International Journal of Scientific & Engineering Research, Volume 3, Issue 10, October-2012 1

ISSN 2229-5518

Branchless Banking:

“A Substitute for Hawala System in Pakistan”

Syed Shabib-ul-Hasan, Hina Naz

Abstract: Branchless banking is making transaction without visiting a formal banking system. It includes; internet, SMS banking, mobile banking, ATM’s, POS and EFTPOS. Mobile banking has become the future of formal banking system. Hawala is an informal, traditional system for financial transactions in which no money actually enters in bank; all transactions are based on trust among the parties. In Pakistan, majority lives in rural areas and literacy rate is not phenomenal. Number of mobile phones connections is much higher than bank accounts. This work is done with the aim to acknowledge the importance of branchless banking in financial transactions and can it really help us in fighting against money laundering and other illicit functioning through Hawala, which is widely used in underdeveloped and developing countries like Pakistan. Furthermore, this paper also aims at highlighting the similarity between Hawala and Mobile Banking and to explore if these similarities could bring the unbanked population into financial mainstream.

Key Words: Branchless Banking, Hawala, Financial Institution.

1. INTRODUCTION:

—————————— ——————————

intelligence agencies to monitor counter-money laundering

and terrorist financing activities with international

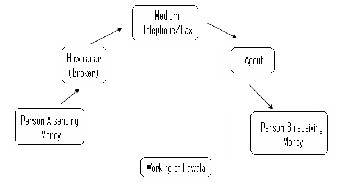

Branchless banking could be considered as a distribution mechanism designed to deliver monetary services being compatible with the modern day requirements. Branchless banking does not require its customer to visit a branch; instead he can make financial transactions using technology based devices. Branchless banking does not only include Mobile Phone Banking, but also includes ATM, Internet, POS and EFTPOS devices. Mobile phones have revolutionized the conventional way of banking. Mobile banking is an opportunity for traditional banking to reach the un-banked; as the wide population in Pakistan live in rural area that doesn’t have access to banking services but have mobile phone connectivity. By working on this opportunity banking sector is able to bring the un-banked to the mainstream of conventional banking by just modifying banking services according to there needs.

SBP has issued regulations for the banks and telecommunication service providers who are interested in opting for branchless banking. As a result, Easy Paisa has been launched in collaboration among Telenor Pakistan and Tameer Microfinance Bank. Easy Paisa is pioneer in branchless banking in Pakistan and data shows its success and popularity among people for making financial transactions. Financial Monitoring Unit (FMU) is also established by SBP to work in close coordination with

————————————————

Syed Shabib-ul-Hasan, Assistant Professor Department of Public Administration University of Karachi, Karachi-75270 Pakistan sshassan@uok.edu.pk

Hina Naz, Research Student Department of Public Administration University of Karachi, Karachi-75270 Pakistan

standards. Any transaction that exceeds Rs.2.5million has been made mandatory to be reported as a currency transaction report to the financial monitoring unit to curb financing the terrorist.

Tameer Microfinance Bank and Telenor Pakistan joined hands in 2009 to launch ‘easy paisa’ aiming at money transference by using mobile phone.1 By easy paisa people are able to transfer local remittances from any nearest easy paisa outlet and international remittances from 80 countries. The customer need to visit any easy paisa outlet and receive remittance and will receive a confirmation SMS. Easy paisa started with payment of utility bills and after receiving overwhelming response encouraged them to come up with enhanced range of services like Mobile Account, Money Transfer, International Home Transfer, Corporate Solutions and Donations.2 In 2010, UBL has also formally launched branchless banking service under the name of OMNI, offering branchless banking to the people of Pakistan.3

People can open an Omni account at nearest omni shop on

providing identity prove and a nominal cash deposit. Omni

is offering variety of services ranging from account opening to cash deposit to bill payments to domestic remittances etc.

IJSER © 2012 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 3, Issue 10, October-2012 2

ISSN 2229-5518

Hawala is an informal and traditional system of transferring value based on the performance and honor of a huge network of money brokers. Hawala is a bank that never exists. This system only works through a trust among the parties. Money is transferred through the brokers called Hawaladars. Work is done on telephone or fax without leaving any footprints. Immigrants use this system to send their earnings to their family. This requires a person to visit a hawaladar, give money to him and then hawaladar calls his broker in that country and simply give him instruction to handover the equivalent amount to the person in his locality. Money transfer through hawala could be risky. It doesn’t include any receipt to leave any footprints to trace. Usually immigrants uses this system for reason like rate of conversion is good, little commission on the part of hawaladar, doesn’t require any paper work, efficient(easily transferred) as bank requires around one week to transfer and most importantly it evades taxes.

In Pakistan, Hawala is widely used by rural population for legitimate transactions. However use of Hawala System affects the economic conditions of a country as it has many serious economic implications. It helps in evading taxes and tightens the government earning from taxes. It also deprives government from foreign exchange, also having adverse effects on balance of payment. As it is not recorded into foreign assets of a country there is no way to quantify it only estimates are made. It is also used by terrorist groups to finance there activities. Task force is also formed to cut-off illicit hawala usage but has not brought the desired results as the system is already underground.

2. LITERATURE REVIEW:

“Mobile Banking refers to provision of bank-related financial services with the help of mobile telecommunication devices. The scope of offered services may include facilities to conduct bank and stock market transactions, to administer accounts and to access customized information.”4 The term mobile banking is a form of branchless banking i.e. financial services via mobile phones. Doing branchless banking through mobile doesn’t require visiting a branch. All the financial transactions can be done with mobile phone. Now the banks all over the world are offering branchless banking services to its customers. Not only banks, but telecommunication companies are doing banking to bank the unbanked. Branchless banking technologies include internet, ATMs, POS, EFTPOS and Mobile phones. State Bank of Pakistan has issued regulations for branchless banking and only bank led model is allowed. Currently Telenor EasyPaisa and UBL Omni are competing to take lion’s share in Pakistani market.

The cost associated with banking through mobile phones is comparatively quiet low to the conventional way of banking. In fact the cost of branchless banking services is around 19 percent cheaper than traditional banking system in 10 countries that are offering branchless banking services5. Branchless banking doesn’t require building an

infrastructure, personnel for operating and maintenance. Average monthly price for using branchless banking services costs US $3.906. In Pakistan it costs US$8.20 a month for easypaisa. In Pakistan the total number for branchless banking outlets has surpassed the total bank branches in country. Setup cost of a branch is 76 percent higher than using a third party agent.7 Branchless banking offers same services as conventional banks with low cost and more ease.

State bank of Pakistan, the regulatory body of banks in Pakistan has issued extensive regulation for the branchless banking activities in 2008. This regulation is applicable to all the banks including Islamic and micro finance banks of Pakistan, those who wish to enter branchless banking. This regulation not only provides a permissible model and framework of activities but also encourage banks to go for innovation and increase the outreach of banking services. SBP regulation focuses on agent related and technology related risk and requires that financial institutions must ensure agent related risk of the transactions either in terms of credit, operational, or risk. It must be ensured that a retailer must, all the time have enough amount of money available for payment to the customers. Customers account should be maintained properly without any hassle and must kept information confidential.

SBP regulations for branchless banking require prospective financial institutions to work with a minimum set of standards for data and security for network, customer protection and risk management. It also describes the procedure and documentation required to be an authorized financial institution to provide branchless banking services. The Board of directors has the responsibility to develop strategic plans for branchless banking and then senior managers have the responsibility to implement the plans. The regulation serves as both an opportunity and obstacle. Regulators have imposed many restrictions limiting the scope of branchless banking but these restrictions are for the protection of consumers. Money laundering needs to be controlled and liquidity risk management becomes another issue. However, SBP is considering to make regulations more flexible to avail opportunity for financial inclusion of un-accessed segment of population. With the help of microfinance institutions mobile banking can unleash the potential to cover underserved segment.

Branchless banking service providers are eager to cover more financial services. This requires maintaining account properly, data management and audit. Data security should be provided and maintaining integrity and trust among alliances, as it involves two players one; financial institution and other telecommunication. However in current circumstances the issue of technological risk is very critical as with the development of technology, the number of cyber crimes also shows increment. The technology has made it possible to outreach financial services to the unbanked. Data storage and information security must follow SOPs. Technological led risk should be controlled via software programs. Telenor and Tameer Microfinance Bank have

IJSER © 2012 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 3, Issue 10, October-2012 3

ISSN 2229-5518

taken steps to ensure security concerns for every transaction. It requires spot-on selection of merchant first, in accordance with the guidelines issued by the State Bank of Pakistan. Secondly, account opening requires verification of CNIC from NADRA. Further, Unstructured Supplementary Service Data (USSD)8 protocol is used to ensure security of transaction.

3. HAWALA SYSTEM:

Hawala is an alternate informal money transfer system that works outside the regulations of conventional banking system. This system has wide spread networking branches easily found in Pakistan, India, Afghanistan and UAE. This system solely works on trust between two parties and work is done on telephone leading no clue to be traced out.

“Its origins are not entirely clear, but it is believed to have been used first in the financing of long-distance trade in the early medieval period on trading route s such as the Silk Road, the Eastern Mediterranean and the Indian Ocean. Hawala is mentioned in texts of Islamic jurisprudence as early as the 8th century. In South Asia, it appears to have developed into a fully-fledged money market instrument, which was only gradually replaced by the instruments of the formal banking system in the first half of the 20th century. Today hawala is probably used mostly for migrant worker s' remittances to their countries of origin.”9

After 9/11 all the eyes are focused on hawala system, as alternate money transference for money laundering and terrorist financing. This doesn’t mean that all the hawala transactions are illegal; most are purposely legal used by expatriate. Investigation of terrorist attacks showed that finance was made through hawala system, as most of the transactions are anonymous. Now a days; a common impression prevail that terrorists are using hawala system to finance there activities around the borders. Since it is anonymous; it leaves few clues for detection and this makes it susceptible for misuse. Charles Bowers states “only after the attacks on the Twin Towers and the Pentagon did knee- jerk speculation by various federal agencies bring the presumed relationship between hawala and terrorism finance to the forefront”10

3.1 Reasons for Hawala Usage:

Hawala entail many reasons for its usage. Among the most few are good exchange rate compared to banking system, less paper work required, low rate of commission, service is offered in far flung areas where no conventional bank is working, less time for delivery and the most importantly delivery at door step. Formal system requires lot of paper trial while in hawala most work is done through memorization or less paper work at brokers end. In rural area no conventional bank exists around miles but hawala delivers fund at door step. These are the reasons that attract people to go for hawala system. Professor Roger Ballard, University of Manchester, also consider trust, speed and ethnic solidarity as reasons for its usage.11 Average cost of

sending $200 to Pakistan from UAE and Saudi Arab cost

$4.88 and $7.30 respectively.12 This high cost force

immigrant Pakistanis to use hawala for making it more

valuable. An important feature about hawala system is that money never enters the formal banking system…13

Hawaladars do have there bank account which is used for settlement and legitimate business transaction.

“The convenience and simplicity of hawala cannot be

matched by banks, as remitting money through banks

requires a process of first going to the bank, then waiting for the recipient’s bank to be credited, and finally the recipient traveling to the bank to withdraw the payment.”14 In Pakistan, the banking network is not wide spread. There are only 26 million bank account holders in Pakistan out of 170 million of its population. Banking network in Pakistan is not readily available in rural areas where more of the population resides. This population use hawala more than urban population due to its coverage. Hawala is also used for the payment of smuggled goods and under invoice for imported goods. This action evades custom duty hence depriving government from taxes.

3.2 Regulating Hawala:

Regulators have attempted to bring hawala under proper regulatory system but constantly fail to do this. Some countries have banned the hawala transactions and in some countries it is regarded as illicit activities. Regulators have agreed that strict regulations on hawala may further put it underground making it out of our reach but system will not die. Regulators agree to make registration for hawaladars mandatory with the government and penalizing those who don’t register. Regulators need to devise procedures to curb its usage for illicit purposes. Evidences support the use of hawala by terrorist to finance there activities. Due to its secrecy, anonymity and being underground attracts terrorist to use this system for money transfer. N.S. Jamwal states “terrorist groups need money to motivate people to join their activities, to procure materials like arms and ammunition and to keep their network going.”15 Hawala system shows it branches all around the globe; it is not isolated solely in one country but is dispersed globally.

“The hawala system, long dominated by South Asians and serving customers throughout the Middle East, appears custom-made for al-Qaeda. It is a cash business that leaves behind few, if any, written or electronic records for use by investigators in following money trails. It operates out of nondescript storefronts and countless bazaars and souks. It reaches both small villages throughout the region and large cities around the world. It is quick, efficient, reliable, and inexpensive. It draws from a long tradition of providing anonymous services…And it is almost entirely unregulated around the world-including in the United States.”16

3.3 Impact of Hawala:

Hawala transactions have direct and indirect

IJSER © 2012 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 3, Issue 10, October-2012 4

ISSN 2229-5518

macroeconomic effects. It is difficult to measure hawala transactions as this is not recorded on foreign assets of a country, increases cash in hands and they are not subject to tax. Tax evasion is a major reason for its usage. Tax evasion results in loss in governmental income. No exact data is available on amount of transaction, only estimation is done and the amount is quite more than what is estimated. The countries that need to have foreign exchange to pay there liabilities are deprived off foreign currency by hawala transactions as payment is made in local currency without moving it in formal banking channel. Hawala transaction also disturbs balance of payment.

4. ATTRACTION FOR BRANCHLESS BANKING:

What has attracted regulators for branchless banking is financial inclusion. Around 65 percent of Pakistan lives in rural areas having limited access to financial services. The concept of conventional banking can’t prevail there due to cost associated with it and low literacy rate. So there should be some alternate channel to include rural population into mainstream of financial system. Branchless banking reduces the cost of delivery of financial services.

Alexander, 200917 argued that two billion people lack access to financial institutions. Banks play a crucial role in today’s economy. Number of mobile phones has increased tremendously in developing countries in recent years. Numbers show that around half of the global inhabitants have access to mobile handset. “In Pakistan, just twenty five million people have bank accounts, while today 70 million have mobile phones.”18 The number of mobile users has now crossed 100 million mark and service providers outreached to distant areas with less cost where conventional banking system requires huge amount of finance to open a single branch. This fact shows that a Pakistan has great potential in mobile banking. In Pakistan banking sector covers only around 12 percent so it’s in best interest for banks and financial institutions to go for alternate financial inclusion channels. Every minute roughly

11 Pakistanis become a part of the cellular community… the sector contributes 3% to the country’s GDP whereas the total telecom sector revenue reached at Rs. 357.7 billion in the year 2009-10.19Success of easy paisa shows figures of Rs. 17 billion Against 10 million Transactions in 15 Months. Statistics shows 70 percent quantum jump. Domestic remittances stand for $6.95 billion from formal channels. But

$2 to $4 Billion is transacted through informal channels like

Hawala system and hand to hand transfer.20

5. FOREIGN REMITTANCE TO PAKISTAN:

The contribution and support of foreign remittances to economic growth in Pakistan is beyond any doubt and only in 2010 it was recorded that around $9 billion had entered the economy through formal channels.21 The significance of this amount and mechanism is very much clear to the

government and regulators both and ever since; they have been trying and getting around 20 percent annual growth in this area. Although the government has targeted to attain a level of around $12 billion support from foreign remittances or else they have to look towards expensive financing options to run the public affairs. Yusupha B Crookes, World bank Country Director for Pakistan said “Despite significant banking sector reforms and efforts to expand financial market coverage over the past few years, outreach has lagged behind the country’s growth and development needs.”22

It is recorded that Pakistan has more than 4.5 million emigrants working abroad and annually more than 140,000 emigrants are added into it (Sabur Ghayur, 2009).23 The number today is much higher because 4.5 million are only registered ones, unregistered can be more. The commitment of the government towards this area could be judged from the fact that they have launched ‘Pakistan Remittance Initiative’ in combined effort with the State Bank of Pakistan and Ministry for Overseas Pakistani. It is hoped that through this initiative government could be able to get double the volume of remittances by attracting and encouraging emigrants to send remittances trough formal channel.24 This scheme allows Pakistanis residing overseas to send remittances at a lower cost and receive a 24 hour toll free call centre, established for their assistance. This system transfer funds to the beneficiary’s account followed by a confirmation SMS.

Farhan Bokhari, (2009) quoted the words of the president

of largest public sector bank in Pakistan, in context of

‘Pakistan Remittance Initiative Program’ that three years

ago, about $4bn was transferred via banks while about $6bn

was believed to be coming through hawala. He further

added “The trend is changing. Now, at least 75 per cent or

even more is coming through official channels and the space

taken by hawala is shrinking.”25 Atif Hanif, pointed that

Pakistan has the ability to stand on its own foot without

relying to the support of IMF and other loan granting

agencies for foreign exchange. If overseas Pakistanis start

using proper banking and money transfer channels for remitting funds to there countries. Proper banking channels

add foreign currency in foreign exchange reserves hence, improving the balance of payment. On the other hand informal channels deprive off foreign reserves and increases cash in hands.26

6. ANALYSIS AND DISCUSSION

A wide range of literature is available on branchless banking and hawala system. Branchless banking is an alternative delivery channels for financial services, through the use of technology especially mobile phones. In Pakistan, there is a great potential for success as bank outreach is very limited. Its young population has few bank accounts while mobile phones are possessed by very large portion of its population. In Pakistan there are around only 26 million bank account holder whereas it has over 100 million mobile

IJSER © 2012 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 3, Issue 10, October-2012 5

ISSN 2229-5518

users. Only 14% of its population has access to formal financial institution. As compared to Bangladesh, 32% of its population has access to formal financial institutions.27

Remittance is a potential lever serving to uplift the Pakistani economy. It is a significant source for foreign exchange. It helps in improving foreign debt situation, builds foreign exchange reserves and strengthens the situation for balance of payment and hence preserves the value of rupee. In contrast, hawala have adverse effects on above mentioned economic factors. Government of Pakistan has taken many steps to bring remittances through regulated channels and lessen the use of informal channels like hawala. A continuous growth is observed in Remittance inflow. Total inflow of foreign remittance to Pakistan is marked at $9 billion with Informal remittance of $2.5 billion through hawala but is only an estimate, as no actual figure is available for hawala. Hawala entail many reasons for its use; among the most few are cost effective, good currency conversion, ease of delivery, low commission, tax evasion and less or no paper trial. Due to its less paper trial and anonymity it is susceptible to abuse. Evidence show that it is being continuously used by terrorist and other extremist group to finance there activities. Hawala has many economic implications. Since it evades tax it tightens the government earning from taxes. It also deprives government from foreign exchange also having adverse effects on balance of payment. As it is not recorded into foreign assets of a country there is no way to quantify it only estimates are made.

In Branchless banking network there is no requirement of visiting a bank for making financial transactions, visit at nearest branchless banking outlet. Branchless banking is cost effective; as infrastructure cost is not there, less time required; transactions through conventional banks require at least one day and in case of foreign remittance it requires one week. Also the transaction cost is low. In Pakistan number of branchless banking outlets are more than bank branches. Financial inclusion has attracted the most to the regulators to go for branchless banking, so that a large segment of population living in rural areas with low or no financial services can be brought into financial channels. In Pakistan, Easy Paisa is pioneer of branchless banking in Pakistan and keeps on achieving milestones. It is second by UBL OMNI. In Pakistan, branchless banking is flourishing and shows remarkable growth. By the end of December

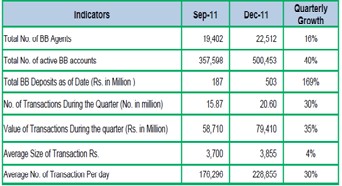

2011, more than 929,000 customers have been registered as m-wallet users. Total number of agents for Branchless banking has reached to a number of 22,512 agents. 86% districts are being covered by Branchless banking service providers. Number of transaction has showed an increment by 30% in December 2011. Average number of BB transactions per month has increased to 7 million involving Rs. 27 billion.

Figure: Branchless banking Indicator Oct-Dec, 11 28

7. CONCLUSION:

Branchless banking has a true potential to reach the unbanked population of a country who live in far flung areas in less cost where traditional banking services are not available. It can surely help in boosting economy as when financial transactions are made through legal channel than authorities can exactly estimate its benefits.

Growth of Easypaisa and Omni has proved that potential exists in branchless banking and is attracting other banks and large retailers to go for mobile banking. Since it is difficult to regulate hawala, branchless banking could be use to replace hawala system. There is a lot of similarity between both. If similarities between hawala and branchless banking are properly targeted, it will bring the unbanked population of a country into financial mainstream. Although, it is not always negative; immigrants are using it for making remittance to their family living in rural areas where banking service is not available but has a potential to support negative activism.

Awareness level among masses about what comes in branchless banking is very low. Despite the fact that branchless banking is growing as it is cost and time effective, telecom and banking sector should take keen interest in branchless banking by efficiently collaborating with each other.

8. RECOMMENDATION:

It is clear that awareness level about branchless banking is very low. In real what comes in branchless banking people are not aware of it. There is a need for awareness program and authorities have to show concern to promote branchless banking.

Branchless banking is secure but people have concerns for safety delivery without any technological barriers. The

IJSER © 2012 http://www.ijser.org

International Journal of Scientific & Engineering Research, Volume 3, Issue 10, October-2012 6

ISSN 2229-5518

maximum transaction limit provided by SBP is very low which becomes barrier when user wants to transact large amount.

More potential exist for growth in branchless banking in Pakistan as success factors are showing continuous increase in usage level. Telecom and banking sector must encourage new entrants for healthy competition and better service. REFERENCES & BIBLIOGRAPHY

[1]“Welcome to Tameer Microfinance Bank Limited,”

http://www.tameerbank.com/money_transfer.htm, 19 Feb. 2012

[2] “Money transfer via Mobile: Telenor Easy Paisa,” Ammar-3Sixty. http://ammar360.com/2009/11/25/money-transfer-via-mobile-telenor-easy- paisa, 29 Feb. 2012

[3]“News,” United Bank Limited Pakistan Media Center. http://www.ubl.com.pk/news/UBL_Omni_Dukaan.asp, 29 Feb. 2012

[4] Tiwari, R. and S. Buse, The Mobile Commerce Prospects: A Strategic Analysis of Opportunities in the Banking Sector, Hamburg University Press, 73.

[5] C. Mckay and M. Pickens. "Branchless Banking 2010: Who’s Served? At What

Price? What’s Next?" CGAP Focus Note, 5 Sept. 2010 [6] Ibid, 5

[7] S. Kardar, "Branchless banking is the future of financial sector," Speech, launching ceremony of Omni from Pakistan, Pakistan, 20 Jan. 2011.

[8] A. Haider,. Interview by Aamir Attaa. Personal interview. Pakistan, 5 April,

2010.

[9] "Hawala System Money Brokers Transfer Funds Legal Broker," Business, Economy, Market Research, Finance, Income Tax Information. http://www.economicexpert.com/a/Hawala.html, 29 Feb. 2012

[10] C. Bowers,. "Hawala, money laundering, and terrorism finance: micro- lending as an end to illicit remittance," Denver Journal of International Law and Policy, 22 June 2009, 379-419.

[11] J. Wilson, "Hawala and other Informal Payments Systems: An Economic

Perspective," Speech, Seminar on Monetary and Financial Law from IMF, Washington D.C, 16 May, 2002.

[12]"Remittances Profile: Pakistan," Migration policy Institute. www.migrationinformation.org/datahub/remittances/Pakistan.pdf , 20 Feb.

2012

[13] UN General Assembly, Special Session on the World Drug Problem, 8-10

June 1998.

[14] T. Nenova, C.T. Niang, and A. Ahmad, "Harnessing Remittances for Access to Finance," In Bringing finance to Pakistan's poor access to finance for small enterprises and the underserved, 75-97. Washington, D.C.: World Bank, 2009.

[15] N.S. Jamwal, “Hawala-The Invisible Financing System of Terrorism. Strategic Analysis,” A Monthly Journal of the IDSA, (April-June 2002). http://www.mafhoum.com/press3/111E62.htm, 20 Feb. 2012.

[16] "National Commission on Terrorist Attacks Upon the United States," National Commission on Terrorist Attacks Upon the United States. http://www.9-11commission.gov/hearings/hearing1/witness_wolosky.htm,

20 Feb. 2012.

[17] D. Alexander, “Anxious times for the global financial system,” Chatham

House, Feb. 2009. [18] Ibid, 17

[19] M. Khan, “SBP Hosts Branchless Banking Conference,” Telecom and IT news from Pakistan. http://propakistani.pk/2010/04/18/sbp-hosts-branchless- banking-conference, 29 Feb. 2012

[20] Daily Times (Karachi), "Easypaisa transactions up 70% in 3 months," 22 Jan.

2011.

[21] "Foreign Remittances to Pakistan in 2011, Growth and Pakistan Economic Condition," Views Buzz. http://www.viewsbuzz.com/foreign-remittances-to- pakistan-in-2011-growth-and-pakistan-economic-condition/, 20 Feb. 2012.

[22] "Pakistan - World Bank Report Calls for Easier Access to Finance for Pakistan’s Poor." The World Bank.http://www.worldbank.org.pk/WBSITE/EXTERNAL/COUNTRIES/S OUTHASIAEXT/PAKISTANEXTN, 21 May 2012

[23] Sabur Ghayur, “Economy of Pakistan: Employment generation through overseas migration,” Economy of Pakistan, 28 Dec. 2008 http://economyofpakistan.blogspot.com/2009/12/employment-generation- through-overseas.html, 20 Feb. 2012

[24] “Pak remittance initiative launched to double volume in next 2 years,” The Free Library. (2009) http://www.thefreelibrary.com/Pak remittance initiative launched to double volume in next 2 years.-a0206490599,20 Feb. 2012

[25] F. Bokhari, "Pakistan takes a grip on money transfers - FT.com." World

business, finance, and political news from the Financial Times. http://www.ft.com/cms/s/0/6e5c1104-e4e2-11de-817b-

00144feab49a.html#axzz1vVhRkSDd, 21 May, 2012

[26] “Pakistan can achieve foreign exchange stability and economic independence on permanent basis without taking loans”

[27] T. Nenova, C.T. Niang, and A. Ahmad, “In Bringing finance to Pakistan's

poor access to finance for small enterprises and the underserved”, ix Washington,

D.C.: World Bank, 2009.

[28] Branchless banking newsletter, SBP, Oct-Dec, 2011 http://www.sbp.org.pk/publications/acd/BranchlessBanking-Oct-Dec-

2011.pdf, 22 May,2012

IJSER © 2012 http://www.ijser.org