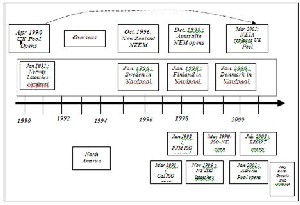

Fig.1. Chronological progression of developments of power markets across the world.

International Journal of Scientific & Engineering Research Volume 2, Issue 4, April-2011 1

ISSN 2229-5518

Electricity Sector Restructuring Experience of

Different Countries

Archana Singh, Prof. D.S.Chauhan

Abstract— Electricity Market from economic, regulatory and engineering perspective is a very demanding system to control

.There is requirement of provision of cost efficiency, lower impact of environment alongwith maintenance of security of supply for use of competition and regulation in the electricity market. Many countries due to failure of its system for adequately management of electricity companies, followed restructuring for its electricity sector. In various countries, different restructuring models were experimented but in the initial phase restructuring was opposed by the parties favouring existing vertically integrated electricity sector. In the paper , restructuring experience of different countries are outlined .

Index Terms—Deregulation, W holesale Electricity Market, Forward Markets, Independent system Operator, Power Exchange.

—————————— • ——————————

Electric utilities have been vertically integrated mo- nopolies that have combined generation, transmission and distribution facilities to serve the needs of the cus- tomer in their service territories. The price of electricity was traditionally set by a regulatory process, rather than using market forces, which were designed to recover the cost of producing and delivering electricity to customers as well as the capital cost. Due to this monopolistic ser- vice regime, customers had no choice of supplier; and suppliers were not free to pursue outside their designat- ed service territories. The main reason for deregulation in developing countries has been to provide electricity to customers at lower prices, and to open the market for competition by allowing smaller players to have access to the electricity market by reducing the share of large state owned utilities. On the other hand ,high growth in demand and irrational tariff policies have been the driv- ing forces for the deregulation in developing countries

.Technical and managerial inefficiencies in these coun- tries have made it difficult to sustain generation and transmission expansions and hence many utilities were forced by international funding agencies to restructure their power industries[1].

Eletricity markets are having a very important characte- ristic of its organizational structure which has been ac- commodated as the most significant change in the in- dustry. Vertically integrated industry structure (a regu- lated monopoly) as the traditional industry structure was owned and operated as a single organization for distribution, transmission, and generation functions[2]. However, the vertically integrated structure, by virtue of the fact that it is a monopolistic structure, is not amend- able to introduction of competition.

Current industry structure primarily requires separate

functions of the generation and distribution (or con-

sumption) from transmission as considering different functions associated with selling and buying electric energy. The reason behind separation of transmission which is the means of transporting the tradable com- modity and ability to influence the transmission- use through, for example, line ratings, line maintenance schedules and network data would be to avoid very powerful competitive advantage to a participant. Beside this, another important function is system operation which is traditionally viewed as a genera- tion/transmission function. This function has evolved to the Independent System Operator (ISO) in the most elec- tricity markets presently which is responsible for coor- dinating maintenance schedules and performing securi- ty assessment.

The deregulation processes have been started with debate for defending the vertically integrated model from opposition by private and state monopolies [3]. The first was Chile to start effort in 1980s for restructur- ing its electricity sector. The most discussed deregula- tion was the British one, with more interest in Norway Model and much attention to actions in Unites States, especially California State. In South America a major transformation took place throughout the electric power industry from 1980 onwards (chronological progress- shown in fig.1).

The electricity sector reform in many developed countries have already undertaken since the 1980s. Initially it was not clear to how to increase efficiency by electricity sector reform. As a matter of fact over various countries, there exists diversity in the wholesale electricity market opera- tion. A transparent, open marketplace would encourage competition among generators and reveal the inefficien- cies of the current system to improve the efficiency of the

IJSER © 2011 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 2, Issue 4, April-2011 2

ISSN 2229-5518

electricity sector.

Fig.1. Chronological progression of developments of power markets across the world.

Hydropower production in Chile varies from 60% to

95%.For supply, there are 4 Gencos with one owned by

State Government. Gencos are dispatched depending on

audited generation costs and reservoir levels.There are 3

Transcos and private 13 Discos. A poolco which is Eco- nomic load dispatch center (CDEC) forecasts global de- mand and updates values monthly.The system operator in charge of coordinating grid operation is run only by

generators favoring the development of several private transmitters. In Chile, wholesale market includes a uni- fied market place, a transport system that “carries” power and market prices defined a spot price for each node along grid. A poolco manages dispatch, reliability and pooling functions .The National Energy Commission (CNE) provides arbitration in the case of disputes [4]. Losses including energy theft were halved in Chile within just seven years and Number of customers per distribu- tion worker has multifolded in ten years after restructur- ing.

Wholesale Electricity Market came into operation in July

1995. Rules promoting free competition in the generation

and commercialization business were implemented.

Transmission and distribution business were treated as

monopolies and competitions were implemented whe- rever possible. For the reservoirs of the national intercon- nected system (NIS) defining minimum operative levels a methodology was ruled. CREG (Energy Regulation

Commission Group) defined limits for the horizontal and vertical integration business. An energy stock market (generator pool) and a central operator (National Dis- patch Centre) of the NIS to support its operation. Transac-

tions between transmission and commercialization bid- ders are made under two modalities which are through subscription of guaranteed bilateral contracts and through direct transcations in the energy stock market

,free offer and demand .Projects of expansion plan are assigned through a scheme of public bids.There is open access to the NTS(National Transmssion System)network [5].

Transmission charges are based on connection charges and use of network charges. Evolution of the electricity sector has multifolded by significant increase in private participation.Competition in commercialization to unre- gulated users has incremented.

Power sector restructuring activities in Argentina started in 1990, resulting in the enactment of the Electric Power Regulatory Frame .It created the National Regula- tory Agency (ENRE) and wholesale Power Market. Transco and Disco required license to operate. Generation developed as free activity in competition and having the transmission network as open access. Marginal declared costs was basis for dispatch on recognition of remunera- tion for capacity as a function of system failure risks. Transport is organized as a monopolistic activity with national network (Transener) and six concessionaires for regional network(Distros);it included concession contract

, transport tariffs based on the economic cost of losses (node factors) and network unavailability (adaptation factors), plus network O &M costs; expansion at the ex- pense of interested parties ;failure penalties as a function of transport charges. It was mandatory for Transport con- cessionaries to provide nondiscriminatory open access to their transmission system. All existing and future load must to be served by distribution concessionaries in their concession area[6]. Wholesale electricity market is under- taken by private company (Cammesa) whose share hold- ers are the associations of generators, distributors, trans- porters, the national state with equal distribution of shares and the large users .

The process of restructuring of the electricity industry in Australia was initiated in 1991, and by 1998 a National Electricity Market was developed, where the National Electricity Management Company (NEMCO) acted as both the ISO and IMO. Generators could sell energy ei- ther by bidding in the spot market, or through formal (bilateral) contracts. The most extensive restructuring is occurring in the South Australia, Victoria, New South Wales and Queensland to form National Electricity Mar- ket (NEM).The key aspect of transition process were like elimination of barriers to entry and of barriers to trade between states, creation of pool style (bulk electricity

IJSER © 2011 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 2, Issue 4, April-2011 3

ISSN 2229-5518

market) competitive entities in generation and in retail supply and development of regulatory arrangements ap- propriate to the new regime [7]. Table1 below summariz- es the deregulated structure in Australia.

Table1.Electricty Restructuring in Australia

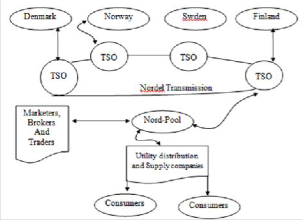

In Norway, the electricity reforms were initiated in 1991. In 1993, Nordic power exchange was established as an

independent company. Swedish electricity market un- bundled in 1996. Thereafter, a common electricity ex- change for Norway and Sweden was established under the name of Nord Pool. In 1998, Finland effectively en- tered into Nordic Market[8]. Denmark joined Nord Pool subsequently. Nord Pool is owned by the Transmission System operators (TSO) of Norway and Sweden. Nord Pool provides freedom of choice to the large consumers. It organizes trade in standardized physical and financial power contracts. Close cooperation between the system operation and market operation is the key feature of Nord Pool. Major contractual relation among Nordic countries is given in figure 2.

Fig2. Nordic Market – Major Contractual Relationship

(i) Nord Pool Spot :

It consist of Nord Pool Spot AS and its wholly owned subsidiary Nord Pool Finland Oy, operates the physical day-ahead market Elspot in whole Nordic region and the physical intra-day market Elbas in Finland, Sweden and Zealand (Eastern Denmark). Elspot and Elbas are Nord Pool Spot auction based markets for trade in power con- tracts for physical delivery. On Elspot, hourly power con- tracts are traded daily for physical delivery in the next day's 24-hour period. On Elbas, continuous adjustment trading in hourly contracts can be performed until one hour before the delivery hour. Its function is to be the aftermarket to the Elspot market at the Nord Pool.

(ii) Nord Pool ASA - Financial Market :

Nord Pool Financial market is a regulated market place which trade in standardized derivative instruments like forward and future contracts going out several years, and has now started trade in options. Outside this mar- ket, there is quite a large and liquid market for over the counter forward and option contracts. The objective of

IJSER © 2011 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 2, Issue 4, April-2011 4

ISSN 2229-5518

financial market is to provide an efficient market, with excellent liquidity and a high level of security to offer a number of financial power contracts that can be used profitably by a variety of customer groups. This market is wholly owned by Nord Pool Group.

(iii) Nord Pool Clearing ASA :

It is a licensed and regulated clearing-house. It is cen- tral counter party for all derivative contracts traded through exchange and OTC. It guarantees settlement for trade and anonymity for participants. It is wholly owned subsidiary of Nord Pool Group.

(iv) Nord Pool Consulting AS :

It is a consulting firm specializing in development of power market worldwide. It is also a wholly owned sub- sidiary of Nord Pool Group.

(v) Nordel:

Nordel is an association for electricity cooperation between forum for market participants, nordic system operators and TSOs of nordic countries. The primary ob- jectives of organization are to create and maintain the necessary conditions for an effective nordic electricity market.

Nord pool is first multinational commodity exchange for Electric sector in the world .It provide open market to all Nordic Countries with common framework.-Nordic and Europian markets are example of decentralized day ahead spot market.There are no general cross border tariff among Nordic Countries.Trading of electricity generated by hydropower dominates the cross-border exchanges between the Nordic countries. The balance of electricity trade between the four countries depends on rainfall con- ditions because of great variation in fuel type capacity of Nordic countries. If hydropower potential is good, Swe- den and Norway record trade surpluses, if hydro re- source is poor Denmark and Finland will benefit from the electricity trading.-There are only one Market Operator (MO)-Nord Pool and five System Operator (SO) which are Svenska Kraftnät in Sweden, Fingrid in Finland, Stat- nett in Norway, Eltra in western Denmark, and Elkraft System in eastern Denmark[9].There are separate regula- tory agencies in the four countries. The MO is in principle only responsible for facilitating the trade of electricity as the commodity, but within the physical constraints set by the SO. The operation of the physical system is the sole responsibility of the SO. Further, the market participants

are given the freedom and responsibility of controlling (scheduling) their resources, and have to optimize the utilization of their physical and contractual as- sets.Transmission system operations are organized on a national basis for Nordic countries.The Five TSOs in the Nordic area are owner of respective main national grid The National Transmission System Operators (TSOs) are responsible for reliability and balance settlements.

The Elspot market is formed as a day-ahead physical- delivery power market and the deadline for submitting bids for the following day’s delivery hours is fixed as 12 am (noon). There are three types of bids available in Els- pot; the hourly bid or single bid, block bid and flexible hourly bid.Participants can submit bids to Nord Pool Spot electronically either through EDIEL communication or through the internet application ElwWeb.Nord Pool of- fers futures contracts for one to nine days ahead and for one to six weeks ahead in time. These futures contracts are settled daily. All these futures and forward contracts use the daily average system price as reference. There are also contracts to hedge zonal price differences, either one quarter or one year ahead.Prices for real-time are deter- mined by the marginal bid like in the day-ahead spot market.Real time market is also known as Regulated Power Market in Norway.Nord Pool PX has a market share of 43% of the physical Nordic demand; the remain- ing 57% is traded bi-laterally.Nord Pool also operates a trading platform for financial derivatives as well as clear- ing house for bi-lateral contracts.

Congestion Management is done by market splitting i.e. resolving congestion in day ahead market and counter trade i.e. resolving congestion in real time.Point of Con- nection tariff structure is followed to promote space.UI pricing mechanism is followed for deviation from sche- dule.Dr. Per Christer,Senior Vice President ,Nord Pool Consultancy has given the Nord Pool Market Model (shown in fig3.).

Figure 3.Nord Pool Model as given by Dr. Per Christer

The Pennsylvania – New Jersey – Maryland in-

IJSER © 2011 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 2, Issue 4, April-2011 5

ISSN 2229-5518

terconnection (PJM) has been a pool between the three founding utilities that enables co-ordination of trade since 1927. PJM is responsible for the manage- ment of a competitive wholesale electricity market across the control areas of its members and for safe and reliable operation of the unified transmission sys- tem. All generators defined as a capacity resource in PJM system are obliged to submit an offer into the day-ahead PJM market. Market participants are al- lowed to self schedule. Transmission system security and reliability considerations are taken into account for the total market clearing operation. A marginal pricing principle is used for market clearing. Each generator at its specific node is paid market clearing price . All loads at their specific nodes are charged as per the market-clearing price . PJM Interconnection is a non-profit company ,a limited liability, governed by a board of managers. There is a specific unit ‘Market Monitoring Unit (MMU)’ within PJM to oversee the functioning of the market. States have public utility commissions (PUCs) and the Federal Energy Regula- tory Commission (FERC)(shown in fig4). PUCs regu- late generation and distribution’s intra-state utility business. The FERC regulates interstate energy trans- actions including wholesale power transactions on transmission lines[10].

Public, Political pressure and higher electricity cost have resulted in ending the regulated monopolies of vertically integrated utilities. Deregulation in US pro- ceeded with the Public Utility Regulating Policies Act approval in 1978 and the Energy Policy Act (EPAct) in 1992.Federal Energy Regulatory Commis- sion(FERC) approved non-discriminatory open access to transmission services in 1995.Utilities and Regulators, including American Electric Power (AEP)

, the California Public Utilities Commission (CPUC),the New England Electric System (NEES) and the Pennsylvania/New Jersey/Maryland(PJM) pool have formulated several proposal for change[11].

Figure 4. PJM Model

The Comprehensive National Energy Strategy an- nounced on April 1998 and stressed that it relies as much as possible on free markets and competition. An Independent System Operator (ISO) and Power Exchange (PX) have been established in 1998 based on market structure after the CPUC’s decision in 1995 which became watershed for the road towards com- petitive market. The outlining of the proposed Cali- fornia Model filed with FERC on April 29, 1996 with- three investor owned utilities (IOUs) in California which were Pacific Gas & Electric or PG&E, Southern California Edison and San Diego Gas Electric. There are three significant characteristic in California Mod- el-

a) To simplify the transmission pricing scheme in-

cluding nodal and congestion charge assessing, Zonal

Approach is applied.

b) A Scheduling coordinator (SC) or PX have been introduced to manage multiple separate energy for- ward markets (each with a supply and demand port- folio). An adjustment approach is adopted to perform inter-zonal congestion management.

c) An adjustment bid approach is adopted to per-

form inter-zonal congestion management.

An Independent System Operator (ISO) and a Power Exchange (PX) have been established in 1998 based on market structure and rules governed by FERC.Multiple separate energy forward markets, each with a supply and demand portfolio managed by a Scheduling Coordinator (SC) or PX have been introduced .The total separation of the wholesale power exchange and the market participant was done from ISO.

Power Exchange will be independent entitiy for

managing bid of energy for each half-hour on a day ahead basis for ISO dispatch decision. The ISO will control the power dispatch and the transmission sys- tem [12]. It will have no financial interest in the Pow- er Exchange or in any generation, load, and transmission or in distribution facilities. The

ISO will coordinate the information exchange

in an open market and willwork as per North American Reliability Council (NERC) and Western System Coordinating Council (WSSC) reliability standards. The ISO will coordinate day-ahead scheduling and balancing for all us- ers of the transmission grid and also will pro- cure ancillary services.

International Journal of Scientific & Engineering Research Volume 2, Issue 4, April-2011 6

ISSN 2229-5518

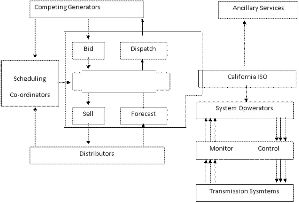

Scheduling Coordinators (SCs) aggregate partici- pants in the energy trade and are free to use protocols that may differ from pool rules. SCs run a forward market in which parties can bid to buy and sell ener- gy and submit the preferred schedule to the ISO and work with the latter to adjust schedules when neces- sary(figure 5).

California PX

Figure 5.California structure with inclusion of Scheduling

Coordinators.

The New Zealand electricity system consists of Nort and South Island as two alternative current (AC system connected by 1200 MW underwater HVDC cable.All capacity on South Island is hydroelectric and it exported power to North Isl- and.Approximately 75% of the North Island demand is met from hydroelectric source with the remaining

25% split between geothermal sources and fossil fuel

(coal, gas and oil) sources. Prior to February 1,1996

,the generating industry was dominated by state- owned Electricity corporation of New Zeal- and(ECNZ) which owned and operated 95% of total capacity.A wholesale market as Contact Energy ltd. for electricity was formed as seperate state owned enterprise from ECNZ On February 1,1996. There are currently 38 electricity distribution compa- nies,providing equal access distribution services and electricity supply to customers and one electricity retailer providing electricity supply only[13].The wholesale electricity market in New Zealand com- menced operation under the name Electricity Market Company(EMCO) on October 1,1996.

The New Zealand Electricity Market(NZEM) intro-

duces competition within the wholesale electricity sector through creation of a national electricity pool

and a spot market for electricity.The EMCO operates the market througha bidding system and is the clear- ing –house for market transactions.TransPower , the operator and developer of the national grid ,performs the various services like provision of reliable national grid ,efficient scheduling and dispatch generation to satisfy market demand,purchasing of ancillary ser- vices and providing information to the grid users in an open ,non-discriminatory manner in the whole- sale electricity market.

The restructuring in the Alberta’s electric industry was started to retain benefits of the existing low cost generators for customers in 1996.In the new structure

,power pool was defined for all energy- trade in the province.Generation sector made fully competitive with competitive bidding except the case of old re- tired power plants.IPP was brought to meet load growth. Grid Company of Alberta,(GridCo) adminis- tered a province –wide transmission grid.The trans- mission grid was owned by the four utilities that own transmission facilities in the province and contract all individual owners to supply transmission servic- es.The Electric Transmission Council as advisory group formed to represent the interests of consumers and transmission users[14].

UK government took a historic step by privatizing the publicly owned electric power industry in Eng- land and Wales (E&W) in 1988.Generation, Transmis- sion and Distribution of electricity were divided into three large companies. All existing fossil fuel plants were taken over by National Power and powerGen .

The National Grid Company (NGC) provides

transmission services from generators to the Regional Electricity Supply Companies (RECs) and coordinates transmission and dispatch of electricity generators [15].NGC runs both the physical and financial side of the E& W electricity market. It serves as both the In- dependent system operator (ISO) and the Power Ex- change and determine both half-hourly market clear- ing prices and runs the physical national grid, mak- ing generator dispatch decisions in real time to man- age congestion on the grid and provide ancillary ser- vices for reliable supply to all the consumers [16]. NGC uses GOAL (generation ordering and loading)

IJSER © 2011 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 2, Issue 4, April-2011 7

ISSN 2229-5518

program to determine the merit order of dispatching generation alongwith reserve capacity[17].

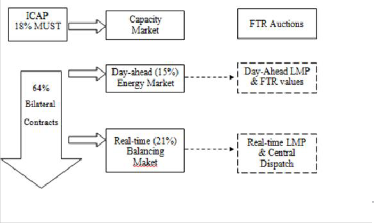

Indian Power sector is in a transition phase from a regulated sector to a competitive market (taken as author is from India). A competitive market provides the participants with benefits of psrice determination

demand of SEB through respective RLDCs at regional level. But it is mandatory cost based (non bid) Power Pool.ABT mechanism facilitates Balancing market in an inherent way but it has got some limitations al- so.Current trading occur between ISGS and states STU/SEBS,

State

by market forces ,easy access to market, transparent

working however it also brings with it many changes that need to be taken care of by the market partici- pants at various stages of development.

The power sector in India has seen significant de- velopments post the enactment of the Electricity Act

2003[18]. The policy and regulatory efforts have also been synchronized to ensure rapid development of the power markets in the country.

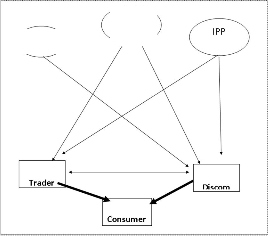

In this direction, Electricity Act 2003 has come into

force from June 2003 in India. It introduces the con- cept of trading bulk electricity. The Act has enabled

consumers and the distribution companies to have

CGS

Genco

choice in the selection of electricity supplies . Similar- ly, the generator also has choice to select among the distribution companies (shown in figure 6.). The Act specifies the provisions for non-discriminatory use of transmission lines or distribution system or asso- ciated facilities with such lines or system by any li- censee or consumer or a person engaged in genera- tion.

At regional level, there are five regional load dis- patch centers( NR,WR,ER,SR,NER) which are operat- ed by Power Grid..At state level, there are 28 states which are responsible for their generation, transmis- sion and distribution. States purchase power from Independent State Generation Supply (ISGS).Trade between states is facilitated by trading firms like PTC,NVVL and others[19].Distribution licenses and Government do not need trading license and trans- mission licenses and load dispatch centers can not trade power.About 2.5 % of total power generated in country is being traded presently.There are 17 li- censed electricity traders for inter state trading till now.Most generation capacity (56% State,36%CGS,11%Private) tied up with long term contracts. Only surplus can be traded.The present inter-regional capacity is 11500MW which is planned to go upto 37000 MW upto 2012.India have Pool type centralized mechanism for dispatching central gene- rating plants. On day ahead basis to meet forecast

Figure 6.Indian Market Structure after Act-2003

between states, through international import

/export (Bhutan, Nepal) and also by state embedded generators/IPPs / Loads and others.The RLDCS or- ganize the day ahead scheduling of the ISGS[20]

.Short term bilateral contracts are taking place through traders but they are lacking formal market and real time information. Often Sellers call for sepa- rate tenders for surplus available with them and trad- ers compete with each others on prices to get the supply. This situation has resulted in prices of traded power moving only in one direction (higher). The root cause is one-sided competition. On the other hand, buyers are not getting adequate response against tenders called by them. A platform for wide sellers and buyers is not available.

In the various countries, most of the electric power industry has been going through a process of transi- tion and restructuring by moving away from vertical- ly integrated monopolies and towards more competi- tive market models since nineties. This has been achieved through as creating competition at each lev- el in the power industry and having a clear separa- tion between its generation, transmission and distri- bution activities as well. Different countries are im-

IJSER © 2011 http://www.ijser.org

International Journal of Scientific & Engineering Research Volume 2, Issue 4, April-2011 8

ISSN 2229-5518

plementing industry restructuring in a variety of ways, depending on the characteristics of each mar- ket area which include: diversity of generation by fuel types, demand/supply balances, the extent of transmission capacity to facilitate energy imports to meet market demand and etc.. In designing and planning the market structure and rules for competi- tion in their jurisdiction, governments, regulators and other industry participants are influenced by local market characteristics and the practices.

[1] M,Illic, F. Galiana and L. Fink, “Power System Restructur- ing:Engineering and Economics”,Kluwer Academy Publisher,1998.

[2] http://class.ece.iastate.edu.

[3] A.K.Izaguirre, Private participation in the electricity sector- recent trends”,World Bank report-Private Sector, December

1998,pp.5-12.

[4] H. Rudnick , “Chile: Pioneer in deregulation of the electric power sector”,IEEEE Power Engineering Review ,June 1994,pp.

28-30.

[5] M.I.Dussan ,”Restructuring the electric power sector in Colom- bia”,IEEE Power Engineering Review,June 1994,pp21-22.

[6] C.M. Bastos,” Electric energy sector in Argentina”,IEEE Power

Engineering Review June 1994 ,pp.13-14.

[7] H. Outhred, “A review of electricity industry restructuring in

Australia”,Electric Power Systems Research,vol.44,1998,pp.15-

25.

[8] R.D.Christie and I. Wangesteen,”The energy market in Norway and sweden:Introduction”,IEEE Power Engineering Re- view,February 1998,pp.44-45.

[9] http://www.nordpool.com.

[10] PJM Interconnection LLC,”PJM Open Access Transmission

Tariff: Schedule-2”, Fourth Revised, Vol1, Issued February

2001.

[11] Z.Alaywan and J.Alen,”California electric restructuring ;a broad description of the development of the California ISO”,IEEE Trans on Power Systems ,Vol.13,No.4,November

1998,pp.1445-1451.

[12] http://www.caiso.com.

[13] T.Alvey,D.Goodwin,X. Ma, D. Streiffert and D Sun,”A security –

constrained bid-clearing system for the New Zealand wholesale elec- tricity market”,IEEE Trans on Power Sys- tems,Vol.13,No.2,May1998,pp.340-346.

[14] J.R. Frey,”Restructuring the electric power industry in Alberta

“,IEEE Power Engineering Review ,February 1996,pp.8.

[15] National Grid Electricity Transmission (NGET) plc, “The connection and use of system code (CUSC),” Issued Feb.2006.

[16] http://www.nationalgrid.com/uk. [17] http://www.iitk.ac.in.ime/anoops. [18] http://www.cerc.org.

[19] http://www.ee.iitb.ac.in/wiki/faculty/sak. [20] http://www.jbic.go.jp/en/research/report.

IJSER © 2011 http://www.ijser.org