA BIDDING SYSTEM BASED ON TWELVE PARTICIPANTS

Members | Contribution by Month (in Tsh) | Total paid | Net gain (loss) | |||||||||||

High Bid | 1000 | 1500 | 2000 | 1000 | 1500 | 1000 | 2000 | 1500 | 1000 | 2000 | - | Total paid | Net gain (loss) | |

Round | R1 | R2 | R3 | R4 | R5 | R6 | R7 | R8 | R9 | R10 | R11 | R12 | Total paid | Net gain (loss) |

P1 (Organizer) | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 120000 | 0 |

P2 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 120000 | (10000) |

P3 | 10000 | 9000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 119000 | (12500) |

P4 | 10000 | 9000 | 8500 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 117500 | (13500) |

P5 | 10000 | 9000 | 8500 | 8000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 115500 | (2500) |

P6 | 10000 | 9000 | 8500 | 8000 | 9000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 114500 | (3500) |

P7 | 10000 | 9000 | 8500 | 8000 | 9000 | 8500 | 10000 | 10000 | 10000 | 10000 | 10000 | 10000 | 113000 | 2000 |

P8 | 10000 | 9000 | 8500 | 8000 | 9000 | 8500 | 9000 | 10000 | 10000 | 10000 | 10000 | 10000 | 112000 | 0 |

P9 | 10000 | 9000 | 8500 | 8000 | 9000 | 8500 | 9000 | 8000 | 10000 | 10000 | 10000 | 10000 | 110000 | 5500 |

P10 | 10000 | 9000 | 8500 | 8000 | 9000 | 8500 | 9000 | 8000 | 8500 | 10000 | 10000 | 10000 | 108500 | 9500 |

P11 | 10000 | 9000 | 8500 | 8000 | 9000 | 8500 | 9000 | 8000 | 8500 | 9000 | 10000 | 10000 | 107500 | 10500 |

P12 | 10000 | 9000 | 8500 | 8000 | 9000 | 8500 | 9000 | 8000 | 8500 | 9000 | 8000 | 10000 | 105500 | 14500 |

TOTAL RECEIVED | 120000 | 110000 | 106500 | 104000 | 113000 | 111000 | 115000 | 112000 | 115500 | 118000 | 118000 | 12000 0 | 136300 0 | - |

Note: Shaded cell represent the period in which the participants received the pot.

You will realize that the person who takes the money at the end will get all the money because there is no one else to bid now. So the person will get around Tsh.1,20000/- in the end, if you try to find out the returns which he/she got out of the whole deal, it will depend on things, how much higher bids were each month. If bids and charges are very low, then a person will make more money at the cost of other situations.

Figure4: Monthly Cash Flow in Second Month

TABLE IV

CASH FLOW S OF A MEMBER

WHO TAKES THE LOAN IN THE SECOND MONTH

Month | Prized Amount/Loan In Tsh. | Contribution In Tsh |

1 | 0 | -10000/- |

2 | 110,000/- | -10000/- |

3 | 0 | -10000/- |

4 | 0 | -10000/- |

5 | 0 | -10000/- |

6 | 0 | -10000/- |

7 | 0 | -10000/- |

8 | 0 | -10000/- |

9 | 0 | -10000/- |

10 | 0 | -10000/- |

11 | 0 | -10000/- |

12 | 0 | -10000/- |

Using the equation for net present value, the usual approach to finding a loan interest is to set the amount of loan received is equal to the sum of discounted present values of the monthly loan payments made for the term of the loan.

IJSER © 2012 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 3, Issue 4, April-2012 5

ISSN 2229-5518

FIGURE 3: MONTHLY CASH FLOW IN SECOND MONTH

TABLE V

CASH FLOW S OF A MEMBER

WHO TAKES THE LOAN IN THE SEVENTH MONTH

Month | Prized Amount/Loan In Tsh. | Contribution In Tsh |

1 | 0 | -10000/- |

2 | 0 | -90000/- |

3 | 0 | -8500/- |

4 | 0 | -8000/- |

5 | 0 | -9000/- |

6 | 0 | -8500/- |

7 | 0 | -9000/- |

8 | 0 | -8000/- |

9 | 0 | -8500/- |

10 | 0 | -9000/- |

11 | 0 | -8000/- |

12 | 120,000/- | -10000/- |

Using the below equation we can find the monthly interest rate is denoted by r![]()

Where,

p - Principal amount borrowed

A - Periodic payment

r - The periodic interest rate divided by 100 (annual interest rate also divided by 12 in case of monthly installments.

n - The total number of payments (for a 30 years loan with monthly payments n=3*13=360.

We have taken efforts in this journal. However, it would not have been possible without the kind support and help of many individuals and organizations. We would like to extend my sincere thanks to all of them. We are highly indebted to Directors, principal, and member of St.Joseph College of Engineering and Technology, Dar Es Salaam, Tanzania for their guidance and constant supervision as well as for providing necessary information regarding the Journal and also for their support in completing the Journal. We would like to express my gratitude towards my parents and people of Tanzania for their kind co-operation and encouragement which help me in completion of this Journal. I would like to express my special gratitude and thanks to industry persons for giving me such attention and time. Our thanks and appreciations also go to my colleague in developing the Journal and people who have willingly helped me out with their abilities.

The results from this study underscore the importance of savings and borrowing vehicle for the poor and lower income households in Tanzania. ROSCA method is s a very good tool for financing poor people. Especially in a ROSCA, members have quicker access to a large sum of money or a commodity than when saving individually. A further strength of the ROSCA is that it binds the members to save regularly, and thus to accumulate savings. An upatu is not a scalable model unless the upatu manager or company has sufficient personal resources as a backup for financial contingencies. The result in this paper provides strong support about benefit of saving and borrowing money for participants. In future work we plan to implement impact of setting up registered upatu in rural areas, impact of altering collateral/guarantee requirements, developing a credit scoring model for ROSCA. The day when the government and the industry participants alike understand the importance of ROSCA to the economy would mark the beginning of a new era.

[1] Rutherford, Stuart, and others. 1999. “Savings and the Poor: the Methods, Use and Impact of Savings by the Poor of East Africa.” Report prepared for MicroSave- Africa, May 1999.

[2] Calomiris, C. W. and I. Rajaraman, “The Role of

ROSCAs: Lumpy Durables or Event Insurance?”

Journal of Development Economics (1998), pp. 207-216.

IJSER © 2012 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 3, Issue 4, April-2012 6

ISSN 2229-5518

[3] Christy Chung Hevener Federal Reserve Bank of Philadelphia. November 2006. Alternative Financial Vehicles:Rotating Savings and Credit Associations (ROSCAs).

[4] Stuart Rutherford Institute for Development Policy and Management University of Manchester. January

1999.The Poor and Their Money An essay about

financial services for poor people.

[5] Mary Kay Gugerty, Daniel J. Evans School of Public Affairs. “You Can’t Save Alone: Commitment in Rotating Savings and Credit” Associations in Kenya, January 2005.

[6] Ardener, Shirley. 1964. “Comparative Study of Rotating Credit Associations.” Reprinted in Ardener and Burman, 1995.

[7] Kimuyu, Peter Kiko. 1999. “Rotating Savings and Credit Organizations in Rural East Africa,”World Development. 27(7): 1299-1308.

[8] Chamlee-Wright, Emily, 2002. “Savings and Accumulation Strategies of Urban Market Women in Harare, Zimbabwe.” Economic Development and Cultural Change.

[9] Levenson, Alec and Timothy Besley. 1996. “The Anatomy of an Informal Financial Market: Rosca Participation in Taiwan.” Journal of Development Economics, Volume 51.

[10] Policy Forum ’’Growth in Tanzania: Is it Reducing

Poverty?” www.policyforum-tz.org.

[11] United Republic of Tanzania, 2002 Population and

Housing Census.

[12] Tanzania Human Development Report The State of

Progress in Human Resource Development1999. February

2000.

[13] Besley, T., Coate, S., Loury, G., 1993. The economics of rotating savings and credit associations. American Economic Review 83, 792-810.

[14] Stefan Klonner “Understanding Chit Funds: Price Determination and the Role of Auction Formats in Rotating Savings and Credit Associations” New Haven, Connecticut 06520-8269 USA.

[15] Bouman, F. J. A., 1979. The Rosca: financial technology of an informal savings and credit institution in developing economies, Savings and Development 4

(3), 253-276.

IJSER © 2012 http://www.ijser.org