International Journal of Scientific & Engineering Research, Volume 5, Issue 1, January-2014 177

ISSN 2229-5518

Determinants of Customers’ Acceptance of Electronic Payment System in Indian Banking Sector – A Study

Sanghita Roy, Dr. Indrajit Sinha

Abstract - Internet is perhaps one of the most important tools to businesses and individuals in the recent world economy. Globalization, financial liberalization and technology revolution have opened the door of new and more efficient delivery and processing channels as well as more innovative product and services in banking industry. With increased educational qualification and growing wealth consumers’ need and expectations are continually changing and they are involving themselves more and more in their financial decisions. After deregulation and reforms in Indian Banking scenario payment systems like Debit Card, Credit Card, ECS, EFT, RTGS, NEFT have offered variety of services to the customers. Despite the growth of electronic payment system over physical check-based system, its rate of adoption in India especially in Metro cities like Kolkata has been relatively slow. Its slow adoption rates raise many questions.. The aim of the study is to determine the factors influencing consumer’s adoption on the light of Technology Acceptance Model. Survey based questionnaires are designed and Factor Analysis is used to find reliable and consistent factors. Proposed model illustrates the level of fulfillment of each acceptance factors and therefore predicts its adoption and indicates areas of improvement.

Index Terms – Customers’ attitude, Internet connectivity, Perceived usefulness, Perceived ease of use, Perceived risk, Perceived credibility, Technology Acceptance Model (TAM)

1. INTRODUCTION

adopted various E-banking techniques to strengthen their

IJSEfinancial posiRtion. According to the report of RBI, during

The worldwide proliferation of Internet has given birth of

Electronic payment system which is “the use of debit and credit cards on the Internet or other electronic devices to perform daily transactions which include paying for goods and services, transfer of money and bill payments at any time of the day”, stated Gholami et. al. (2010) with Andam(2003, [1]). Electronic payment offers the benefit of acquiring and using goods and services without paying for them with cash, thus removing the burden of carrying cash (Fosent et. al. 2010, [3]). Electronic payment the term was first used by IBM’s marketing and Internet team in

1996(Amor, 1999, [4]). By Electronic payment systems refer

to various innovative applications and approaches including the use of credit card, debit card, Automated Teller Machine(ATM), Electronic Fund Transfer(EFT), online payment that are used to facilitate customer’s decision to pay for a product or services (Vassilious,2004, [2]). Research indicated that use of electronic payment are largely influenced by demographic characteristics of users such as gender, age, education level, income, marital status, culture and attitude towards debt ((Abdul-Muhmin and Umar, 2007; Wickramasinghe & Gurugamage, 2009, [7]).

After globalization, financial liberalization and economic reform during the last two decade Indian banks have

the last two decade all the electronic mode of payment have shown better growth than the physical check based system [5]. Manoharan (2007,[8]) highlighted the impact of Electronic payment system on Indian Banking sector. Payment system in India has been divided into three parts, i.e., large value payment system, retail payment system, and retail electronic system.

In the country like India where 90% of its population rely on conventional payment system i.e. physical cash and check rather than electronic payment, it is not so simple to consider and decide on the basis of cost and benefit of using E-payment system [5]. Majority of people are still reluctant to deal with Electronic payment because of security and privacy concern [8]. In the course of preparing this research paper, we had the privilege of visiting few remote places of south bengal to find out the perceptions of people about electronic payment system. It was observed that most of the people have not a common knowledge about Internet- its operation and usage. About Electronic payment, they hardly know operation of ATM. People are quite far from all the ICT developments taking place in banking. Even in metro cities 60% people rely on traditional payment instruments. Even for large value payments, like sale and

IJSER © 2014 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 5, Issue 1, January-2014 178

ISSN 2229-5518

purchase of land and building, people prefer physical cash

rather than receiving any other form of payment.

2. LITERATURE REVIEW

The paradigm shift from manual to technology enabled banking delivery channel was first introduced in Finland in

1996. As per the latest result 84 percent of Finns use

Internet today, among them 64 percent are user of internet banking [13]. More than 50 million of the US adult population is banking online according to a new survey by the Pew Internet and American Life Project Evolving Technology Trends in Indian Banking Sector 33. In US the biggest transformation occurred between 2003 to 2006 [6]. Survey on internet banking in U. K. by Forrester Research during 2007 showed that about 31 percent of British adults use online payment system. This is despite the fact that about two thirds (67%) of the British are regular users of the internet [7]. Ahmad Bello (2005) investigated the impact of

e-banking especially “how e-payments are satisfying the

investigate the acceptance of E-banking in Nigeria. The

result shows that acceptance of is significantly influenced by Age, Educational Background, Income, Perceived Benefits, Perceived Ease of Use, Perceived Risk and Perceived Enjoyment [15].

2.1 TAM and related studies

Here we will investigate the factors determining the acceptance of Electronic payment customers in the light of Technology Acceptance Model (TAM) (Davis, 1989) and Roger’s Diffusion of Innovation (DOI) theory (Rogers, 1983, [30]) . Using Technology Acceptance Model Pikkareinan et. al. (2004, [30]) opined that Perceived Usefulness (PU) and Perceived Ease of Use (PEOU) among other factors significantly affect the acceptance of E-payment. Other factors being: Perceived Risk, Trust, Security and privacy etc. Using the DOI theory, Lee and Lee (2000, [17]) investigated the factors influencing the adoption of various

Electronic-payment technologies. Tan &Teo (2000, [30])

IJSER

customers” in Nigeria [9] . Andoh-Baidoo and Osatuyi

(2009) in their study illustrated that Nigerian banks are not taking advantage of the full spectrum of e-payment features because of some challenges especially inadequate power supply and telecommunication [10]. Baten and Kamil (2010) determined the economic prospects of e- banking as well as demonstrating the scope and benefits of e-payments in Bangladesh [9]. Salehi and Alipour (2010) examined e-banking and e-payments in an emerging economy seeking to provide empirical evidence from Iran[12] . As per the report of consulting firm Celent, India, indicates that, the value of retail E-payments in India has reached US $150 billion to US $180 billion by the end of

2010 [11].

In the works of Taylor and Todd (1995) and Gefen and Straub (1997), it was found that gender has a direct influence on adoption of technology with men and women having different rates of computer technologies adoption [12] .Gikandi and Bloor (2009) used time series data to investigate the determinants of adoption and influence of e- commerce involving 90% of the retail banks in Kenya.Olatokun and Igbindion (2009) used diffusion of innovation (DOI) theory to investigate the adoption of Automatic Teller Machines in Nigeria [17]. James (2012)

used Statistical Package for Social Sciences (SPSS) to

discovered that adopted four attitudinal constructs of the

DOI theory: relative advantage, compatibility, complexity and trialability, as part of their research model. They found that relative advantage, compatibility, and trialability significantly affected the intention to use Internet banking, whereas complexity was not significant. TAM is based on the theory of reasoned action(TRA) (Fishbein and Ajzen,

1975; Ajzen and Fishbein, 1980, [7]).

Perceived Usefulness (PU) is defined as the degree to which a person believes that using a particular system would enhance his or her job performance.

Perceived Ease Of Use (PEOU) is defined as the extent to which a person believes that using a particular system will be free from effort.

Perceived Risk, Trust, Security and Privacy

Perceived Risk is very much close to Perceived Security and privacy. Still people have fear in doing E-payment transaction, as they are concerned with security and privacy aspects of such system. It is noted that although consumer’s confidence in their bank was strong, yet their confidence in the technology was weak.

IJSER © 2014 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 5, Issue 1, January-2014 179

ISSN 2229-5518

Perceived Credibility is defined as the extent that a user

using the system should carry out a transaction securely and maintain the privacy of personal information against unauthorized access. According to Hanudin (2007), perceived credibility is a determinant of behavioral intention to use an information system.

Customer attitude

Attitudes as defined Davis (1989) and Karjaluoto et al., (2002) are the users’ desirability to use the system. It reveals the perceptions of usefulness, credibility and individual preferences (Jahangir et al., 2007). Consumer’s attitude is argued to have a strong, direct and positive effect on consumers’ intention to actually use new information system (Jahangir, et al., 2007).

3. OBJECTIVES & HYPOTHESIS

The main objectives of this study are to:

H5: Customer attitude has a positive effect on consumer acceptance of Electronic Payment

4. METHODOLOGY

The study was based on primary data. The tools constructed for the collection of data were Interview Schedule using structured questionnaires. Data for this study were collected by means of a survey conducted mainly in metro city Kolkata, West Bengal and its surrounding suburb area from August to October 2013. The structured survey questionnaires were in English and those were distributed to randomly select 650 participants. Participants were mainly from Education sector. Others were from Banking, Government services, IT professionals, students, retired persons or even housewives. The respondents were asked beforehand whether they had

knowledge about online banking and Electronic Payment

IJSER

(a) Finding of most influencing factors among the

factors that influence the customers’ adoption of electronic payment services in India

(b) Finding the most popular electronic payment

system among various electronic payment options. (c) Study the level of awareness and usage of E- payment techniques among different age group, different income group with their educational level

by demographic analysis

(d) Finding the reasons of unpopularity or constraints and providing suggestions for further improvements for E-Payment acceptance.

To achieve the above objectives, following hypotheses have been framed:

H1: Perceived Usefulness has a positive effect on consumer acceptance of Electronic Payment

H2: Perceived Ease of Use has a positive effect on consumer acceptance of Electronic Payment

H3: Perceived Risk has a negative effect on consumer adoption of Electronic Payment, higher the risk lower rate of Electronic payment adoption

H4: Perceived credibility has a positive effect on consumer acceptance of Electronic Payment

services. Only those who answered in affirmative were given the questions to complete in presence of the researcher. The questionnaire consist of two sections. Section A was designed to collect demographic informations like age, gender, occupation, educational qualification and section B was designed to generate information relating to the experience of the customer while using Electronic payment services. 235 responses were received and after checking the validity of the questions 167 respondents were fit for carrying out descriptive analysis. Data thus collected were posted in a master table to facilitate further processing. Statistical analysis of the data were done through SPSS 16 software in computer. In the analysis 5 point Likert scale was used. Scores were allotted for the usage such as totally agree -1, agree-2, neutral-3, disagree-4 and totally disagree-5.

The questions were initially tested with a focus group of 30 respondents mainly professionals from Education sector in West Bengal. The focus group was quite helpful and confirmed that the formulated hypotheses were likely to be highly relevant in explaining perceived adoption of E- payment services in India. On the basis of the pilot study, interview schedule and questions were redesigned with suitable modifications.

IJSER © 2014 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 5, Issue 1, January-2014 180

ISSN 2229-5518

Two types of variables available in the research - dependent

variables and independent variables. The goal of this research was to understand and describe the dependent variables to know the consumers’ intention to use E- payment system. Independent variables significantly influenced the dependent variables in either positive or negative ways. In this study the independent variables were Perceived Usefulness, Perceived Ease of Use and Perceived Risk. These three independent variables would be tested to identify whether or not these variables possess influence on the dependent variable.

5. ANALYSIS & FINDINGS

5.1 Demographic analysis

The response rate is 36.15 percent (235). Among these, 167 (71.06 percent) of the responses are usable as most items are adequately responded. A total of 70.06% are male

respondents. A majority of the respondent (45.78%) is in the

50,000 (40.96 %), though while doing this survey 34.93%

people had not disclosed about their income.

Survey report shows that E-payment system is accepted only by the urban people (82.03%), while rural and sub- urban people hardly know about it. Majority of them are rare users of ATM card only. From this survey one thing is clear that people still have faith on public bank (74.25%) and State Bank of India lies top of this list. SBI have 35.92% online users, followed by United Bank of India- 10.17 percent online users. All the private bank users are urban people. Majority of them are customers of HDFC bank (9.58

% online users), followed by Axis bank (5.98 % online

users), ICICI bank (4.19 % online users) respectively. Those who are users of online all of them primarily perform ATM transaction. Next comes use of Debit card, credit card and rest. According to the survey report VISA has largest customer base than Master. Detailed information is depicted in Table I (given after references)

range of 26 to 40 years of age. Next falls the age group of 18 to 25 years, they are keen to adopt the latest technology.

People with age of above 40 or above 60 years basically prefer conventional method (8.0 percent) i.e. cash and check. Most of them are aware of latest technology but as they are not tech-savy they are afraid of doing so.

In consideration with marital status 48.73 percent respondents are married while 47.46% respondents are single. As both the percentage are all most same, marital status is not a significant factor in Electronic-payment adoption. The survey shows that users of E-payment system are mostly highly educated people- master degree holder (38.32 percent) and next the graduate people (28.143

%). More than three-quarters (66.46%) of the respondents

perform online transactions and have previous experience in surfing internet. Only minority 26.34 percent is techno- phobic and might simply be reluctant to change. During survey most of the participants came from education sector. So majority users 56.88 percent are from this sector, 20.58% respondents are in IT & Telecom, 17.38% in Govt. service,

23.7% people are involved in business and only 14.22% are house-wives. Tremendous responses came from students, almost 80% of them are users of electronic payment system. Majority have a moderate income level, which is below Rs.

5.2 Measurement Model

Reliability Test

A reliability analysis is carried out to check for the underlying dimension of the success factors generated through factor analysis. A rare of thumb suggests that the reliability measures of each of the constructs were found to be above the 0.70 cut off (Cronbach, 1970). Table II depicts a summary of the Alpha scores of all the response ranking of the factors that affect the adoption of E-payment system. All factors exhibit a Cronbach’s alpha co-efficient of at least

0.72, indicating that the questionnaire (n=167) has attained

rather high level of reliability. Hence, all variables are retained. Among the factors, Perceived Risk (PR) has the highest ranking of Cronbach alpha of 0.78, followed by customers attitude (CUAT) 0.77. Perceived Ease of Use (PEOU) has the lowest ranking with 0.72. Table II (given after references)

Next step was to ensure construct confirmatory validity. Confirmatory construct validity was evaluated using factor

analysis to detect high loadings on the hypothesized factors

IJSER © 2014 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 5, Issue 1, January-2014 181

ISSN 2229-5518

and low cross-loadings. All eigen values associated with

hypothesized factors were set to greater than unity. Principal component analysis was used for extraction method for factor analysis with Varimax rotation. In summary, model and hypotheses tests were conducted with five independent variables – Perceived Ease of Use (PEOU), Perceived Usefulness(PU), Perceived Credibility (PC),Perceived Risk (PR) and Customer Attitude (CUAT) and one dependent variable – use intentions (USE). The Descriptive statistics of these variables are presented in

Table III (given after references)

119.312, P = 0.000), we tested the significance of each

variable. Perceived ease of use, Perceived Credibility,

ceived Risk, Customer attitude significant. Table VI (given after references) illustrates which hypotheses are supported.

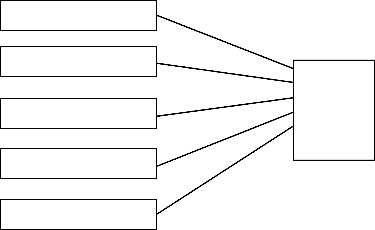

Perceived Ease of Use

0.184

MODEL TESTING

Perceived Usefulness

Perceived Risk

0.090

0.141

Electronic

Payment

Adoption

To test the model and the hypotheses, Multiple regression analysis was used. It is constructive statistical technique that can be used to analyse the associations between a set of independent variables and using a single dependent

Perceived Credibility

0.081

0.062

variables.

IJSECustomer AtRtitude

Method : Stepwise analysis(criterion: Probability of F to

enter <=0.05). Table IV (given after references)

a. Predictors: (Constant), PEOU

b. Predictors: (Constant), PEOU, PU

c. Predictors: (Constant), PEOU, PU,PC

d. Predictors: (Constant), PEOU, PU,PC, PR

e. Predictors: (Constant), PEOU, PU,PC, PR, CUAT

f. Dependent Variable: USE

Key elements of analysis: Five models were tested and fifth model indictes it has five predictors besides constant to determine the dependent variable that met entry requirement in the final quation(PEOU, PU,PC, PR, CUAT). The multiple R ( R = 0.831) shows a substantial correlation between five predictor variables and the dependent variable. Table V (given after references)

RESULTS

The model explains 69.0% of the variance in intention to use e-payment. Because the overall model is significant (F =

6. CONCLUSION & IMPLICATION

This paper presented an empirical review of Electronic payment acceptance in Kolkata. The model formulated evaluated Perceived Ease of Use (PEOU), Perceived Usefulness(PU), Perceived Credibility (PC),Perceived Risk (PR) and Customer Attitude (CUAT) to continue using E- payment acceptance. Among the factors Perceived Ease of Use (PEOU) is found to be the most significant predictor. Conversely, customer attitude was found to have least significant affect on adoption of E-payment. From the finding it is clear that customer have to use more and more this online payment system. More we use the new technology more it will be friendlier with us.

E-payment system in India, has shown tremendous growth, but still there has lot to be done to increase its usage. Still

90% of the transactions are cash based. So, there is a need to widen the scope of electronic payment. Innovation, incentive, customer convenience and legal framework are the four factors which contribute to strengthen the E- payment system.

IJSER © 2014 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 5, Issue 1, January-2014 182

ISSN 2229-5518

7. LIMITATION & SUGGESTIONS

This study was conducted in Kolkata and its surroundings. Study from other part of the country may reveal a different result due to demographic and economic differences. Also the sample was restricted basically to city where level of literacy is relatively higher. Another limitation is majority of the respondents are from education sector and also sample size is relatively small. Moreover, the study excludes the voice of non-users. Banks may adopt following strategies in order to make E-payment popular.

• Banks should ensure that online transaction is safe and secure like traditional transaction

• Banks should organize free seminars and

conferences specially in rural areas to educate less qualified people regarding uses of ATM, Debit

card, Credit card etc. and also explain them about

[3] Asaolu, O.,T.,Ayoola, J.,T., and Yemi, E., (May 2011)

“ELECTRONIC PAYMENT SYSTEM IN NIGERIA: IMPLEMENTATION, CONSTRAINTS AND SOLUTIONS”, Journal of Management and Society, Vol. 1, No

2, pp. 16-21

[4] P. W-Ching, (2008), “User’s adoption of e-banking services: the Malaysion perspective”, Journal of Business and Industrial Marketing, Vol. 23, No. 1, pp. 59-69

[5] Singh, M. and Kaushal, R.,(2012) “Factor Analysis Approach to Customers’ Assessment of Electronic Payment and Clearing System in Indian Banking Sector”, Journal of Information Technology, Icfai University Press

[6] Ifinedo, P “Facilitating the Intention to Expand E- business Payment Systems Use in Nigerian Small Firms: An Empirical Analysis”, retrieved from www.intechopen.com

[7] Crede, A (1998) Electronic payment System, Electronic

IJSER

security and privacy of their account.

• Some customers mainly older people are hindered by lack of computer knowledge. They need to be educated on basic skills required to conduct online transaction.

• Banks must emphasize the convenience that

electronic payment can provide many benefits to people, such as avoiding long queue, in order to motivate them to use it.

Future research in examining level of acceptance of electronic payment should overcome these limitations and should include views of non-users, marketing strategy, promotional and communication issues to acquire new users and effectively maintain the existing customers.

REFERENCES

[1] K.Geetha and V. Malarvizhi, (2012), “Assessment of a Modified Technology Acceptence Model among E-Banking Customers in Coimbatore City”, International Journal of Innovation, Managemnet and Technology, Vol. 3, No. 2

[2] Themba, G and Tumedi, B., C. (2012) “Credit Card Ownership and Usage Behaviour in Botswana”, International Journal of Business Administration, Vol. 3, No. 6.

money and the Internet: The United Kingdom Experience

to Date retrieved from www.susx.ac.uk/spru.

[8] Manoharan B (2007), “Indian e-Payment System and Its

Performance”, Professional Banker,Vol. 7, No. 3, pp. 61-69.

[9] Mantel B (2000), “Why Don’t Customers Use e-Banking Products: Towards a Theory of Obstacles, Incentives and Opportunities”, FRB Chicago Working Paper No. EPS-2000-

1.

[10] Nargundkar R (2002), Marketing Research, Tata

McGraw-Hill, New Delhi.

[11] Ramani D (2007), “The E-Payment System”, E-Business, Vol. 7, No. 5, pp. 35-41.

[12] Talwar S P (1999), “IT and Banking Sector”, RBI Bulletin, Vol. 53, No. 8, pp. 985-992.

[13] Wenninger J (2000),“Emerging Role of Banks in e- Commerce”, in Current Issues in Economics and Finance, Vol.

6, No. 3, Federal Reserve Bank of New York.

[14] Abrazhevich, D (2002) “Classification and Characteristics of Electronic Payment Systems” retrieved from www.citeserr.nj.ntc.com

[15] Anik, A.A. & Pathan, A.K. ( 2002) A framework for managing cost effective and easy electronic payment

IJSER © 2014 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 5, Issue 1, January-2014 183

ISSN 2229-5518

system in the developing countries. Retrieved from www.commonwealth.com.

[16] Ayo, C. K, Adewoye J.O, and Oni A.A, (2010),” The State of e-banking Implementation in Nigeria: A Post- Consolidation Review”, Journal of Emerging Trends in Economics and Management Sciences, Vol. 1, No. 1, pp. 37-

45

[17] Leong, A. (1998) Paper, Plastic and now, Electronic: A Survey of Electronic Payment System, retrieved from. www.euromoney.com

[18] Sadeghi, A & Schneider, M (2001) Electronic Paymenrt

SystemElectronic Payment Systems.

[19] Alhudaithy, A.I. and Kitchen, P.J., (2009) “Rethinking models of technology adoption for Internet banking: The role of website features”, Journal of Financial Services Marketing, Vol. 14, No. 1, pp56–69.

[20] Lee, H.H., Fiore, A.M. and Kim, J., (2006) “The role of

[24] Adeoti, O.,O., Osotimehin, O.,K. and Olajide, (2012) “Consumer Payment Pattern and Motivational Factors using Debit Card in Nigeria”, International Business Management, Vol. 6,No.-3, pg-352-355

[25] Gapar, Md., Johar, Md. And Awalluddin, A.,A.,J, (August 2011) “THE ROLE OF TECHNOLOGY ACCEPTANCE MODEL IN EXPLAINING EFFECT ON E- COMMERCE APPLICATION SYSTEM”, International Journal of Managing Information Technology (IJMIT) Vol.3, No.3

[26] Sudhagar, S., (2012) “A Study on Perception and Awareness on Credit Cards among Bank Customers in Krishnagiri District”, IOSR Journal of Business and Management (IOSRJBM) ISSN: 2278-487X, Volume 2, Issue 3 (July-Aug. 2012), PP 14-23

[27] Mahil, R., V. and Vidya Sagar, N, (2007) “PROFILING OF INTERNET BANKING USERS IN INDIA USING INTELLIGENT TECHNIQUES” Journal of Services Research,

IJSER

the technology acceptance model in explaining effects of

image interactivity technology on consumer responses”

International Journal of Retail & Distribution Management, Vol.

34, No. 8, pp 621-644.

[21] Sekaran, U. and Bougie, R., (2010) “Theoretical framework In theoretical framework and hypothesis development”. Research Methods for Business: A Skill Building Approach, United Kingdom: Wiley, pp. 80

[22] So, W.C.M., Wong, T.N.D and Sculli, D., (2005) “Factors affecting intentions to purchase via the internet”, Journal of Industrial Management & Data Systems, Vol. 105, No. 9, pp1225-1244.

[23] Sanzogni, L., Sandhu, K and Ghaith, A.,W.,(2010) “FACTORS INFLUENCING THE ADOPTION AND USAGE OF ONLINE SERVICES IN SAUDI ARABIA”, retrieved from http://www.ejisdc.org

Volume 6, Number 2 (October 2006 - March 2007)

[28] Hamidinava, F. and Madhoushi, M., (2010) “Evaluating The Features Of Electronic Payment Systems In Iranian Bank Users’ View”, International Review of Business Research Papers Volume 6. Number 6. December 2010 Pp.78 – 94

[29] Li, H., Y and Huang, J,(2009) “Applying Theory of Perceived Risk and Technology Acceptance Model in the Online Shopping Channel”, INTERNATIONAL JOURNAL OF BANK MARKETING, Vol.-2, No.-2

[30] Pikkarainen, K and Pikkarainen, T, “The measurement of end-user computing satisfaction of online banking services: empirical evidence from Finland”, retrieved from www.emeraldinsight.com

TABLE I – Demographic information

|

Category | Frequency | Percentage |

| | |

Gender | | |

Male | 117 | 70.05988024 |

IJSER © 2014 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 5, Issue 1, January-2014 184

ISSN 2229-5518

IJSER

IJSER © 2014 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 5, Issue 1, January-2014 185

ISSN 2229-5518

Ph.D | 16 | 9.58083832 |

Diploma | 7 | 4.19161676 |

others | 4 | 2.39520958 |

| | |

User of online transaction | | |

Regular user | 111 | 66.4670658 |

Not user | 44 | 26.3473053 |

Prefer Conventional Method | 8 | 4.79041916 |

Not aware | 4 | 2.39520958 |

| | |

Card Provider | | |

VISA | 84 | 56.75675676 |

Master | 64 | 43.24324324 |

IJTable II: COSNSTRUCTS ANED THEIR RELIARBILITIES

Table III: Descriptive Statistics

| Mean | Std. Deviation | N |

USE | 4.4155 | 1.14391 | 167 |

PEOU | 4.8543 | 1.05860 | 167 |

PU | 4.9187 | .98717 | 167 |

PC | 4.1842 | 1.01282 | 167 |

IJSER © 2014 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 5, Issue 1, January-2014 186

ISSN 2229-5518

PR | 4.8841 | .96034 | 167 |

CUAT | 5.0063 | .93914 | 167 |

Table IV: Model Summary

3 I.821Jc .674

S.73268

E.015

R.025

Table V: Coefficients

Model 5 | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | Collinearity Statistics |

Model 5 | B | Beta | Beta | t | Sig. | Tolerance | VIF |

(Constant) | -.577 | .262 | | -3.458 | .024 | | |

PEU | .681 | .049 | .557 | 12.848 | .000 | .721 | 1.386 |

PUSF | .306 | .049 | .191 | 5.104 | .000 | .716 | 1.396 |

CRED | .189 | .041 | .156 | 4.370 | .000 | .758 | 1.335 |

PRSK | .109 | .046 | .090 | 2.560 | .016 | .647 | 1.528 |

CUAT | -.085 | .037 | -.075 | 2.493 | .018 | .823 | 1.099 |

IJSER © 2014 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 5, Issue 1, January-2014 187

ISSN 2229-5518

Table VI

| VARIABLE | Coefficient | t-Value | Significance | Support |

H1 | Perceived Ease of use | 0.184 | 4.370 | .000 | YES |

H2 | Perceived Usefulness | 0.141 | 5.204 | .000 | YES |

H3 | Perceived Credibility | 0.081 | -2.323 | .019 | YES |

H4 | Perceived Risk | 0.090 | 2.350 | .023 | YES |

H5 | Customer attitude | 0.062 | -1.726 | .03 | YES |

IJSER

IJSER © 2014 http://www.ijser.org